Any investment portfolio is exposed to various risks as investors are generally required to take on risk to generate returns. Risk cannot be eliminated, but it can be managed and reduced in various ways. Portfolio hedging strategies can be used to reduce the market risk that stock portfolios are exposed to.

In this article, we describe several ways to reduce market risk, either temporarily or permanently.

⚠️ Important note: This article provides an introduction to various hedging strategies, hedging instruments and how they can be implemented. However, this is a complex topic, and this article should not be regarded as investment advice. Before implementing any of these strategies and particularly short selling or option strategies, you should seek professional advice or research the topic thoroughly.

What Are You Actually Hedging?

The objective of hedging stocks, or other investments, is to manage risk. But exactly what risk is being managed? In a portfolio of stocks, each stock carries unique risks associated with the company and the market it operates in. There are various ways to hedge the risk of an individual equity position. However, we generally accept these risks and rely on diversification to reduce the impact they pose to a portfolio.

Market risk is more of a problem because it can affect an entire portfolio. This is the risk that a large correction or bear market can pose to almost every stock in the market. If you want to reduce a portfolio’s exposure to market risk, you will need to look beyond diversification.

Portfolio hedging strategies are implemented to reduce a stock portfolio’s exposure to market risk – in the form of volatility or risk of loss of capital. The strategies described here concern this type of risk. Investors also face inflation risk. This can be hedged, though a typical stock portfolio aims to generate returns that beat inflation – so in a sense a stock portfolio is a hedge against inflation.

Different Approaches to Portfolio Hedging

Broadly speaking, there are two approaches to hedging stocks. The first is to implement a hedge consisting of options or short positions to reduce downside risk. This type of hedge can be added or removed according to market conditions. The second approach is to include assets that tend to perform well during bear markets and corrections to a portfolio of stocks. This approach is a little less effective but can be combined with a long-term investing strategy. This means you will not have to try to “time the market”.

Short Selling

Short selling is a very direct method of hedging stocks which can be useful in certain situations. If you anticipate general market weakness, you can short sell stocks, ETFs (exchange traded funds), futures or CFDs (contracts for difference) to temporarily reduce exposure to the stock market.

There wouldn’t be much point in having a permanent hedge consisting of a short position like this – so it’s an active approach to portfolio hedging. In most cases, you would short sell an instrument that represents a market index, like an index future or an ETF.

Example: Portfolio hedging by short selling S&P500 ETFs

Let’s say you have a portfolio of stocks worth $100,000 and you are worried that a stock market crash is about to occur. You can short sell 167 SPY S&P500 ETFs, which at a price of $600 would be worth $100,200.

If the market does fall, your gains on this short position would help to offset losses in your portfolio. However, if the index rises, your short position will generate losses that will offset gains in your portfolio. The effectiveness of the hedge will depend on how similar your portfolio is to the instrument you sell. To improve the hedge, you can consider using other ETFs that are a closer match to your portfolio.

Hedging stocks in this way has two distinct advantages. Firstly, a hedge like this can be implemented quickly and relatively cheaply. And, secondly, you can avoid the taxes that may have been incurred by selling stocks in your portfolio and realizing a capital gain. The disadvantage to this approach is that you are limiting gains as well as losses. Your timing will also have a significant impact on how well the hedge performs.

Market timing is not easy, and you will need to decide when to open and close the hedge – so that are two decisions you will need to get right. Nevertheless, there are times when you may want to reduce exposure, and this is a very simple way to do so. Remember, you do not have to hedge the entire portfolio. You can also add to the short position as volatility increases, and remove the hedge when volatility falls.

Inverse ETFs

An alternative to short selling index ETFs or futures is to buy inverse ETFs and leveraged, inverse ETFs. These funds are designed to rise when the underlying index falls and vice versa. It’s important to note that because of the way these products are structured, their performance can diverge from the performance of a direct short position.

They can still be effective over short periods of time but may not perform as expected over longer periods. The other notable difference between inverse ETFs and direct short positions is that they require capital to purchase, whereas short positions result in a credit in your trading account.

Portfolio Hedging With Options

Options offer a more sophisticated alternative for portfolio hedging. A call option is a contract that gives you the right to buy an asset at a specific price (the strike price) in the future before or on a specific future date. A put option gives you the right to sell the asset at the strike price. The price you pay for an option is the premium. In the context of hedging stocks, the premium can be thought of as insurance against loss.

