In fact, I used to be proud to say that, thinking that gambling was only for chumps.

But after reading Crist on Value, I’m beginning to reconsider my position on the activity.

Let me explain…

Crist on Value

Steven Crist is a legend in the world of horse betting.

A Harvard graduate, Steve Crist took a different approach to betting on horses than most other people, applying math, logic, and probability in making wagers, instead of simply picking the most likely horse to win the race. While by no means was this revolutionary, Steven Crist has been one of the most outspoken advocates for using this approach of finding value in wagers, and he’s used it to great success (Crist’s nickname is “King of the Pick Six” – the pick six is a wager where the bettor must select the winners of six consecutive races and is considered the most difficult type of bet).

In 1998, Steven Crist teamed up with Alpine Capital to purchase Daily Racing Form (DRF), a newspaper that has published the past performances of race horses since 1894 and is the gold standard statistical service for horse race handicappers (as one journalist put it, DRF is to horseplayers what the Wall Street Journal is to investors). After leading the publication for many years, Crist retired from DRF in 2016. While running DRF, Steve Crist also wrote a weekly column and a blog, where he often talked about his method of horse betting.

In 2001, Steven Crist wrote a chapter for the book Bet With the Best: Strategies from America’s Leading Handicappers. That chapter was simply called Crist on Value.

While Steven Crist doesn’t mention stocks, markets, the economy, companies, or investing anywhere at all in Crist on Value, the parallels between horse betting and investing are incredibly interesting. In fact, most of Crist on Value seems like it belongs in Benjamin Graham’s The Intelligent Investor, not a book on how to bet on horses!

Michael Mauboussin, a value investor and one of the sharpest thinkers in finance today, has called Crist on Value “one of the best 13 pages on investing I have ever read.”

I’d probably agree with that.

The Similarities Between Horse Race Betting and Investing

As it turns out, the connection between horse betting and investing runs pretty deep.

As a kid, Warren Buffett used to bet on horse races at Omaha’s Ak-Sar-Ben Race Track. And here’s Charlie Munger talking about horse race betting in his famous Worldly Wisdom speech:

The model I like — to sort of simplify the notion of what goes on in a market for common stocks — is the pari-mutuel system at the racetrack. If you stop to think about it, a pari-mutuel system is a market. Everybody goes there and bets and the odds change based on what’s bet. That’s what happens in the stock market.

Now, before you invite me to sit next to you at the bank of slot machines at the nearest casino, remember that what we’re talking about here are pari-mutuel betting systems – gambling games like horse betting and poker where you’re betting against all the other betters – and NOT fixed-odds betting – games like roulette or craps where the odds are fixed.

Winning these fixed-odds games is pure chance and making money off of them over the long-term is impossible because the casino is setting the odds. In American Roulette, there are 38 spaces. If you were to bet $1 on each of 1,000 spins, you would have bet a total of $1,000 – but you would only have won back a total of $936, for a total loss of $64. The longer your play, the more you lose and the more the house wins (hence the phrase “the house always wins”).

Pari-mutuel betting games, on the other hand, are an entirely different story because it’s the public – not the house – that is setting the price of the bet. And somewhere between frequently, occasionally, and rarely, the public makes the wrong price.

Michael Mauboussin expands on this point in his book More Than You Know: Finding Financial Wisdom in Unconventional Places:

One way to think about it is to contrast a roulette wheel with a pari-mutuel betting system. If you play a fair game of roulette, whatever prediction you make will not affect the outcome. The prediction’s outcome is independent of the prediction itself. Contrast that with a prediction at the racetrack. If you believe a particular horse is likely to do better that the odds suggest you will bet on the horse. But your bet will help shape the odds. For instance, if all bettors predict a particular horse will win, the odds will reflect that prediction, and the return on investment will be poor.

The analogy carries to the stock market. If you believe a stock is undervalued and start to buy it, you will help raise the price, this driving down prospective returns. This point underscores the importance of expected value, a central concept in any probabilistic exercise. Expected value formalizes the idea that your return on an investment is the product of the probabilities and the various outcomes and the payoff from each outcome.

This is similar to what I wrote about in Why the Stock Market is So Hard to Predict. You see, roulette and craps are “level one” chaotic systems – chaos (i.e. randomness) that does not react to predictions made about it. Everybody in the casino can bet on red 32 if they want, but the roulette wheel won’t care and it won’t affect the 1/38 chance that the ball has of landing on red 32. Likewise, the casino could care less which numbers are played – the payoff remains the same.

