July 4th, 2021

Quick Stock Overview

Ticker: QIWI

Source: www.stockrover.com

Key Data

- Sector: Technology

- Sales ($M): 553

- Industry: Information Technology Services

- Net Cash per share: $6.87

- Market Capitalization ($M): 667

- Equity per share: $7.03

- Employees: 2,865

- Debt / Equity: 0.2

Summary

Qiwi is the leading provider of online financial services that you are very unlikely to have heard about. The reason is because Qiwi is leading in Russia and CIS countries. Just to refresh your memory, the CIS countries include multiple former USSR countries, but not most of central and eastern Europe.

Source: www.xprimm.com

Strategic Analysis

Fintech and Regionalization

The iInternet has revolutionized countless industries, including the finance sector. Fintech startups have been around for a while, with the first giants like PayPal making the explosion of e-commerce possible in the first place.

But now, Fintech companies are looking beyond building bridges between web shops and the financial system. They are actively looking are replacing the incumbent financial system. This can be things like bypassing banks for currency conversions and trans-border transfers, like with Wise, or even trying to create a whole new monetary system like with Bitcoin.

The leaders in Fintech (and Tech in general) have for a long time been American. The rest of the world was significantly lagging in iInternet adoption or lacked the critical size to develop quickly enough. With the rise of mobile internet and the worldwide omnipresence of smartphones, this has changed.

Many markets have proven difficult to penetrate for the American giants, especially the Russian and Asian markets, due to regulatory, cultural, and linguistic reasons. This has allowed for local companies to become locally the winner-take-all in their respective markets. For example, think of China with Alibaba instead of Amazon, or Didi instead of Uber.

The same happened in Russia, with the younger part of the population looking eagerly to new mobile-centric offers, bypassing the national banking dinosaurs. Many use PayPal or other similar offers for international services, but the network effects mean that locally, everybody will also use and share with each other more local solutions, adapted to the local market needs and problems.

A Precursor in Russian Fintech

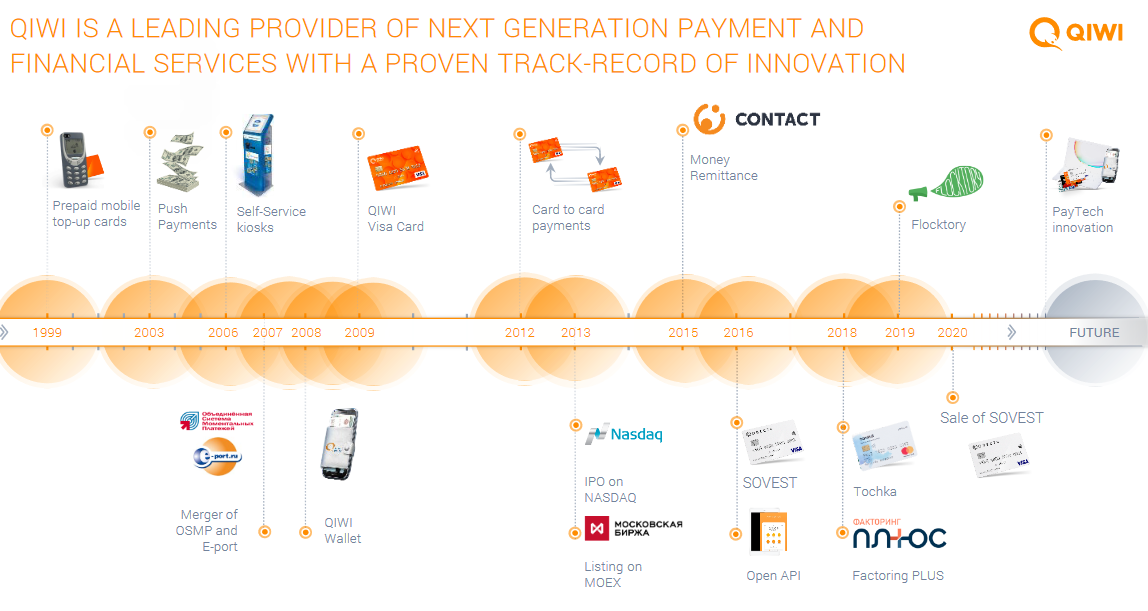

Qiwi might not be well known in the west, but it has been operating at the edge of mobiles services since 1999, starting with prepaid mobile cards. It then slowly expending to self-service kiosks, wallet app, card payments, consumer loans (SOVEST), and more recently the B2B and gaming market.

The timeline below gives you an apercu of the delayed penetration of smartphone services in Russia. Qiwi was and still is at the center of it.

