December 14th, 2021

Quick Stock Overview

Ticker: REGN

Source: www.stockrover.com

Key Data

| Sector | Healthcare |

| Industry | Biotechnology |

| Market Capitalization ($M) | $67,214 |

| Price to sales | 5.2 |

| Price to Free Cash Flow | 13.0 |

| Dividend yield | 0% |

| Sales ($M) | 13,543 |

| Net Cash per share | $26.15 |

| Equity per share | $160.48 |

| P/E | 10.0 |

| ROIC | 35.3% |

| Free cash flow/share | $48.10 |

Investment Thesis

A Great Complicated Company

I have only covered one biotech company (Vertex) simply because they are simply tough nuts to crack. A gaming company or a gold mine can be roughly understood with little research. Biotech products, however, are incredibly complex and technical. Regulatory conditions and sale processes are also complicating factors that usually cause me to look elsewhere.

This is even more true for actual “biotech” companies. It’s true, there are still a lot of old-school pharmaceutical companies in the pharmaceutical industry. Many of them were born out of the chemical industry. A chemical compound would be created to see if it could be used as a medicine. Chemical molecules came first, and finding a purpose for them was the general strategy. It is only a few hundred atoms in size, so a relatively simple product.

During the late 1970s, a new type of pharmaceutical company appeared, which I will call “true” biotech. Rarely do their treatments involve a chemical compound, but rather something of a biological nature. There is a specific protein, hormone, cell, etc… that can help cure or alleviate a disease.

Typically, such products are made of hundreds of thousands, if not tens of millions, of atoms. Due to its complexity and size, it requires a deeper understanding of the underlying biological mechanisms. Simply modifying a known theme will no longer suffice. Because of this, it is difficult to judge their treatment except by the most qualified specialists.

In spite of the complexity of “true” biotech, I cannot ignore it when the financials of a company shout “cheap!”. And sometimes the universe is guiding you.

When I decided to write about today’s company, Regeneron, news about the Omicron Covid variant came out and made the company even cheaper. I now had a double task on my hands. First, I had to determine the value of the business. Second, determine if the market panic about Omicron has affected the future value of Regeneron.

In an ideal world, the panic would provide us with a remarkably cheap entry point. I believe it does. But before that, let’s see what Regeneron has to offer.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A New Field of Medicine

A Science-Driven Company

The tech industry gloats about its innovative profile quite often. For Regeneron, however, it rings true. The company’s mission has always been to create scientific breakthroughs. The company achieved its first milestone in 1990 by being the most cited paper on neurobiology. Scientists have a way of thinking that is seldom emphasized by “normal” companies but makes perfect sense to them.

Both of its founders, Mr. Schleifer and Mr. Yancopoulos, are neurologists and molecular immunologists, respectively. The first FDA approval happened only in 2008, which demonstrates how tedious medical research can be.

Source: www.regeneron.com

Until the 2008 approval, the company had managed to stay afloat by contracting with large legacy pharmaceutical companies such as Sanofi and Bayer.

Since then, the FDA approval has kept coming:

- In 2011, EYLEA, an eye injection for age-related diseases.

- In 2015, PRALUENT, reducing the risk of heart attacks.

- In 2017, DUPIXENT (eczema) and KEVZARA (rheumatoid arthritis).

- In 2018, Libtayo, a drug to treat specific types of skin and lung cancers.

- In 2020, Inmazeb, an Ebola treatment.

- Multiple new indications have also been approved for most of these medicines since their initial approval.

Source: www.regeneron.com

A Unique Type of Treatment

Antibodies Treatments

Regneron progressed from very slow (and at times unsuccessful) drug development to a volley of successes and approvals. A huge part of the focus has been on immunobiology and antibodies, the field of expertise of the Co-Founder and now Chief Science Officer, Mr. Yancopoulos.

I won’t go into too much detail about the field in this report. I recommend a four-page document provided by Regeneron if you would like a primer. The final product is an antibody-based treatment.

