One of the challenges many new budgeters face is how to handle the periodic payments that arise throughout the year. Scheduling the monthly rent or mortgage payment is easy, as are estimates for electricity (seasonally adjusted), telephones, and even gas and food.

But what about the annual life insurance premiums? How about the semi-annual car insurance payments? Even events like Christmas can be a budgeting challenge. Do you budget your Christmas spending just in November and December (which can be tough if your budget is tight), or do you somehow spread the budgeting out all year? And how can you easily keep track of it all?

Enter the sinking fund.

What Is a Sinking Fund?

It’s historically a term used in accounting to describe setting aside money for debt retirement or a large capital expenditure (think of a new roof or expensive piece of equipment that will need to be bought in the future). The company will simply set aside an amount (often fixed) each month for a set period of time, after which the funds needed to purchase the equipment or new roof will be readily available.

For a simple example, if the company needs a new $24,000 truck next year, they will set aside $2,000 per month for 12 months. Often sinking funds are used for very large, multi-year projects. Imagine a large commercial building needing a $1,000,000 roof replacement every 25 years. It’s a lot easier to set aside $3,333 per month for 25 years than to come up with $1,000,000 when the replacement is needed!

Let’s do a little Q&A regarding sinking funds for our personal use!

Using a Sinking Fund for Personal Finances

Using a sinking fund is great not only for large-ticket items (like a car replacement) but also for irregular expenses throughout the year. We all face those large periodic expenses. Perhaps in the past, we’ve stressed about how we’ll come up with the amount due by the deadline.

The use of a sinking fund has eliminated the significant fluctuations in our monthly spending. It’s much easier to set aside $100 every month than trying to come up with $1,200 at one time. Most of us don’t have that much leeway in our monthly spending to cover a bill that large.

What Expenses Should Be Included in Your Sinking Fund?

Personally, we use this principle for many of our irregular expenses:

• Annual automobile, homeowners and umbrella premiums

• Personal Property Taxes

• Real Estate Taxes

• Christmas and other gifts

• Vacation

• Gym membership (paid annually for better pricing)

• School expenses, summer camps

☝️ Some expenses are lower if paid annually, so a sinking fund can actually save you money!

For example, auto and home insurance are often less if paid in full at the beginning of the policy. Our gym offers three free months if we pay for a year in advance. Relatively small savings like these really add up over the course of the year, so don’t miss out on them!

You’ll need to determine your own list. Scour your monthly spending plan for any items that will occur sometime during the year, but not on a monthly basis. If you pay your car insurance monthly, leave it in your budget. If you pay it annually as we do, include it in the sinking fund.

Of course, be reasonable. For small bills (for example, an annual $20 magazine renewal), simply fund them with your regular cash flow during the month of renewal. Sinking funds should only be used for those expenses that can’t be easily funded in one month’s budget.

How Much to Add to the Sinking Fund Each Month

Simply estimate the annual budgeted amount for each of the items you have selected to include in your sinking fund. Then total the individual estimates and divide by 12 to convert the annual total to a monthly amount. This freshly calculated monthly amount then appears on the spending plan (i.e., budget) each month.

An example might look something like this:

Sinking fund contribution calculation

| Item Description | Annual Amount |

|---|---|

| Automobile Insurance | 900.00 |

| Christmas Gifts | 750.00 |

| Gym Membership | 360.00 |

| Life Insurance | 255.00 |

| Personal Property Taxes | 1,035.00 |

| Vacation | 1,500.00 |

| Total | 4,800.00 |

| Monthly Amount (Total/12) | 400.00 |

For this example, $400 would be added to your sinking fund each month and it would appear as a line item on your monthly budget, just like food and utilities.

💡 Be sure to review these amounts each year as they will surely change. Some may be removed and others added.

This may sound complicated, but it really isn’t! Let me illustrate with a case study:

Sinking Fund Case Study

Suppose your monthly income was $3,500 and your sinking fund contribution for the month was $400 (as calculated per the guidelines described earlier). Assuming (for simplicity sake) you’re opening your bank account with your first month’s paycheck.