Source: https://investor.qiwi.com/

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

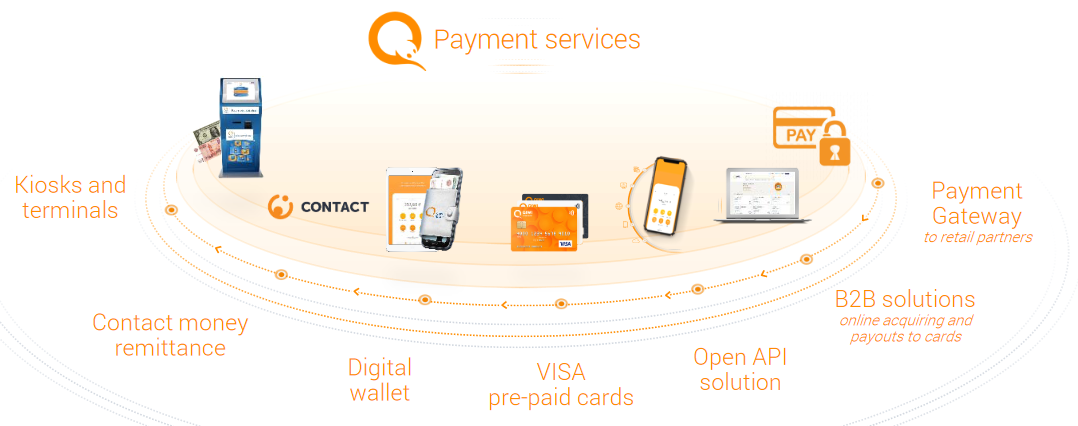

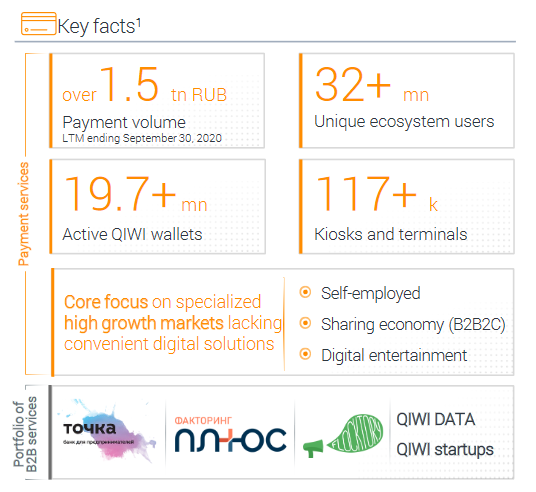

Qiwi main services are centered around payment services, offering a large spectrum of solutions. Users can use kiosks or digital wallets to transfer money, pay an invoice or use prepaid VISA cards.

Source: https://investor.qiwi.com/

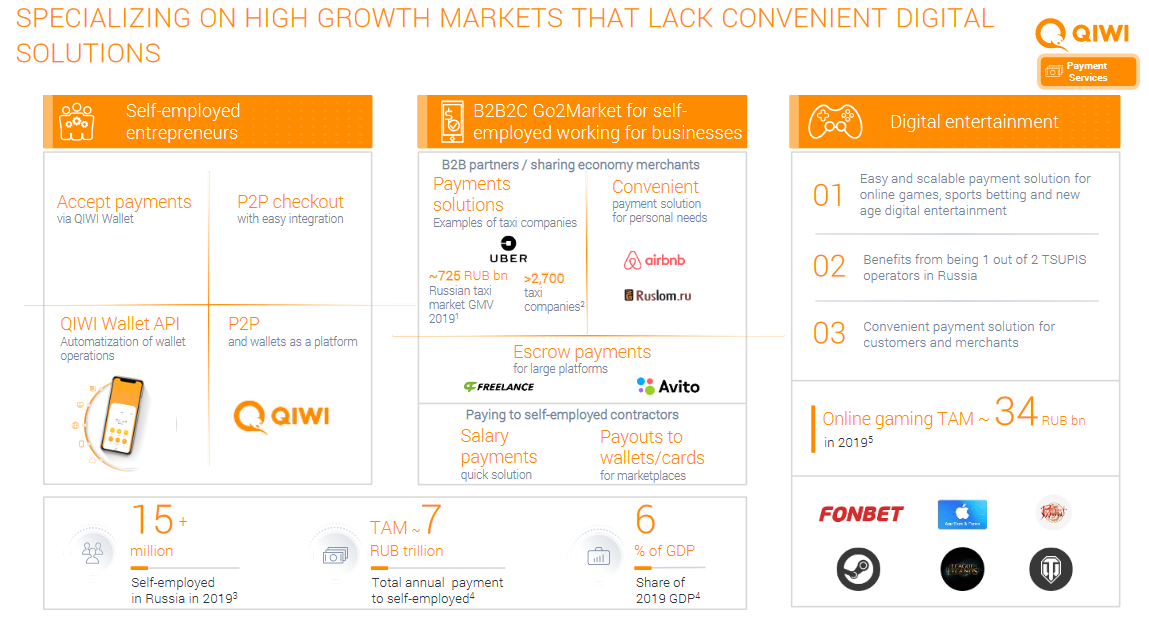

Qiwi has 32 million unique users, of which 20 million use actively the Qiwi wallet. They performed a total of 1.5 trillion RUB transactions in 2020 ($20B). Qiwi is active in many segments online financial transactions but have a focus on 3 segments: self-employed entrepreneur and gig-economy workers, digital entertainment (gaming and gambling), and B2B.

Source: https://www.investor.qiwi.com/

Source: https://investor.qiwi.com/

Now, let’s dig a little deeper into Qiwi’s products.

B2C Offers:

Digital Wallet: The digital wallet is the crossroad of Qiwi ecosystem. It is used by e-commerce merchants to bill their own clients. And individual users can use it to transfer money or getting cash out at one of the 117,000 kiosks and terminals. Users also get access to VISA cards or to get cashback bonus on their spending. Of the 30 million users, the 20 million using the digital wallet are likely to be the ones truly engaged in Qiwi ecosystem.

Entertainment: Qiwi operates several online casinos and also allows its users to purchase video games on all the majors gaming providers and platforms. The business model is pretty straightforward, it takes fees from the gambling spending and video game purchases.