The body uses these mechanisms to fight most illnesses (especially viruses). Vaccines work the same way. A vaccine is an antibody-based medicine, since it trains your body to make antibodies against a specific disease.

Regeneron has learned the art of manufacturing and converting antibodies into injectable forms to treat specific diseases that the body is unable to control on its own. This opens up the possibility of using antibodies to not only prevent, but also cure diseases.

Source: www.regeneron.com

The Potential

The targeting mechanisms of antibodies are similar to those of guided missiles. Either the antibody neutralizes its target directly, or it “tags” the target to be destroyed by the body’s immune system.

This ability to target is why it is considered one of the most promising fields for cancer treatment in the future. Cancer cells can be tagged with antibodies to be eliminated by the body’s immune system using custom-designed antibodies.

Since antibodies are naturally occurring molecules, the body tends to accept them more readily than exotic chemicals. They also last weeks or months, instead of hours or days.

We have mechanisms in our bodies that allow us to build distinct types of antibodies in response to new diseases. Therefore, you can replicate the process in the lab. This is how Regeneron developed its Ebola treatment and REGEN-COV for COVID-19.

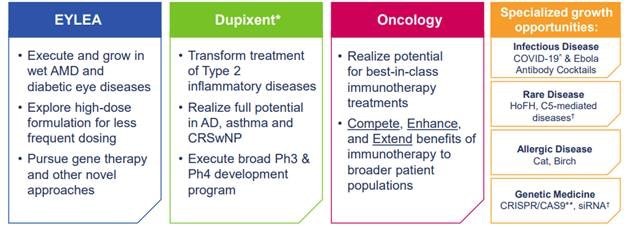

In the present, Regeneron has focused on the most promising or most needed antibody treatments. As a result, the company is now active in three fields: ophthalmology (eye medicine), oncology (for cancers of a very specific type), and inflammatory disease (like asthma).

The technology has a much broader range of potential applications. It has already commercialized solutions against infectious diseases (Ebola and Covid), and many more are on the way, which will be discussed in the R&D chapter.

Chapter 2: The Drugs Lineup

As all Regeneron’s value is derived from its treatments and patents, this report will focus heavily on its approved and in-development treatments.

The Existing Treatments

Covid

How could a biotech company report these days not mention Covid? Since I mentioned earlier, the company has a Covid treatment, which may or may not still be effective against the newly discovered Omicron variant. In response to a possible resistance to the new variant, the stock of the company dropped 5% in one day.

First, let’s discuss something. Covid is probably here to stay. Vaccination does not seem to fully prevent its spread. Moreover, anti-vax sentiment will prevent vaccination campaigns from reaching their full potential.

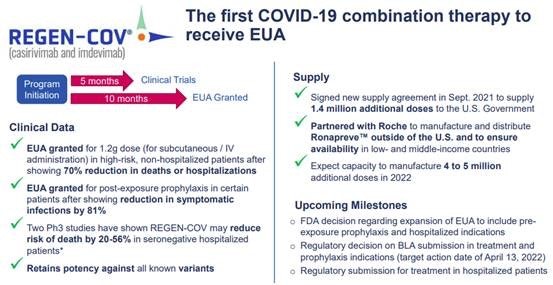

In order to reduce death and hospitalization, we need actual treatment. With REGEN-COV, Regeneron reduces deaths and hospitalizations by 70%. We will need this kind of treatment to turn Covid into a manageable problem, one that can be solved without lockdown and further restrictions.

Governments around the world seem to agree, with 4-5 million doses expected in 2022. The distribution will be handled by Roche. If 2022 is anything like 2021 (I hope not), I would expect 2023 to be a banner year for COVID-treatment.

What about the resistance to Omicron? The recent mini-panic is unwarranted, in my opinion. First, Regeneron developed this treatment from scratch within a year. Since then, it has been successfully tested for safety. Only additional tests will be needed to determine the effectiveness of the tweak against Omicron, so the process will be sped up.