The simplest way to use options to hedge a portfolio is to buy a put option. However, investors often use a combination of long and short option positions to reduce the total cost. We will first describe a simple example using a put option, and then look at some more complex option structures.

Example: Portfolio hedging by buying a put option

You have a stock portfolio worth $100,000 and want to hedge it using SPY put options. The S&P 500 index is currently at $6,000, and the SPY ETF is trading at $600. You decide to hedge by purchasing put options on SPY with a strike price of $600 and an expiration date 90 days away.

Each SPY option contract covers 100 shares, so one contract controls $60,000 worth of SPY ($600 x 100). To closely match your $100,000 portfolio, you decide to buy 2 put option contracts, which gives you exposure to $120,000 worth of SPY. That over-hedges slightly, but it’s the closest match available.

The premium for each option is $18, so:

- Premium per contract = $18 x 100 = $1,800

- For 2 contracts: $1,800 x 2 = $3,600

To fund this hedge, you sell $3,600 worth of shares, reducing your portfolio’s equity exposure to $96,400. You are now hedged on $120,000 worth of SPY, which is more than your portfolio’s value, but since portfolios rarely track the index perfectly, this may help offset larger drawdowns.

In summary:

- You’ll benefit from the hedge if SPY drops by more than 3.6%.

- You’re protecting roughly 94–100% of your portfolio for 3 months.

- The hedge costs $3,600, or 3.6% of the notional value covered.

From this example we can make a few observations:

- There will be a cost for a hedge like this regardless of whether the expected correction occurs or not. Using options is a trade off between the cost and the potential loss.

- There may be a mismatch between the performance of the index and the performance of your portfolio. This will depend on the index you choose, and the type of stocks you hold in your portfolio.

- An option has an expiry date – the further out the expiry date the more expensive the options will be.

- Apart from the premium you paid, there is no opportunity cost, and your upside is not limited as it was with the short sale.

Alternative Option Structures

An at-the-money put option, where the strike price is equal to the current price is the simplest way to hedge with options – but it’s also the most expensive alternative. The following are a few cheaper alternatives:

- Out-of-the-money put option – Instead of buying an at-the-money put option, you can buy a put with a lower strike price. This means your portfolio will only be protected after the index falls a certain amount, but the premium will be lower. So, you will be partially protected from a large correction, but will still be affected by a small decline.

- Put spread – You can also buy one put option and sell another with a lower strike price. The premium you earn by selling the second put option will offset part of the premium you pay for the first. A put spread means your downside protection is limited to the difference between the two strike prices. If the index falls below the second-strike price, gains on the first option will cancel out losses on the second option.

- Collar – A collar consists of a long put and a short call option. You would buy a put option with a strike price at or just below the current market price and sell a call option with a strike price above the current market price. By selling a call option you earn a premium to offset the premium you pay for the put option. The disadvantage of a collar is that the short call position will cap your portfolio gains if the market rises. This structure does make sense if you are convinced the market won’t rise.

- Short fence – A short fence combines a put spread and a collar so that you buy one put option and sell a put and a call option. We can illustrate the logic behind this structure by building on the previous example.

Example: Portfolio hedging with a short fence

In this scenario, you want to hedge a $100,000 stock portfolio using a short fence (or collar spread) strategy.

You start by buying a 3-month at-the-money put option on SPY with a strike price of $600, which is the current SPY ETF price. The premium for this put is $18, which means the option costs you $1,800 per contract, or $3,600 total for 2 contracts (covering $120,000 of notional value). That’s 3.6% of the amount you’re protecting.

To reduce this cost, you:

- Sell a call option with a $640 strike price for $4, and

- Sell a put option with a $510 strike price for $6

This generates $10 in premium income per share:

- $10 x 100 x 2 contracts = $2,000 received

Now your net cost is $1,600 ($3,600 – $2,000), or 1.6% of the notional value covered by the hedge.