B2B services:

Qiwi offers 3 different services to companies.

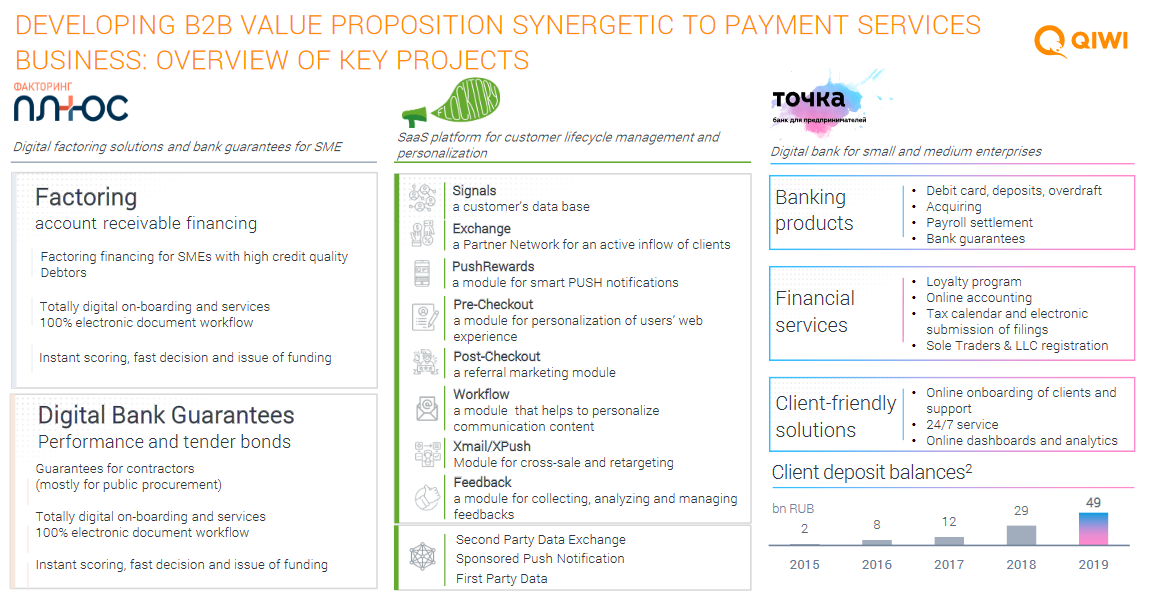

Flocktory: a social media-focused marketing platform. The key idea of this SaaS solution is to allow e-commerce customers to promote a merchant via social media and to get a reward if their friends make a purchase. The company was purchase by Qiwi for $11M in 2017.

Tochka: an online bank for SMEs that made a partnership and joint venture with Qiwi in 2018. Tochka main sale point is to offer ” All your company’s accounts, cards, balance and bookkeeping in one screen. Statement in one click”. Tochka is among the top 10 Russian banks by assets and seems a good fit for the Qiwi ecosystem of e-commerce and entrepreneur.

FactoringPlus: This branch offers factoring financing, allowing companies to get credit depending on their yet-unpaid invoices. Thanks to the in-depth data on its B2B clients’ finances (from Flocktory, Tochka and wallets transactions), I think Qiwi can make a pretty good decision on the factoring risks.

One last business was a loan department, Sovest, but this has been sold recently, so will not count in Qiwi’s activities anymore.

Regulatory Risks

Fintech companies are trying to disrupt a highly sensitive and regulated industry. Hence, they run face two different risks.

First, they risk lobbyists from the established banks managing to push for damaging new regulations and legislations. In countries with a weaker rule of law like Russia, this is a real concern.

Secondly, because they operate new business models, usually light on paperwork and user checks, they risk having problems with the regulating authorities. KYC (Know Your Customer) rules are very strict to avoid money laundering and other illegal activities, and Fintech is in danger to be used for illegal money transfers. So, every Fintech company has to balance out easiness to use and user-friendly systems with regulatory risks.

Regulatory Troubles

And this seems to be exactly the problem that Qiwi has recently run into. The stock price is now cheap, and this is the main reason. We will discuss further in the conclusion what to think of it, but let’s first look at what happened.

The Central Bank of Russia (CBR) has fined Qiwi $150,000 for “insufficient reporting and record-keeping requirements”. More serious, the CBR also announced “the suspension or limitation of most types of payments to foreign merchants and money transfers to pre-paid cards from corporate accounts”.

So, pre-paid cards for companies and foreign merchants are for now off-limits for Qiwi. This is a serious blow to their operations, reputation, and growth. Since then, the CBR has allowed Qiwi to resume operations with some key foreign companies and reduce some restrictions, but not all. This result in a 2021 decline in revenue of 15-25% and net income of 15-30%. Not a death sentence, but for sure a serious problem.

The company essentially claims this is the result of an increase in the CBR scrutiny of electronic transaction in general and not a problem with Qiwi in particular. While this might be true, I am somewhat skeptical of it. We will discuss the possible consequences and scenarios in the valuation section.

Economic Moats

In value investing terms, moats are what allows a company to keep a hedge against its competition for a longer time.

Large And Interconnected Ecosystem

The main moat for Qiwi is its very diversified ecosystem. A Qiwi user might start using it for buying a game on Steam, or to send money abroad. But he will then also use it when he starts to drive for Uber or set up an e-commerce platform. Or he might talk to his boss about the factoring financing or the Flocktory ERP. The company can leverage many entry points for its users and expand from there.