In addition, if there are new resistances (something we are not yet sure of), a redesign will be quicker than figuring out how to make an antibody cure from scratch for a disease we don’t yet know. In other words, I fully expect Regeneron’s headstart in curative Covid treatments will allow it to keep up with new variants as they emerge.

In fact, new variants and constant updates and new orders for the last version of the treatment will boost sales. Once again, I think Covid will stick around, so Regeneron’s income from it will be more durable than what markets are pricing in.

Other Infectious Diseases

Regeneron also developed a drug to fight Ebola, a disease that can kill up to 50% of its victims. The Covid treatment was developed so rapidly thanks to this research.

With Covid, what at the time looked like an unprofitable area of research has become a cash machine and reputation booster. An example like this exemplifies brilliantly how science-driven companies use technology platforms and data as their most valuable assets. I will elaborate on the value of the research tools and data in chapter 3.

Currently, Regeneron does not appear to be pursuing any other diseases in its research pipeline. Nevertheless, I like the ability to produce quick treatments in case of new and unexpected situations. Covid taught us that modern biotechnology can turn out innovative treatments at an unprecedented rate.

Eyes Treatments

A treatment that prevents people from becoming blind is of priceless value to those affected.

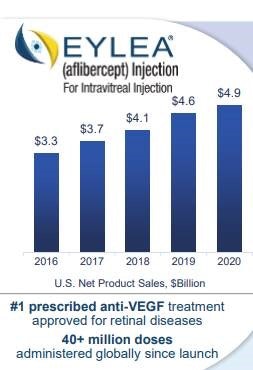

Product sales have grown steadily by 5-7% every year through the Bayer distribution network. For some patient categories, Regeneron treatment has demonstrated that it can prevent vision loss in 75% of cases. These drugs should have a steady market for the next decade.

Inflammatory Diseases

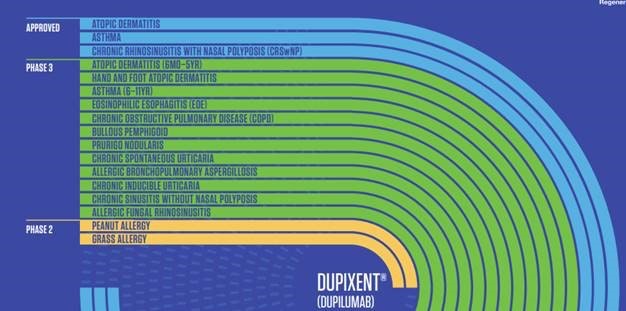

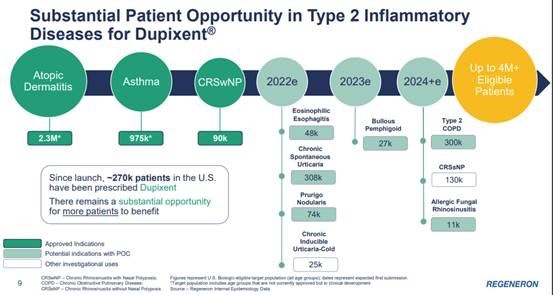

Many diseases are caused by abnormal inflammation, from allergies to skin rashes and chronic respiratory and digestive issues. Antibodies play a part in regulating inflammation, which is a central aspect of immunity. Duxipent has been approved for three applications so far, including regulating inflammation of the skin and respiratory system.

The effectiveness of the drug is now being tested for 14 other diseases, including asthma, food allergies, and pollen allergies.

In just one year, Dupixent sales have grown by 55%. The drug is going to grow very quickly, both from new approvals and wider use of already approved treatments.

A 50-100% increase in Dupixent’s revenue is expected by 2024. This is BEFORE we get news about the effectiveness in selling serious, but very common allergies such as peanut, cat, and pollen.