In contrast, pari-mutuel betting games like horse betting and poker are “level two” chaos systems – these games react to predictions made about their outcomes. While the horses don’t care who’s picking them as a favorite to win and the cards that are dealt aren’t affected by a poker player’s wager, the betting within the game itself IS affected by the actions of other bettors. In horse race betting, your bet helps shape the odds for that wager – which might be better or worse than the actual odds a certain horse has of winning the horse race. In poker, the players determine the size of the pot – which might be large or small relative to the odds your hand has of winning. And the same is true of the stock market, where investors’ predictions of a company determine the price of that company’s stock – which might be more or less than the company’s true intrinsic value.

A Quick Primer on Some Important Horse Betting Terms

Before we actually get to Crist on Value, I think it’s helpful to know some of the most important horse betting terms (so that you can understand some of the nuances of what Steven Crist is actually talking about). Here are the horse betting terms you should know:

- Pari-mutuel betting: In pari-mutuel betting, all bets are placed together in a pool, the “take” is paid to the house (see below), and the remaining amount is disbursed to the winners in proportion to the amount wagered. This is in contrast to fixed-odds betting, where the odds are set by the bookmaker. In pari-mutuel betting, the final payout is not determined until the pool is closed. In fixed-odds betting, the payout is agreed at the time the bet is sold.

- The house: The institution organizing the betting (e.g. the racetrack, casino, or bookmaker).

- Takeout: Also called the take, cut, rake, or vigorish, this is the amount the house takes before paying out the winnings. For horse race betting, this varies by state and track, ranging from 15.43% to 31% depending on the specific wager and location.

- Breakage: The winning payoff is always rounded down to the nearest 10 or 20 cent increment. This is called breakage, and the delta is kept by the racetrack.

- Payoff: This is the amount actually paid to the winning bettors. Here is an example of how payoff is calculated:

- If $1,000 is bet in total on win bets, and $200 is bet on the winning horse, then:

- First, the track collects it’s cut. Let’s say the takeout is 17%, which leaves $830 ($1,000 x 83%).

- This ratio of winnings to winning bet is $830/$200 = 4.15. This ratio is then applied to the minimum $2 bet: 4.15 x $2 = $8.30. The $8.30 is rounded down to the nearest 20-cent increment, or $8.20.

- So $8.20 is the final payoff per $2 bet. All winning bettors will be paid at this ratio. For example, a $100 bet will win $100 x (8.20/2.00) = $410.

- If $1,000 is bet in total on win bets, and $200 is bet on the winning horse, then:

- Odds: Converting percentage probabilities (like a horse’s winning chance) into betting odds is easy. If I think a horse has a 20% chance of winning, then that horse will win 1 out of every 5 times – in other words, it will win once (20% of the time) and will lose 4 times (80%) out of every 5 races. So the odds of that horse winning are 4-1 (80%/20% to 1). If I think the horse has an 80% chance of winning, then the odds of that horse winning are 1-4. As you can see, odds of winning are listed as LOSE-WIN. Converting odds into probabilities is a similar task. If a horse is listed as paying off at odds of 3-2, then the implied probability of that horse winning is 2 / (3+2) = 40%. In the case of 3-2 payoff odds, the payoff on a $2 wager would be $5 ($2 original bet + $3 in profit).

- Horseplayer: Some one who bets on horse races.

- Daily Racing Form (DRF): The Daily Racing Form (DRF) provides the past performances of all the horses running on the day’s program and includes informative horse racing articles and handicapping by DRF staff. Digital issues and subscriptions now range from $3.50 to $99.95, depending on the type of access and duration.

- Handicapping: The practice of assigning predicting the outcome of horse races by assigning percentages to each horses chance of winning.

- Long / short odds: A horse with long odds has apparently no chance of winning (e.g. 19-1, or a 5% chance of winning). A horse with short odds is favored to win (e.g. 2-3, or 60% chance of winning).

- Overlay / underlay: An overlay is a good bet – the horses odds of winning are longer (worse) than they should be. An underlay is a bad bet – the horses odds of winning are shorter (better) than they should be).

- Win, place, and show: The most basic bet is picking the horse that you think will finish first (win). You can also bet on a horse that you think will finish first OR second (place) or will finish first, second, OR third (show).

- Exacta, trifecta, and superfecta: The exacta is a bet on the horses you think will finish first and second – but they must be in the correct order. The trifecta is the same type of wager but on the horses you think will finish first, second, and third, and the superfecta is a bet on the horses you think will finish first, second, third, and fourth (again, the horses must finish in the correct order).