By being the historical leader in digitalization of finance in Russia, Qiwi can leverage a powerful brand and have its users stay in its ecosystem for most of their online transactions.

Switching Cost

Qiwi users have used the company’s services for many years. Simply put, their online life is so entangled with multiple Qiwi services that switching to a competitor would be a huge hassle. So as long as the company keeps delivering even just an “ok” service, most of its users will stick to it. This is especially true for the most profitable users that are using Qiwi the most. Added to the complexity of the Russia and CIS markets, this means very few competitors can be expected to emerge and try to steal Qiwi users.

Competition

Besides some foreign competitors like PayPal, not very active in Russia and CIS countries, Qiwi faces competition from mostly 2 companies.

Yandex

Yandex is the Russian Google and at the same time the Russian Uber. Yandex is by far the most impressive Russian tech company and is expanding aggressively abroad, especially in Eastern Europe. It has its own set of digital wallet and payment services and very high technical skills. I am not really sure how much of a threat Yandex is to Qiwi.

Yandex has for sure more firepower and is overall a stronger company. But it is also very much distracted by other ventures, with search engine, self-driving car, ride-hailing, food delivery, music streaming, e-learning, cloud computing, delivery services, etc. Digital wallets and such are really just an afterthought for the Russian tech giant, barely even mentioned in their investor presentations.

Sberbank

Sberbank is the largest and most powerful bank in the country. This also meant for a long time it was slow-moving, bureaucratic, and mostly focused on its political connection more than technology. This is changing slowly, and Sberbank online is now a thing.

However, the very nature of the company makes me think it will be slow to react and move against more tech-savvy and agile competitors like Yandex and Qiwi. Sberbank is for larger business and older people, while Qiwi is for younger generations, freelancers, and small businesses.

Management

Management of Qiwi is for me one serious black mark on the company and echoes the recent problems with the regulatory authorities. For all companies, (especially financials) a quick turnover of management might warn on incoming trouble. Qiwi seems to illustrate this case well.

The CFOs

Several CFOs worked at Qiwi in a short period of time. The last resignation is from last March (he was appointed in November 2020). The same sequence of hiring and resignation happened in 2019, between June and October. A possible cause for such quick CFO turnover is that the new hire gets to know the company’s inner workings and realizes he does not want to have his reputation covering some malpractice of some sort. Once, it could have been indeed a personal reason, or just a bad hire. Twice, and there seems to be something suspicious going on.

The recent penalties by the CBR seem to indicate that indeed, Qiwi was not keeping a proper record of everything. I will discuss in the conclusion the risks associated, but overall, the news about the CFO position was a warning about troubles to come.

Elena Nikonova, QIWI’s former Deputy CFO for Financial Reporting is now the interim CFO. She is a former Ernst & Young consultant.

Andrey Protopopov, CEO

Recently nominated, he was proposed for the position by the board in March 2021. Mr. Protopopov was before Qiwi’s Head of IT and product since 2013, after 12 years working for Procter & Gamble. Maybe more relevant than his profile is who he replaced. The previous CEO was the founder and majority shareholder Sergey Solonin.

It looks to me like the board has gotten enough of the malpractice that led to the sanctions by the CBR and pushed instead Mr Protopopov to clean the house after the resignation of the last CFO to date. As an insider of the company with a technical profile, he is likely to know where to start and what to do.

Quantitative Analysis

Financials

Generally, I look at the last full financial years for easy comparison and avoiding seasonality. But with the recent sanctions and the effect of COVID on 2020, I will mostly rely on the last quarter to look at the ongoing situation of the company.

Revenues

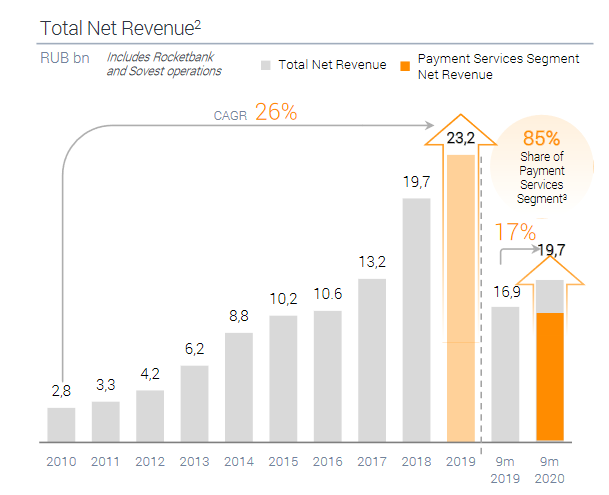

Total revenue has for the first time seriously decreased, but 18%, to $68.2M. In the last quarter report’s own admission, the decline was mostly due to the loss of high-yield cross-border e-commerce transactions. Interestingly enough, payment volume has still grown thank to a strong performance on the money remittance activity.

This breaks a pattern of strong and steady revenue growth, multiplied 10-fold since 2010.

Despite declining revenue, net income has increased by 18% at $27.2M. The increased revenue comes mostly from a decrease in personal, administrative, and general costs. The decrease in costs was largely due to the sale and divestment of Solvest and RocketBank, a banking operation which were not profitable and that Qiwi will probably be better off without.