Oncology

Regeneron’s main cancer treatment revenue grew by 80% in one year, and it is only now expanding outside the U.S. We can expect explosive growth here as well. The treatment has been validated for some skin and lung cancers, and there are more trials to test it for other types of cancer, like cervical cancer. In the research portfolio section, I will discuss Regeneron’s full potential in cancer treatment.

Overview

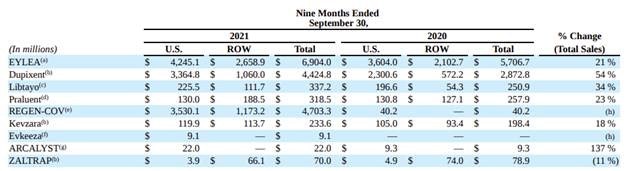

As of now, the main revenue driver is EYLEA, the ophthalmology treatment. Given that it is the oldest drug in the company, it makes sense. Until recently, Dupixent had the second-highest revenue.

Both drugs are still growing quickly, especially Dupixent with a 54% year-to-year jump. And that’s before it’s used for other diseases like asthma and cat allergies.

In the last 9 months, the Covid treatment (REGEN-COV) has significantly boosted the bottom line, accounting for a quarter of total revenues. The majority of revenue comes from the United States, with the rest of the world (notably the EU) only recently approving the treatment. A wider geographical reach and a move away from a vaccine-only approach should provide very strong support for REGEN-COV sales.

The Research Pipeline

First, A Small Recap

Let me sum up a little before I delve into the most complicated part of the company. Regeneron’s current product lineup focuses on eye treatment, inflammatory diseases, and oncology. Covid recently introduced a 4th “infectious disease” segment to its business.

Each of the existing drugs is showing aggressive annual growth, with a lot more applications and diseases to follow in the next 1-3 years. On its own, this is the simplest part of the company to understand.

There are multiple diseases for which these products are already approved. In light of their proven safety, the only problem connected with clinical trials could be low efficacy. As a result, a lot of the research effort is de-risked, so it is likely that clinical trials will be successful. Expect an approval rate of 50% or more.

In this section, we get a pretty solid picture of how well the company is doing, with growth coming from approved and well-understood molecules. Let’s talk about the newer drugs in the portfolio.

The R&D Pipeline

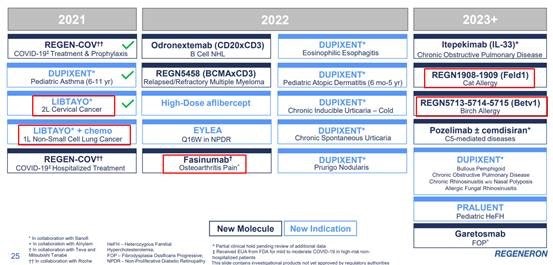

Regeneron is working on a bunch of upcoming drugs, and also on various applications and modifications for its approved drugs. In the diagram below, I highlighted the existing drugs in red. All the others are potential breakthrough treatments.

You can tell at a glance what company’s future focus is by the color-coding. Phase 3 trials are the most advanced and most likely to be approved. I believe this will strengthen the business, especially in the inflammation segment. This covers Cat and Birch allergies, 2 not-life-threatening but also very common and potentially very lucrative conditions.

Phase 2 trials are using molecules that have proven safe, but we aren’t sure if they work on real patients. Regeneron is trying to break into a brand-new line of business, hematology. There’s a whole business section for it.

Guessing the future success of clinical trials is a fool’s errand, especially in the first and second phases. Not even the scientist working on it every day can guarantee success. Therefore, investors shouldn’t bank on these outcomes. It’s better to rely on general probabilities. Nevertheless, with 8 different molecules being tested, at least 1 or 2 should work well.

Also, Regeneron is testing a whole bunch of new molecules for treating cancer thanks to its growing success in oncology. Oncology has the highest failure rate when it comes to developing novel treatments, so I expect maybe one of these will make it to market. Using Libtayo as a template, this could generate at least a few hundred million dollars in extra income.