What this hedge means:

- The $600 long put protects your portfolio from losses if SPY drops below $600

- The $510 short put offsets gains from the long put below $510 (a 15% decline from $600)

- The $640 short call caps your upside if SPY rises above $640 (a 6.7% gain from $600)

Summary:

- You paid 1.6% of portfolio value to protect the first 15% of downside

- If SPY drops between $600 and $510, your long put provides full protection

- If SPY falls below $510, gains from the long put are offset by losses on the short put

- If SPY rises above $640, your portfolio upside is capped

This “short fence” strategy gives you defined downside protection up to a limit, and helps reduce the cost of the hedge — but at the expense of limiting potential gains.

Option strategies like a short fence provide partial protection but will not protect a portfolio from a catastrophic market crash. These structures are favoured by portfolio managers who aim for relative outperformance.

Options on ETFs vs. Options on Futures

In the examples on short selling and portfolio hedging with options we have used the SPY ETF and options on it. You can also use futures contracts and options on these futures contracts. There are pros and cons to using both. ETFs and options on ETFs can easily be traded using a normal stock trading account.

There are also more ETFs than futures contracts, though some are more liquid than others. Futures and options on futures require a separate futures trading account. However, they can be traded with margin, which means you do not have to fund the full value of a long option position. Futures also have lower trading costs and tighter spreads.

Portfolio Hedging With Asset Allocation and Diversification

Hedging stocks with options and futures can be very effective, but it also can be expensive – both in terms of option premiums and opportunity cost. Alternatively, there are several ways to hedge a portfolio through diversification and asset allocation. Assets that are viewed as safe havens can retain value during periods of market volatility. Therefore, hedging stocks with safe haven assets is a common strategy to protect portfolios against drawdowns.

This often results in capital flowing into these safe haven assets as volatility increases, which means their prices rise as equity prices fall. The prices of these “risk-off” assets may appreciate over time, though they tend to underperform the equity market. Including them in a portfolio results in slightly lower returns, but at the same time reduces portfolio volatility significantly. The following assets can be used as hedging instruments:

Bonds

Bonds, and AAA-rated government bonds, in particular, are regarded as being risk free. Bonds have proven to be a reliable way of hedging stocks during almost every period of stock market volatility over the last few decades. US treasuries have also appreciated over most periods for the last four decades.

You can hold bonds in your stock account via an ETF like the iShares 20+ Year Treasury Bond ETF (TLT).

Gold

Gold is probably the oldest safe haven around and has been used as a store of value and a medium of exchange for centuries. The price of gold has also shown itself to be negatively correlated with stock prices during market corrections. Whether or not gold makes a good standalone investment is the subject of a separate discussion – but it has proven to be a very effective hedge over the years. Gold has the added benefit of being an inflation hedge.

There are lots of different ways to invest in gold, and we will cover them in a different post. However, for stock investors, the SPDR Gold Shares ETF (GLD) is an efficient and cost-effective vehicle.

Defensive Stocks

Stocks in certain sectors and industries are regarded as being defensive if their fundamentals are not closely tied to the health of the general economy. Defensive sectors and industries include consumer staples (like household products), healthcare, utilities and defence. While defensive sectors theoretically outperform during bear markets, in practice this isn’t always the case. Certain sectors have outperformed during each correction, but on the whole, defensive sectors haven’t always been a reliable means of hedging stocks.

If you do want to invest in defensive stocks you can consider ETFs that hold stocks in relevant sectors and industries, or consider a specialist fund like the Invesco Bloomberg Pricing Power ETF (POWA).

Cash

Holding cash is another method of hedging stocks. In today’s low interest environment, the return you earn from cash will be close to zero. However, hedging stocks with cash is very flexible and cash can be rotated into stocks at lower prices as a correction unfolds.

Holding cash directly provides peace of mind and means you won’t have liquidity issues if trading on exchanges is restricted. Alternatively, you can invest in an ETF that holds bonds with maturities shorter than 3 months. A popular choice is the State Street 1-3 Month T-Bill ETF (BIL).

Volatility ETFs

A newer hedging instrument that has emerged in the last decade is the volatility futures contract and ETFs that hold these contracts. These are not safe haven funds but they do perform well in “risk off” environments. Implied volatility is the variable component of an option’s price and increases when demand for options rises. This typically occurs as market volatility increases. The VIX index tracks an index of the implied volatility of various S&P 500 option contracts. This index is tradable via futures contracts with weekly expiry dates.