It is worth noting that this is with a loss of $5.5M in the B2B activities, due to aggressive marketing and business development costs. This seems to bear fruit in business growth if not in profitability, with for example a +50% increase in revenues for Flocktory year-to-year. Only the future will tell if they will be able to turn profitable or be like the failed Solvest venture.

Dividends

Dividends are one strong point in favor of Qiwi. With the recent decline in share price, the growing dividends are now at a very high level of 8%. And contrary to a company struggling financially but refusing to reduce dividends, Qiwi’s earnings are sufficient to cover the dividends. In fact, dividends have a history of following closely the company earnings.

The recent increase in earnings per share might indicate that dividends still have room to grow, especially considering the cash war-chest of the company.

Source: www.finbox.com

Debt and Balance Sheet

Qiwi’s balance sheet is what got my attention about it in the first time. If the company was just a growing Fintech at a temporary discount, I would have only been moderately interested.

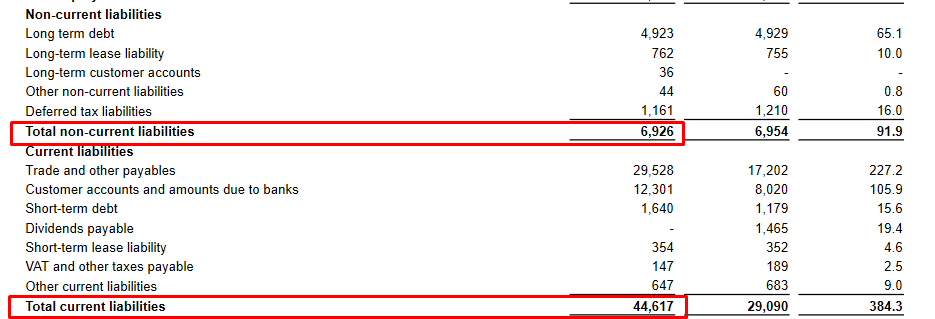

As surprising as it might be for a financial company, Qiwi have actually no debt to speak of. And it mostly retained all the extra cash that was not distributed in dividends. This led to a constant improvement of the net debt, now at -$539M. This is a remarkably negative net debt when you consider that Qiwi current valuation is a market cap of $667. So, the whole business, net of cash and debt, is really valued at only $128M.

Source: www.finbox.com

If you want to look a bit more in detail, see below the full balance sheet, where cash (47 billion RUB) is almost enough to cover the entirety of the liabilities (51.5 billion RUB).

Cash Flow

Qiwi cash flows have been almost constantly positive for a decade (the only negative moment being the 2015 Russian recession from oil prices crash), but somewhat irregulars over time. I think this reflects the periods where the company investing strongly in new operations like the now divested Salvest.

Source: www.finbox.com

To assess the quality of capital allocation, we can look at various ratios, like returns on invested capital, equity, and assets.

Qiwi’s returns on most metrics are very good, including on capital, invested capital, or equity. A persistent level of 20-30% or more has been the norm of the company, including during the period under sanction by the CBR.

Source: www.finbox.com

Categorization and Valuation

Investment Category

Qiwi is hard to qualify, as it mostly depends on the opinion about the future of the company. On one hand, it is first a value company, as it is currently very cheap, especially if compared to net income and the quality of its balance sheet.

On the other hand, it is or is not a quality growth company, depending on one aspect. That is if the new CEO manages to clean up the house and avoid further regulatory troubles. The company has delivered in the past high-quality results on growth, return on capital and dividends. Will it manage to do so in the future?

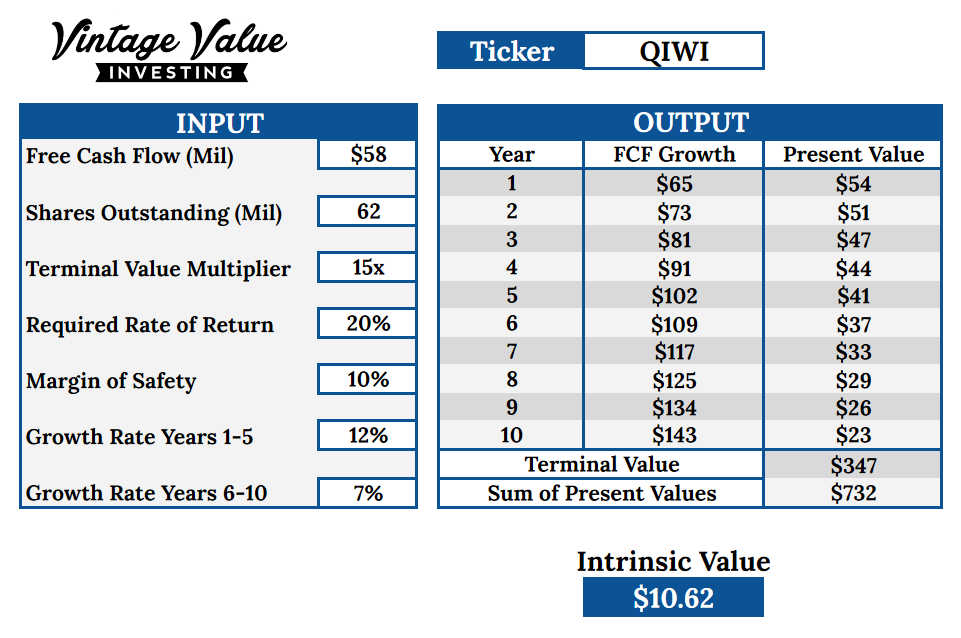

Discounted Cash Flow

Considering the rather irregular free cash flow of Qiwi, this method might not be the most reliable. But I will use it to assess different possible futures for the company.