Here’s Regeneron’s slide about when to expect news about its multiple clinical trials. I highlighted the most interesting ones in red.

Cancer treatments are critical because they’re likely to be very profitable. In the future, these studies could also help develop better cancer drugs.

I also highlighted the other three because of how big their addressable market is. Osteoarthritis pain is going to keep growing thanks to the aging population. Cat and birch allergies are so common that Regeneron’s revenues would surge up if they found a treatment.

The rest of the research pipeline isn’t bad either, but shareholders should probably pay attention to the news on either the most lucrative or the most addressable markets.

Chapter 3: The Hidden Asset: The Research Platform

How Did They Do It?

In my introduction, I talked about how Regeneron had contracted its research platform out to big pharma companies to survive its early struggles with drug approval. That platform formed the foundation of its later successes.

Earlier, I gave you an overview of Regeneron’s existing treatment and research portfolio. We can then guesstimate the growth in the next 2-5 years. In addition to that, it’s the ability to keep innovating that will drive future revenue.

Regeneron has built an entire treatment discovery process over 30 years. This is the company’s most valuable asset, as its competitors could not replicate it in less than 10-20 years. In order to do this, you would have to recruit the right scientists, select the right cell lines, identify the right targets to develop antibodies for, and develop the tools and software to analyze them.

The Process

The whole process is explained in multiple videos here, so if you want to find out more, check them out. Here’s a simplified version:

1) Animal testing

With Velocigene and Velocimouse, Regeeron scientists can discover the function of thousands of genes previously unknown, as well as create genetically modified mice to find new treatments. This gives the research team original ideas and speeds up the discovery process.

2) Human antibodies

When a mouse target is found, a human antibody needs to be developed. Velocimab and Velocimmune provide a platform to make large quantities of human antibodies by modifying lab-grown cells and mice.

3) Clinical trial

Once enough of the product has been made, clinical trials can begin. Phase 1 tests safety only, phase 2 the medical potential, and phase 3 the efficacy in real patients.

4) Mass production

Whenever a drug is approved, Regeneron sets up a factory to mass-produce antibodies. As antibodies are very complex products, they’re made from genetically modified cells or mice, so the process isn’t easy. Experience is another key asset that’s nearly impossible to replicate.

The Genetic Database

To expand beyond animal genetics, Regeneron will use an extensive human genomic database, the Regeneron Genetic Center, to find breakthrough ideas. The center has now gathered its 1,000,000th exome (the part of the genome that turns into protein in the body).

Genetic data combined with de-identified medical records is the world’s biggest data set of its kind. The idea behind gathering so much genetic data is to find the common denominator between people with the same disease. This should lead to more effective treatments.

During the past decade, genomic technology has exploded, supporting Regeneron’s efforts in the domain. The project’s first target was just 20,000 exomes. That’s now the weekly target. Going forward, Regeneron can add another million exomes every year.

Earlier, I said the Velomab, Velocimmune, etc… were Regeneron’s best kept secret. As these are already used at full speed to develop and test new drugs, it’s mostly true. I think in 5-10 years, the visionary decision to collect a huge dataset of exomes started in 2014 will prove to be the driver for new discoveries. Regeron is very data and science-driven, and it shows.

Chapter 4: Financials & Valuation

Financials

Of course, none of these qualities would matter if Regeneron’s price was too high. Quality is critical, but so is price.

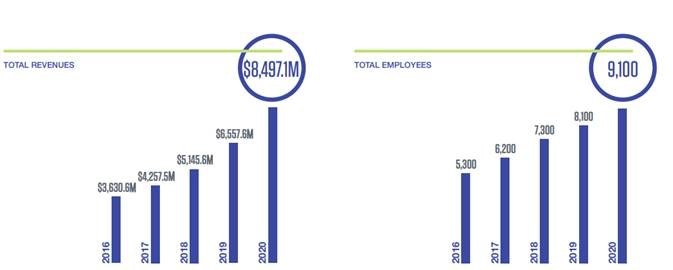

Regeneron is known for its aggressive growth. The company has almost tripled its revenue in five years. In the same timeframe, the company has also invested in extra capacity, nearly doubling its employee count.