Further, assume over the next three months, you’ll have to pay your life insurance annual premium of $255, and your annual gym membership of $360, in addition to your regular monthly expenses.

When you calculate your $400 sinking fund contribution amount, you include these two expenses.

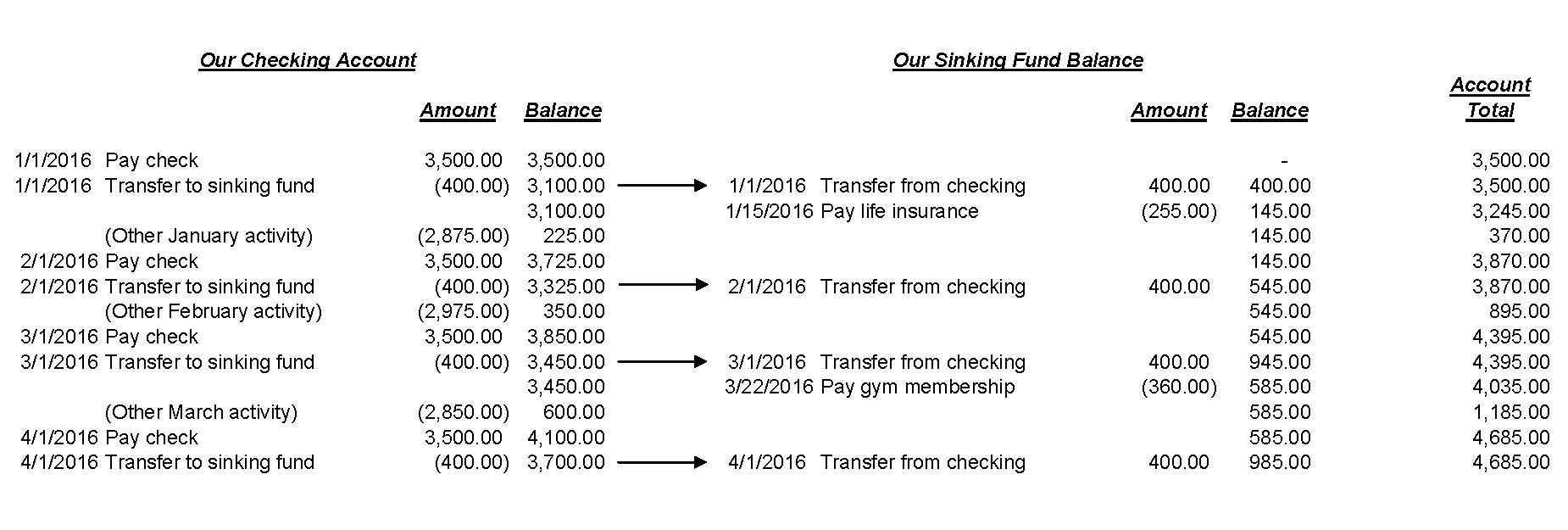

Your check register might look something like this:

Each month your paycheck is deposited on the first. Immediately $400 is transferred to your sinking fund. On 1/15/16 and 3/22/16, you paid the two bills being funded by the sinking fund.

Notice that those disbursements come from the sinking fund and not your checking account. Why? Because you’ve already set aside the money in the sinking fund! You no longer have to worry about how you’ll come up with the $360 for the gym membership when it renews! You’ve planned ahead and have money resting comfortably awaiting the time when it’s needed.

Where to Keep the Sinking Fund Balance Until It’s Needed

Some will choose to set up a dedicated savings account to transfer this amount to each month. Many banks will set up a free savings account and link it to your checking account, with easy online access. Ask your bank what options they offer.

Others, like ourselves, leave the money in our checking account, but we segregate it from the other spending money within the account. Allow me to explain: Notice in the case study above how the “Account Total” column to the far right didn’t change when the sinking fund was funded. Since the money is still physically in the same account, it wouldn’t change. When we complete our bank reconciliation each month, we’ll use the “Account Total” column instead of the “Checking Account” balance.