In one scenario, I assume that the sanction on international transactions stay forever, and durably break the company growth. Hence, no growth in the current cash flows and rather pessimistic multipliers.

In the other scenario, I assume a few difficult years, with a return to growth after some time once the situation improved. Russia’s economy is going to get more digital over time (e-commerce is still just 8% of the market there), and Qiwi’s dominance on the local market is still intact.

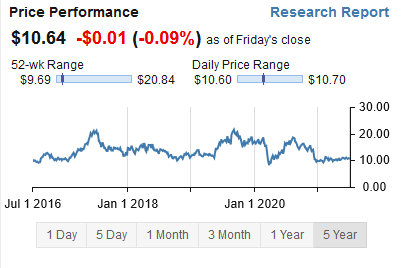

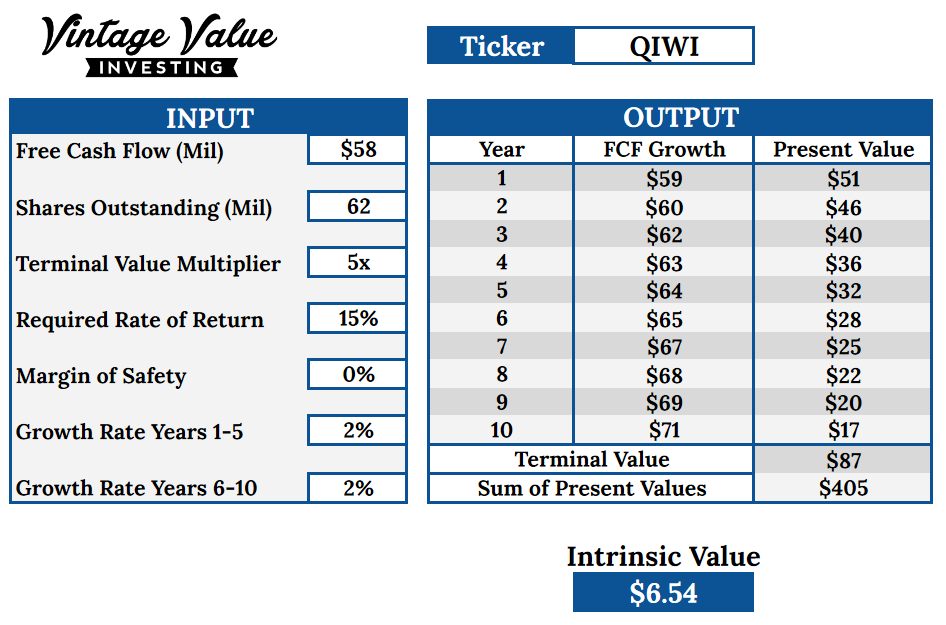

The pessimistic scenario, with permanent low multipliers, gives an intrinsic value of $6.54. This would imply that in the worst case, there is still some way down from the $10.64 current stock price, but maybe not that much.

In the more optimistic scenario, sanctions are lifted in the next 2-3 years, restarting the international transaction e-commerce activities. This allows for quick growth in cash flow at first, from the very depressed level of this year, followed by still strong growth in the future. In that scenario, Qiwi stock would be currently undervalued.

The current valuation in the optimistic scenario would offer a 20% rate of return.