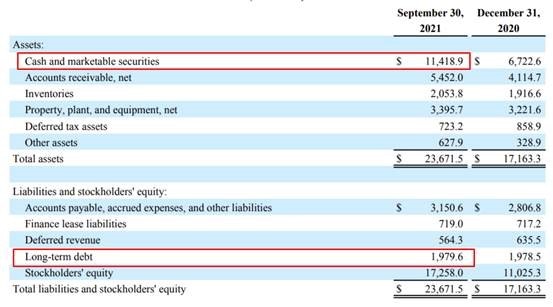

Often, biotech companies have to enter into heavy debt to fund their growth. This is This is because R&D for products that will be profitable after three or five or seven years is tricky to finance. Here, it doesn’t matter because of exploding revenues. We have twice as much cash as we do in liabilities. Furthermore, it provides a healthy cash cushion to cover the cost of all trials.

I also appreciate the conservative approach taken to the balance sheet, with no significant intangible assets that can be challenging to understand. I think it might even be a touch conservative since it ignores the patents, the immunology platform, and the exome database, which are obviously very valuable.

Most of the revenue gets reinvested back into the business, especially in R&D. That’s $2.7B of R&D investment, or 32% of total revenues.

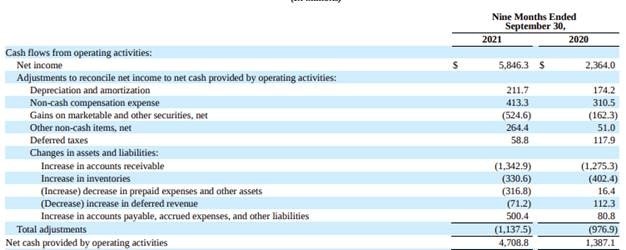

Sales and cash flow are up compared to 2020, partly because of new treatments and partly because of the emergency approval for Covid.

The company doesn’t pay dividends, but buys back shares, and has stepped up re-purchases in 2021. Stock repurchases have broken a long-term trend of increasing share count.

Valuation

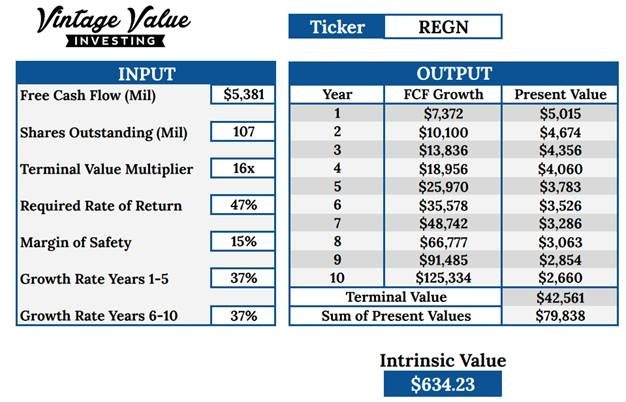

Discounted Cash Flow (DCF)

In the past, the company price to free cash flow ratio has been on the decline, but this partly reflects the lack of free cash flow until 2017-2018. Given the company’s growth profile, 13 is too low and I’d prefer 16 which is still conservative.

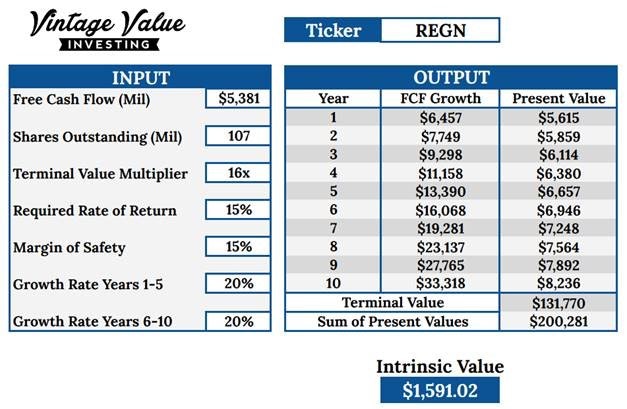

Most of the multiple depression has to do with a quick increase in cash flow related to the commercialization of Covid treatments (from 2,004 to 5,381). This is the good kind of multiple compression!