- Daily double, pick three, pick four, or pick six: The daily double is a bet on the first place horse in two consecutive races (usually the first two of the day). The pick three and pick four are bets on the first place horse in three or four, respectively, consecutive races. The pick six is a bet on the first place horse in six consecutive races (usually the last six of the day). If nobody calls all six correctly, part of the winning pool is paid to those correctly picking five of the winning horses (or less if nobody picked five), and the rest is carried over to the next pick six pool.

- Minimum bet amounts: A minor – but important – detail: the minimum bet at racetracks is generally $2 on win, place, and show bets, and $1 on all other types of bets.

Steven Crist on Value (Investing) and Horse Betting

Sweet! Now we’re at the exciting part – breaking down Crist on Value.

Here are my 6 key takeaway insights from Steven Crist on value investing and how to make better decisions:

1. Price versus Value

“The point of this exercise is to illustrate that even a horse with a very high likelihood of winning can be either a very good or a very bad bet, and the difference between the two is determined by only one thing: the odds.”

As Steven Crist explains, with modern AI and machine learning algorithms analyzing extensive datasets, horse betting probability calculations have become increasingly sophisticated. A horse’s potential winning chances can now be assessed with greater precision, revealing nuanced insights about value betting.

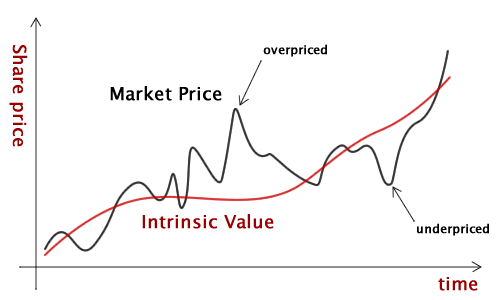

What Crist is doing here is separating out price (the payoff and the payoff’s implied winning percentage) and intrinsic value (the horse’s actual chance of winning). This is the fundamental principle of value investing that Benjamin Graham and David Dodd first set forth in Security Analysis, with its most recent 7th edition released in 2023:

Price ≠ Intrinsic Value

This, of course, is directly applicable to investing. Any stock can be a great investment or a bad investment – even if the company is amazing. It all depends on the stock’s price and it’s comparison to that company’s true intrinsic value.

2. You Need to Have the Right Temperament

“Now ask yourself honestly: Do you really think this way when you’re handicapping? Or do you find horses you “like” and hope for the best on price? Most honest players will admit they follow the latter path.

This is the way we all have been conditioned to think: Find the winner, then bet. Know your horses and the money will take care of itself. Stare at the past performances long enough and the winner will jump off the page.

The problem is that we’re asking the wrong question. The issue is not which horse in the race is the most likely winner, but which horse or horses are offering odds that exceed their actual chances of victory.

This may sound elementary, and many players may think they are following this principle, but few actually do. Under this mindset, everything but the odds fades from view. There is no such thing as “liking” a horse to win a race, only an attractive discrepancy between his chances and his price. It is not enough to lose enthusiasm when the horse you liked is odds-on or to get excited if his price drifts up. You must have a clear sense of what price every horse should be, and be prepared to discard your plans and seize new opportunities depending solely on the tote board.

If you begin espousing this approach, you are sure to suffer abuse from your fellow horseplayers. When one of them asks you who you like in a race and you say, “I think the 4 is a bigger price than he should be,” the likely response is, “So what? Who do you like?” Your cronies are apt to tell you that you should be betting on horses, not on prices, and after an inevitable stretch of watching some of their underlays win, you will begin to doubt yourself.

Sticking to your guns is easier said than done, but it is the only way to win in the long run. The horseplayer who wants to show a profit must adopt a cold-blooded and unsentimental approach to the game that is at variance with both the “sporting” impulse to be loyal to your favorite horses and the egotistical impulse to stick with your initial selection at any price. This approach requires the confidence and Zen-like temperament to endure watching victories at unacceptably low prices by such horses.“

There’s so much wisdom is this short passage. Let’s break it down.

First, Steve Crist is saying you shouldn’t be asking which horse in the race is most likely to win. Your job is to figure our which horse is offering odds that exceed its actual chance of victory. This is what famous value investor Howard Marks calls “second-level thinking” in his book The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor.