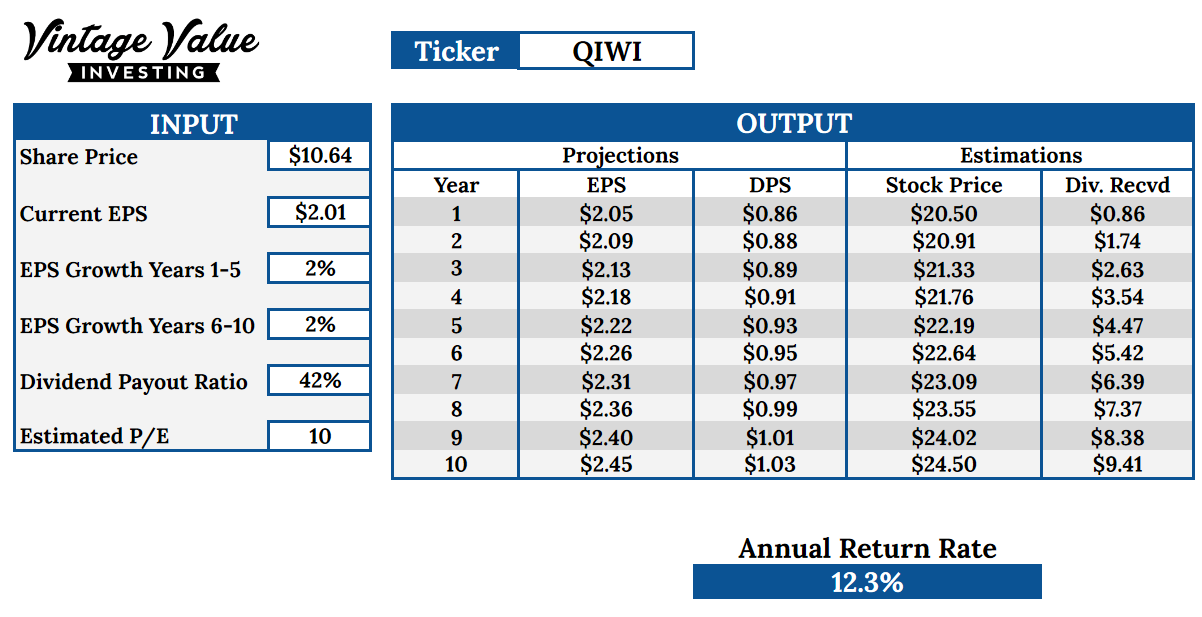

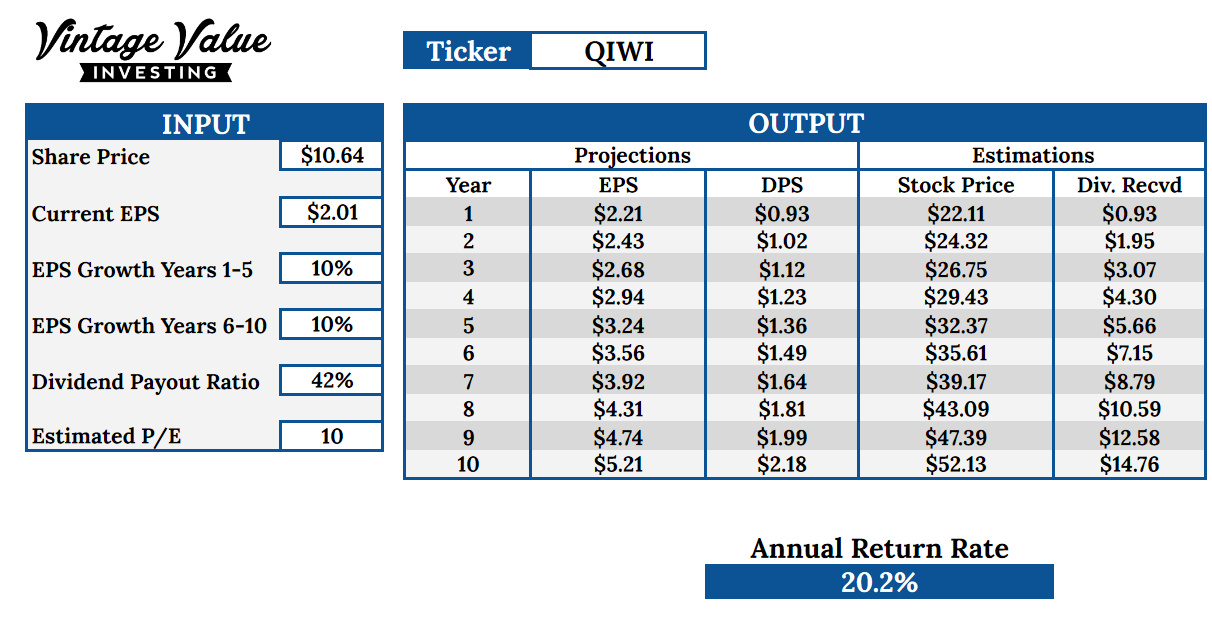

Earnings Growth

Earnings Growth is a method that considers QIWI stock essentially from its ability to grow its earnings over time. Here too I will use a pessimistic and an optimistic scenario.

As the company has managed to keep strong earnings, despite the recent issues, the pessimistic scenario is surprisingly good. Almost no future growth would still give an annual return rate of 12.3%.

The historical earnings growth for Qiwi has been at 22%. Even using a much lower and conservative 10% future growth for the optimistic scenario, this would give a strong 20% return.

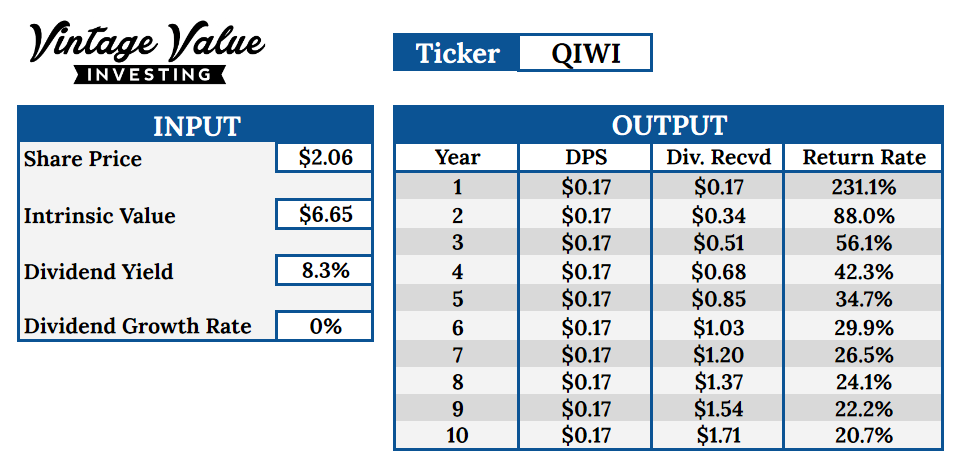

Deep Value

None of the methods above include the cash on the balance sheet, despite it being one of the best things about Qiwi. I think that currently, the CBR sanctions have spooked investors and they are discounting the balance sheet entirely.