As with all financial issues, you’ll have to decide what works best for your situation.

How to Handle the First Year’s Sinking Fund

By now you might be asking: “How do we handle the first year’s sinking fund if bills come due before the money is available?”

This sounds like a complicated question, but it’s pretty straightforward.

Let me ask it this way: Using the earlier example of a $400 per month sinking fund, how would you handle a $600 bill that is due in January if you only had $400 set aside at the time?

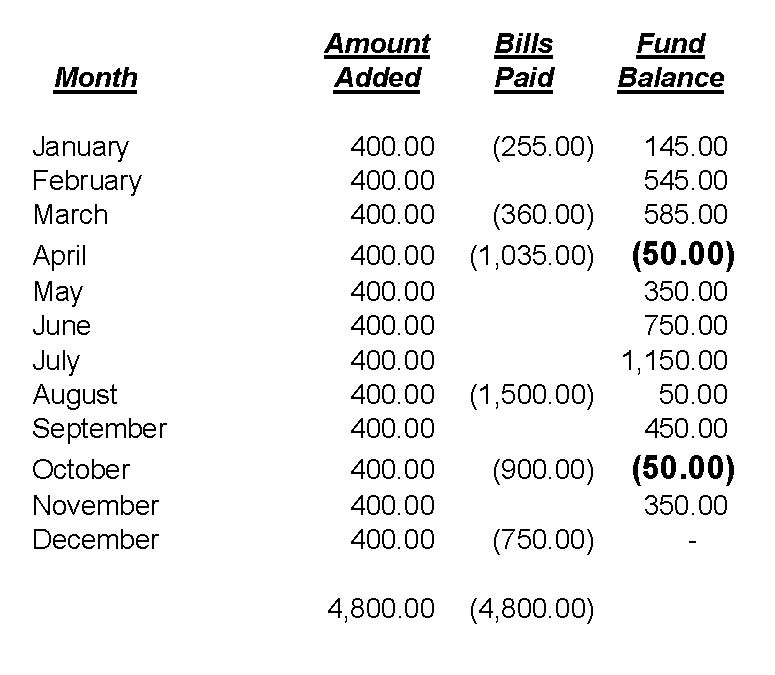

Suppose the actual payment schedule for the sinking fund items in our example were as follows:

You will note the $400 being added each month and the bills being paid throughout the year. Both total $4,800 as expected. However, in both April and October the sinking fund is negative! The total of the year-to-date bills due exceeds the amount contributed through that period of time.

Of course, we can’t have a negative sinking fund!

There are several possible solutions to this problem:

- Make a one-time initial contribution to the sinking fund to cover the shortfall. In this example, it would require a $450 contribution in January. Doing so would keep April and October from going negative.

- Bump up each of the contributions from January 1 to the first negative month by enough to cover the shortfall. In this example, adding $12.50 to each of the first four month’s contributions would eliminate the shortfall.

- Cover the shortfall from that month’s operating budget. For example, on your April budget, include $50 for Personal Properties Taxes and only remove the available money from the sinking fund.

The final option would be my personal preference, but again, you’ll need to make your own decision.