First-level thinkers only consider one variable at a time, often the one that is the most obvious: What horse is the best? What company is the best? Second-level thinkers take many thing into account and ask the complicated questions: Which horse is disliked by the crowd but actually provides a good return given its true chance of winning? Which company does the market dislike due to certain short-term headwinds, but actually has great long-term value that everyone else is overlooking?

Then, Crist says that you MUST stick to your guns, even when your friends and your own emotions are tugging at you to abandon your approach and join the crowd. Rudyard Kipling would remind you to “keep your head when all about you / are losing theirs.”

It’s the only way to win in the long run. If you want to make money – whether it’s in horse betting or in the stock market – you must adopt a cold-blooded and unsentimental approach to the game. And you have to do this despite the egotistical impulse to stick with your initial selection at any price.

You have to be willing to change your mind and strong enough to walk away from an investment if the price isn’t right. This approach requires the confidence and Zen-like temperament to endure watching victories at unacceptably low prices by such horses – or to watch other investors make money on a stock that they bought for far more than its intrinsic value (a product of luck,

instead of skill).

3. Invest with a Margin of Safety

“I made Two Item Limit 60 percent to win the race, giving a 35 percent chance to Tap Dance and the remaining 5 percent to their three overmatched opponents. Odds of 2-1 or better on Tap Dance would make her playable.

Unfortunately, everyone else seemed to have had the same idea about Tap Dance waltzing to the lead. With five minutes to post, both fillies were even money, and I felt neither remorse nor disloyalty as I went to the window to make the only logical bet: Two Item Limit to win, which she did at $4.40. Betting 6-5 shots to win is not my usual style, but I saw no other way to play the race and was convinced I was receiving outstanding value. When I first began playing the races, I probably would have bet on both Dollar Bill and Tap Dance instead of Monarchos and Two Item Limit, out of loyalty to my initial selections and the sense that you “should” bet on the horses you initially like.

The success of these two plays, though, was ultimately based upon the probability of victory I had assigned to each winner. I cannot argue in good conscience that Two Item Limit had precisely a 60 percent chance of victory as opposed to 57 or 63 percent, and I doubt that such calibration is in fact achievable. It is, however, possible through experience to get close enough that if you demand sufficient value to cover the margin of error, you should outperform the competition – your fellow horseplayers.“

I included Steven Crist’s entire anecdote about betting on the horse Two Item Limit so that we could set the stage for his last two lines.

Crist calculated Two Item Limit’s chance of winning to be 60%. But this is a rough calculation – Crist admits that he wouldn’t be able to argue that the horse’s victory was exactly 60% and not 57% or 63%. In fact, that degree of precision is probably impossible. What Crist DID do, however, was apply his considerable experience in horse race handicapping and combine that experience with a margin of safety.

The 6-5 odds on Two Item Limit right before the race started implied that the other bettors thought the horse only had a 45% chance to win, not the 60% Crist had calculated. The 6-5 odds result in a payoff of $3.60 for every $2 wager (assuming a variable takeout rate between 14-35% depending on the specific racing jurisdiction), which translates into an 80% return – given that Two Item Limit wins. Run this scenario 50 times with Two Item Limit winning 60% of the time, and Crist would have bet $100 and won $108. The difference between Crist’s calculated 60% chance of winning and the implied 45% chance of winning gave Crist a big margin of safety. He would’ve had to have been way off on his prediction of the race’s outcome to not come away with a profit – even after takeout and breakage.

(An important note here: Crist, of course, had a 40% chance of losing that wager – something that he isn’t able to control. And he wouldn’t be able to repeat this scenario 50 times like I described above. But he COULD bet on 50 other races with similar probabilities – something a professional horseplayer would naturally do. Over time, the law of averages makes the percentages true – even if in any one scenario the outcome isn’t favorable).

Warren Buffett has talked about margin of safety using similar terms:

You have to have the knowledge to enable you to make a very general estimate about the value of the underlying business. But you do not cut it close. That is what Ben Graham meant by having a margin of safety. You don’t try to buy businesses worth $83 million for $80 million. You leave yourself an enormous margin. When you build a bridge, you insist it can carry 30,000 pounds, but you only drive 10,000 pound trucks across it. And that same principle works in investing.

When betting on horses, you don’t bet on a horse that you think has a 45% chance of winning the race if the odds imply it has a 40% chance of winning the race. That margin of safety just isn’t big enough for you to be wrong. As Steven Crist writes, you need to demand sufficient value to cover the margin of error.

The same thing works in investing. You don’t try to buy businesses worth $83 million for $80 million. You try to buy business worth $150 million for $80 million. Then you’ll have a margin of safety – the main purpose of which is to make an accurate estimate of the future (of a business or of a horse race) unnecessary in the first place.