But let’s assume that the sanction stays in place forever and that Qiwi fails to grow from now on. Considering its grip in the Russian local market and its B2B venture, a very pessimistic scenario, even with sanctions forever.

So, I will use the $6.50/share from the pessimistic discounted cash flow valuation.

But current $10.65/share does not consider the cash sitting idle. If I consider the current -$539M net debt, this means the “real” current share price that is actually a lot lower. Most of it is cash sitting on the balance sheet, not a valuation of the ongoing business.

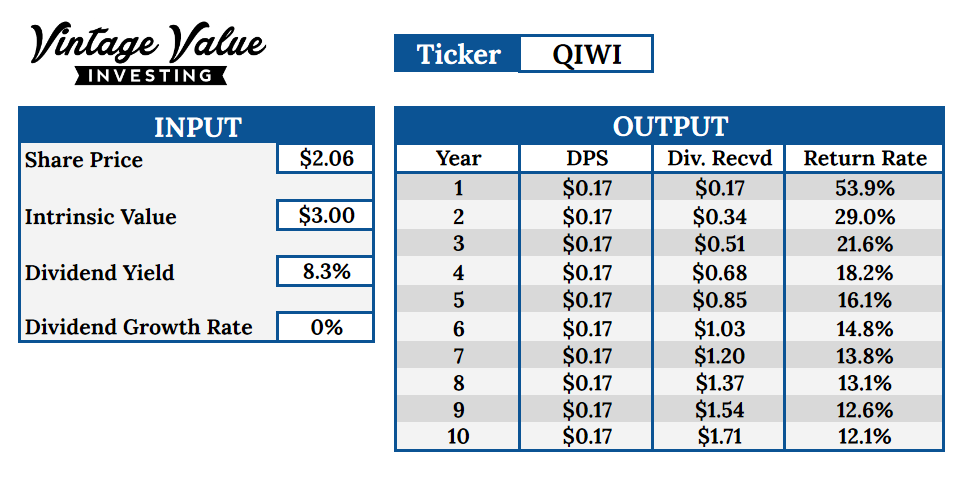

At a $128M “real” market cap net of cash and debt, this would mean a “real” share price of $2.06 ($128M in market cap / 62 million shares).

Once we have considered the cash on the balance sheet, even a low intrinsic value, way below the current share price, would still be enough to qualify Qiwi in the deep value category. Even it took a decade for the market to acknowledge it, returns would still be in 20+%.

Even if the intrinsic value was way below that, at a third of the current price, the quality of the balance sheet might still offer decent returns.

Other Calculation Methods

Considering the incertitude around dividend growth, I decided that the Yield on Cost method would not be useful for QIWI.

Final Assessment

Company Synthesis

Qiwi is a company where I had trouble making up my mind. Some aspects of it, like ongoing sanctions from the central bank, should make a big no-no in terms of risk. The geopolitical and currency risk of it being in Russia does not help.

But at the same time, the very rich balance sheet, the steady net income, and the “only” 18% revenue decline might mean that market strongly overreacted by considering Qiwi a dying business. So, which one angle to believe?

Right now, Qiwi is priced for stagnation with a good chance of total failure. It could turn into a complete net-net, with an 8% dividend yield on top of it, and good earnings, and the stock price would probably not even react.

Still, markets might be right on that. When regulatory troubles come for financial companies, the saying is “there is never just one cockroach”. Who knows what other malpractices have been hidden away and might lead to more fines and sanctions?

Or does the partial lifting of the sanction, a new CEO indicate the trouble are already behind, and things are going to improve from now on?

Valuation

Valuation methods gave very different results, indicating how difficult it is to value Qiwi. If the company returns to normal, returns should be in a 15-30% range. So, the question is really to assess how likely it is for things to go bad.

I consider the recent management changes, the divestment of unprofitable projects like Solvest, and the exit of the founder responsible for the previous bad decision as a good sign. The board has finally reacted and manage to wrestle back control, something that should have been done when the first CFO arrived and left in 6 months in 2019. The whole mess could have been avoided then.

The real unknown is the possibility of more malpractices and sanctions incoming. The relatively moderate fine and partial lifting of sanctions could indicate that the CBR has not found anything else and is satisfied with the corrections being implemented.

Possible Strategies

Qiwi has 3 possible futures. A low chance of more hidden flaws, more sanctions, and total failure of the company. Another low chance of permanent ban from international transactions, reducing greatly the company growth potential. And the possibility that Qiwi manages to get back in compliance with the regulatory authorities.

Considering the high risks involved, Qiwi should in any case be a small part of a portfolio, from 1-5% at most. I would however argue that the encouraging signs on the regulatory front and the massive cash amount provide a margin of safety in itself. So is the very depressed share price.

So even if things take 5-6 years to get back to normal, Qiwi could still be a 20-30% return investment.

This investment would definitely increase the volatility of your portfolio, so in my view, should be made in conjunction with more stable and safer compounders, like for example GD I covered a few months ago.

If Qiwi does not crash and burn, the daring investors that took the risks will have to choose in a few years. Either exit their position with the gains from the company turnaround, with the company stock catching up with the fact that the net income has tripled since 2017.

Or hold it for the long term, counting those growing revenues, high dividends, and domination of a market with hundreds of millions of people (with accelerating switch to digital, 70% of retail transactions are still in cash) will allow Qiwi to become a steady compounder in the future. One that also delivers strong dividends along the way.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in QIWI and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.