Due to so much cash flow coming from Covid-treatment, I’m running two DCF calculations, one with 2020 numbers and one with 2021 numbers. This way we know how valuable the core business is outside of the pandemic effect, which may or may not be a sustainable business line.

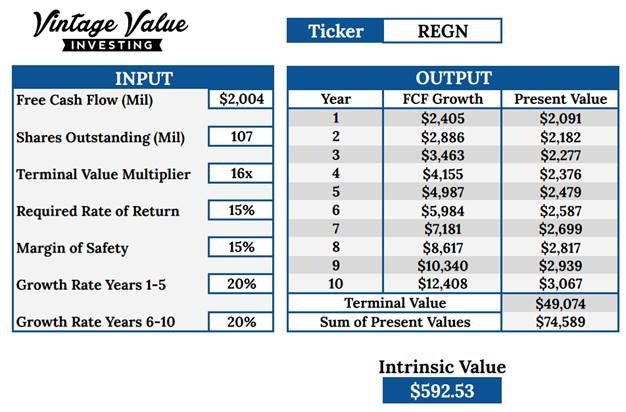

DCF with 2020 numbers

DCF with 2020 numbers

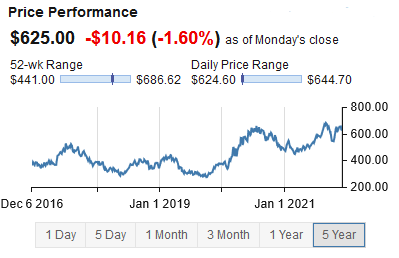

I was a bit shocked when I got the results. Even if you ignore Covid’s income, which is very conservative, it seems undervalued. It seems like a bargain at the current price of $625 per share.

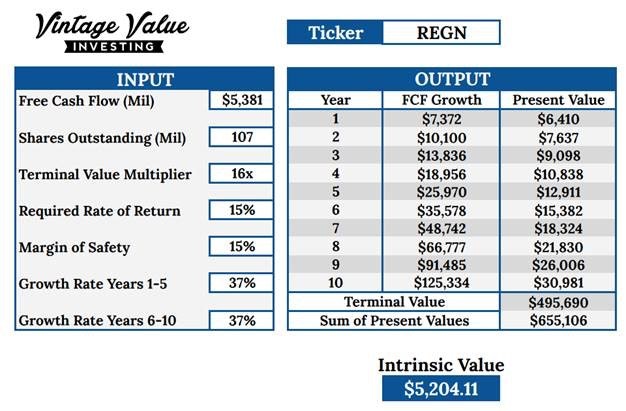

What’s even more shocking is that I used a 20% growth rate of free cash flow. The actual historical growth rate was 37%. The company probably can’t keep up with this, but if you want to see a wild bull case, here is what it would look like:

What kind of return would that be? A whopping 47%! This is really reaching the limit of valuation methods and I totally don’t expect this to be Regeneron’s future. On the other hand, that’s a pretty reasonable expectation of 15-20% yearly return.