4. Market Efficiency

“Does that mean today’s player faces nothing but higher vigorish and the remaining sharpies? Not at all. I firmly believe that, in general, the nitwits still outnumber the sharpies. More important, most sharpies aren’t as sharp as they think, and even the winning sharpies make plenty of egregious mistakes on individual races. As long as the volume of ill-informed money exceeds the takeout, there can be a positive expectation for the true sharpshooter who waits for the competition to make mistakes.“

Many people bring up the Efficient Market Hypothesis, claiming that the stock market is completely efficient and that it’s impossible to find undervalued securities. Any outperformance versus the market can only be attributable to luck.

Warren Buffett – and his incredible track record of approximately 19.8% returns per year from 1965 through 2023 – would obviously disagree.

It might be true that the market is more efficient today than it was decades ago and that it’s harder to beat the market – just like it’s become harder to make money from horse betting since attendance at horse races has declined (meaning less uninformed bettors) and takeouts at race tracks across the country have been increased to make up for that decline.

But if you’re sharp, there’s still value to be found. You just need to be patient and wait for your competition – and the market – to make a mistake.

5. Wait for the Right Race

“There are also plenty of races in which your competition will make no actionable mistakes. Everyone seems to be at about the right price, and there is no compelling reason to jump into the pool. It is worth remembering that the whole is better than the sum of its parts: The betting public’s post-time favorite wins more often than any individual public handicapper, and over time first choices win more than second choices, which win more than third choices, and so on down the line. There is no shame in passing a race because you just don’t see any value in it. Nor should you force yourself to play a race in which you have no confidence in your own odds line. That doesn’t mean you have to sit on your hands – $1 boxes for action were made to fill the spaces between races where you have a legitimate edge or opinion.”

“It’s not an easy game, but you’re not playing against “the game.” You’re betting against the other bettors. It doesn’t matter if they pick as many winners as you do, or even more, if you are betting only when the price is right.“

Despite my earlier comments on market ineffiency, that doesn’t mean that every single stock is mispriced. Sometimes, the price IS right. In these instances, your best action is to – do nothing! Just wait for the race where you have a real advantage.

As Warren Buffet likes to say, “the stock market is a no-called-strike game. You don’t have to swing at everything – you can wait for your pitch.”

Of course, when your pitch does come, then you need to bet big on it – since great opportunities to pop up as often as they ought to. Here’s another quote from Warren:

When it rains gold, put out the bucket, not the thimble.

Hundreds of Books on Horse Race Betting

And when the Buffett family moved to Washington, D.C., Warren just had one request for his dad:

“When we got to Washington, I said, ‘Pop, there’s just one thing I want. I want you to ask the Library of Congress for every book they have on horse handicapping.’ And my dad said, ‘Well, don’t you think they’re going to think it’s a little strange if the first thing a new Congressman asks for is all the books on horse handicapping?‘”

But Buffett reminded his father of the help he gave him during the winning campaign, and pledged to be there for him again during his re-election. So Howard got Warren hundreds of books about handicapping horses.

“Then what I would do is read all these books. I sent away to a place in Chicago on North Clark Street where you could get old racing forms, months of them, for very little. They were old, so who wanted them? I would go through them using my handicapping techniques to handicap one day and see the next day how it worked out. I ran tests of my handicapping ability – day after day – all these different systems I had in mind.“

Buffet on Value and DRF

Buffett noted that a bookie actually took action inside Washington’s Old House Office Building.

“You could go to the elevator shaft and yell, ‘Sammy!’ or something like that and this kid would come up and take bets.“

Even Buffett himself did some bookmaking for guys who wanted to get down on the big races like the Preakness Stakes. “That’s the end of the game I liked, the 15 percent take with no risk,” Buffett said.

Buffett got along well with his high school golf coach, Bob Dwyer, and the two frequently rode the Chesapeake & Ohio railroad together from Silverspring, MD to Charles Town racetrack in West Virginia. Dwyer taught Buffett how to better understand the Daily Racing Form.

“I’d get the Daily Racing Form ahead of time and figure out the probability of each horse winning the race. Then I would compare those percentages to the odds,” said Buffett, who bet from $6 to $10 to win.

“Sometimes you would find a horse where the odds were way, way off from the actual probability. You figure the horse has a 10 percent chance of winning, but it’s going off at 15-to-1.“

That last part sounds a lot like Crist on Value, doesn’t it?