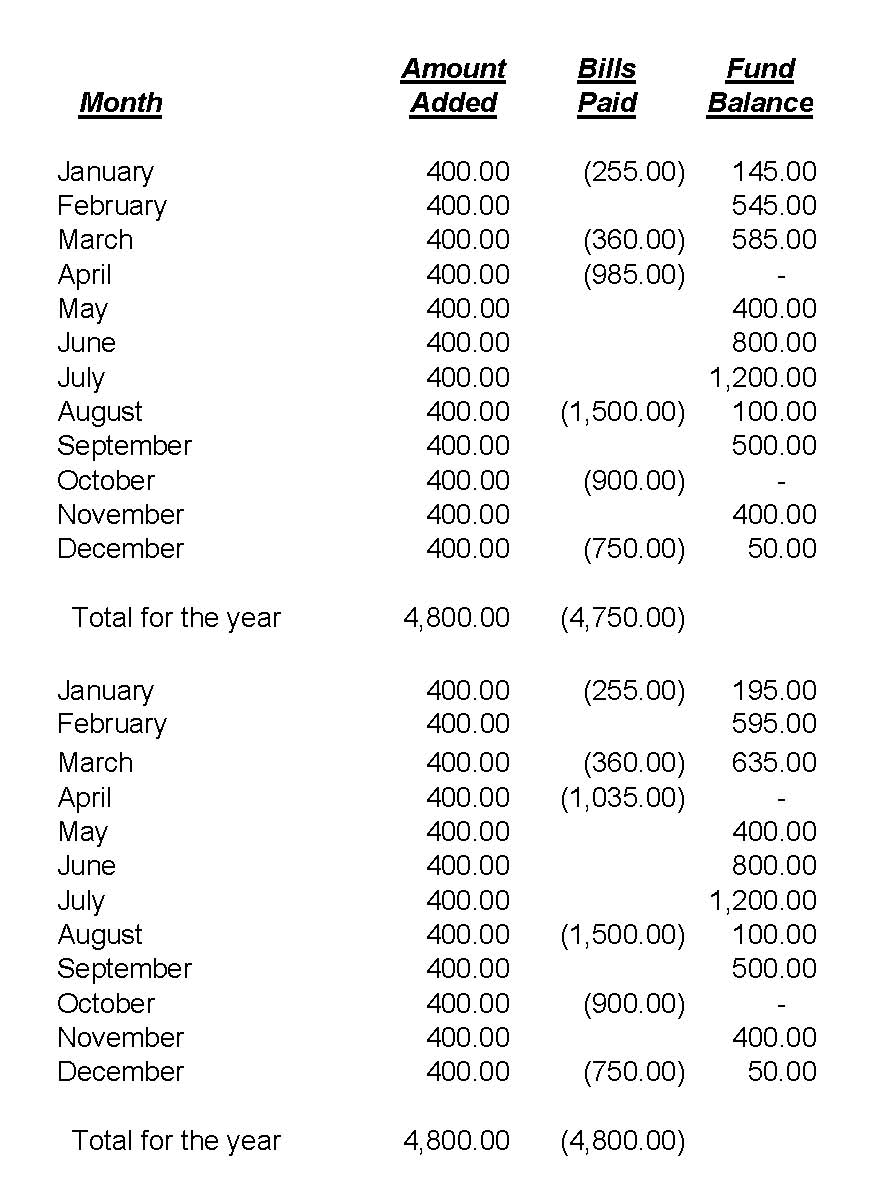

This is generally only an issue for the first year that you use a sinking fund. In later years, you should start the year with a “carry over” balance from the previous year to boost the balance high enough to cover large items early in the year. Continuing our example, here is Year 1 and Year 2 of the sinking fund balances (assuming you use option #3 above):

Notice in April of Year 1 that I only withdrew the available amount of $985.00. The other $50 needed for the Personal Property Taxes will have to be added to the April budget. By handling it this way, you’ll note the Year 1 December ending balance in the sinking fund is $50.00.

In April of Year 2, the full amount of the Personal Property Taxes is available in the sinking fund when they are due. Problem solved!

Conclusion

Sinking funds are a great way to smooth out your spending and avoid some of the stress that can arise due to irregular due dates for some expenses. While your amounts will surely be different from those in our case study, you should be able to easily determine the amount you should use.

Keep in mind that this is not an exact science. Surely your amounts won’t come out as evenly as I’ve shown here (I know ours don’t!). But with practice and determination, you too can develop a sinking fund strategy that works for your exact situation!

A sinking fund is an excellent way to avoid debt — it’s wayyyy too easy to use credit cards for a large and unexpected expense! Also, I think it’s important to keep a sinking fund distinct from an emergency fund — the two aren’t exactly the same.

I agree, Frank. Sinking funds are really a part of the budgeting process vs. funds set aside for emergencies. One you’ll use every month – the other you hope you’ll never use! Thanks for stopping by and commenting!

I’m really enjoying your posts John. Keep it up.

Thanks, Jim. I appreciate the kind words!