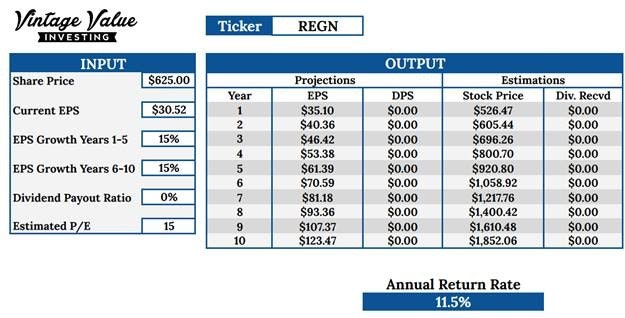

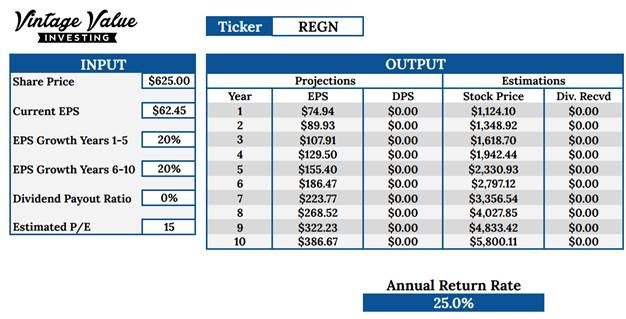

Earnings Growth

Here too, I’ll calculate with the pre-Covid treatment and post-Covid numbers. Over the last 10 years, earnings have grown 28% a year. Let’s take a more “conservative” 15% – 20%.

Earnings Growth with 2020 numbers

Earnings Growth with 2021 numbers

As you can see, using 2020 or 2021 changes everything.

From both DCF and earnings calculations, I’m estimating 11%-15% return for 2020, and 25-27% with 2021’s earnings and the Covid treatment.

The reality will probably be somewhere in between. 2021 wasn’t all about Covid treatments, and the main products are still doing well. In a few years, Covid will probably fade away (I hope so). By introducing new drugs, growth should remain strong regardless of any Covid-related events.

Conclusion

I’m still a bit confused by Regeneron’s current valuation as I finish writing this report. As far as I can tell, the company just seems to have grown its revenue and earnings faster than its valuation. Considering that the valuation is close to the all-time high, it can be said that the market hasn’t re-rated the company yet.

With so much attention on Covid, it’s easy to forget about the rest of the company. There’s skepticism about Covid income’s sturdiness. That 5% drop in a day shows that REGEN-COV might not be that effective against Omicron.

Obviously, that’ll hurt short-term results. However, with the company’s demonstrated ability to quickly develop antibodies for Covid, it might actually be able to compete on equal terms with vaccines that had the first-mover advantage. So, overall, not much of a concern.

The company’s research portfolio is another strength. As I said before, guessing clinical trial results is a fool’s errand. What’s more significant is the process the company developed to build this portfolio in the first place.

By focusing on one kind of innovative medicine (antibodies), Regeneron has become a leader in its field. The company can leverage its patents with big pharma’s distribution network.

They have world-class immunology knowledge, and it’s just starting to come to fruition. The upcoming entry in hematology, an entirely new field of application for Regeneron, is a great example. I’m sure there’s other applications in neurology, pneumology, etc… that are still unexplored. Some are just getting started, like oncology.

Last but not least, platforms like Veloci-X and initiatives like collecting 1 million exomes will allow Regeneron to stay ahead of its competition.

Current valuation largely ignores the company’s long-term growth potential and discounts quite a bit of its Covid drug’s potential. I think both of those are wrong.

First of all, the number of Covid cases is trending up in heavily vaccinated areas like Gilbraltar and Portugal, which means symptomatic treatments need to be increased too. This should be a boon for REGEN-COV in the US and worldwide.

Additionally, Duplient’s applications for common allergies should boost the company’s income regardless of the pandemic.

Investors should keep an eye on the following:

- REGEN-COV ability to keep up with variants

- Extension of Duplient to new applications, especially the one with a large addressable market like common allergies.

- When will EYLEA’s revenue plateau?

- Results from the new drugs clinical trials, especially success or failure of extra cancer drugs and new hematology drugs.

Regeneron growth is cheap right now, and for long-term investors, this could be a compelling entry point.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in REGN and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.