Going broke one day at Charles Town

One day, Buffett went to Charles Town by himself. He lost the first race and his performance went from bad to worse until he was down $175. Feeling depressed, he went to an ice cream shop and bought himself a sundae with the last of his money.

While eating, Buffett thought to himself that he had just lost more money than he made in a week.

“And I’d done it for dumb reasons. You’re not supposed to bet every race. I’d committed the worst sin, which is that you get behind and you think you’ve got to break even that day. The first rule is that nobody goes home after the first race, and the second rule is that you don’t have to make it back the way you lost it. That is so fundamental.“

This was an important lesson that definitely influence Buffett’s investing later in life. You’re not supposed to be every race. Instead, just wait for the right pitch.

Charlie Munger on Horse Betting

Here’s an excerpt from a speech Charlie Munger gave at the USC Business School in 1994 called A Lesson On Elementary, Worldly Wisdom as it Relates to Investment Management & Business. In this segment, Charlie Munger gave his thoughts on horse betting, pari-mutuel betting systems, and investing in the stock market:

Any damn fool can see that a horse carrying a light weight with a wonderful win rate and a good post position etc., etc. is way more likely to win than a horse with a terrible record and extra weight and so on and so on. But if you look at the odds, the bad horse pays 100 to 1, whereas the good horse pays 3 to 2. Then it’s not clear which is statistically the best bet using the mathematics of Fermat and Pascal. The prices have changed in such a way that it’s very hard to beat the system.

And then the track is taking 17% off the top. So not only do you have to outwit all the other betters, but you’ve got to outwit them by such a big margin that on average, you can afford to take 17% of your gross bets off the top and give it to the house before the rest of your money can be put to work. Given those mathematics, is it possible to beat the horses only using one’s intelligence? Intelligence should give some edge, because lots of people who don’t know anything go out and bet lucky numbers and so forth. Therefore, somebody who really thinks about nothing but horse performance and is shrewd and mathematical could have a very considerable edge, in the absence of the frictional cost caused by the house take. Unfortunately, what a shrewd horseplayer’s edge does in most cases is to reduce his average loss over a season of betting from the 17% that he would lose if he got the average result to maybe 10%. However, there are actually a few people who can beat the game after paying the full 17%.

I used to play poker when I was young with a guy who made a substantial living doing nothing but bet harness races…. Now, harness racing is a relatively inefficient market. You don’t have the depth of intelligence betting on harness races that you do on regular races. What my poker pal would do was to think about harness races as his main profession. And he would bet only occasionally when he saw some mispriced bet available. And by doing that, after paying the full handle to the house—which I presume was around 17%—he made a substantial living. You have to say that’s rare. However, the market was not perfectly efficient. And if it weren’t for that big 17% handle, lots of people would regularly be beating lots of other people at the horse races. It’s efficient, yes. But it’s not perfectly efficient. And with enough shrewdness and fanaticism, some people will get better results than others.

The stock market is the same way—except that the house handle is so much lower. If you take transaction costs—the spread between the bid and the ask plus the commissions—and if you don’t trade too actively, you’re talking about fairly low transaction costs. So that with enough fanaticism and enough discipline, some of the shrewd people are going to get way better results than average in the nature of things.

It is not a bit easy. And, of course, approximately 90% of actively managed funds will underperform low-cost index funds. But some people will have an advantage. And in a fairly low transaction cost operation, they will get better than average results in stock picking.

How do you get to be one of those who is a winner—in a relative sense—instead of a loser? Here again, look at the pari-mutuel system. I had dinner last night by absolute accident with the president of Santa Anita. He says that there are two or three betters who have a credit arrangement with them, now that they have off-track betting, who are actually beating the house. They’re sending money out net after the full handle—a lot of it to Las Vegas, by the way—to people who are actually winning slightly, net, after paying the full handle. They’re that shrewd about something with as much unpredictability as horse racing. And the one thing that all those winning betters in the whole history of people who’ve beaten the pari-mutuel system have is quite simple. They bet very seldom. It’s not given to human beings to have such talent that they can just know everything about everything all the time. But it is given to human beings who work hard at it—who look and sift the world for a mispriced bet—that they can occasionally find one. And the wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don’t. It’s just that simple. That is a very simple concept. And to me it’s obviously right—based on experience not only from the pari-mutuel system, but everywhere else.”

The Ultimate Guide to Value Investing

Do you want to know how to invest like the value investing legend Warren Buffett? All you need is money to invest, a little patience—and this book. Learn more