Several ETFs that hold volatility futures are available to investors. These funds will give your portfolio positive exposure to implied volatility, so they offer another alternative for hedging stocks. However, it’s important to note that over time these ETFs lose value. This occurs because each futures contract is rolled into a more expensive contract as expiry approaches.

The ProShares VIX Mid-Term Futures ETF (VIXM) is one volatility fund to consider.

Portfolio Hedging Examples With Safe Haven Assets

We have mentioned several ETFs that can be used to reduce downside risk in an equity portfolio. In the following examples, we will combine these ETFs with the S&P500 SPY ETF to see how they performed during the corrections in 2008 and 2020. In each case, we are tracking the performance of a portfolio with 70% invested in the SPY ETF and 30% in the other ETF.

- SPY: S&P500 only

- SPY + TLT: 70% S&P500 and 30% bonds

- SPY + BIL: 70% S&P500 and 30% cash

- SPY + GLD: 70% S&P500 and 30% gold

- SPY + DEF: 70% S&P500 and 30% defensive stocks

- SPY + VIXM: 70% S&P500 and 30% volatility ETFs

First, the major bear market of 2008 and 2009:

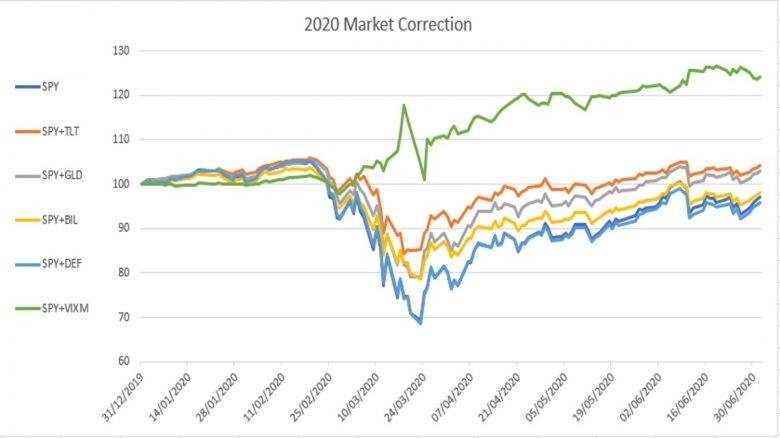

And secondly, the sudden correction that occurred in March 2020:

Using these examples we can make a few observations:

- Firstly, apart from the volatility ETF, allocating 30% of a portfolio to a safe haven asset reduced downside risk by up to 50%.

- The volatility ETF didn’t exist in 2008, but was very effective in 2020.

- Gold was a very good hedge in 2008 and performed slightly worse than bonds in 2020.

- On balance, gold and bonds are both effective hedging instruments.

- Cash is inferior to bonds as a hedge – though it does provide liquidity.

- The defensive ETF we included here provided very little protection during both corrections.

For a more complete picture of the effectiveness of these assets for portfolio hedging, we need to consider the opportunity cost. We can do this by repeating the exercise over a five year period. You will notice that the portfolio with VIX ETFs underperforms by a very wide margin. The portfolios with gold and bonds provide adequate long term performance.

Portfolio Hedging With Alternative Assets

Alternative asset classes can also be used for hedging stocks. Alternative assets that can be used for hedging include hedge funds, commodities, real estate, private equity funds, venture capital and even art. These assets can all generate positive returns over time – but returns will depend on the choice of asset or fund, and the timing of the investment.

When it comes to hedging stocks, the biggest advantage of the alternative assets mentioned above is probably the fact that they are illiquid. If an asset is illiquid, it can’t be traded and priced each day. The risk of loss still exists, but you don’t have the volatility of liquid instruments that are valued using mark to market pricing.

Cryptocurrencies and commodities can also provide some diversification, and commodities, in particular, can be effective inflation hedges. However, both commodities and cryptocurrencies can become volatile during equity market corrections.

When to Hedge a Portfolio

If you are hedging stocks using short selling or options, you will need to decide when to implement a hedge. There is often a temptation to implement a hedge when you believe a market crash is coming. Before you do this, you should consider how likely you are to be correct. Plenty of crashes are predicted that never actually occur. If you hedge your portfolio every time a crash is predicted, you might lose a lot of potential upside or spend a fortune on option premium. Nevertheless, there may be certain periods when you would like to reduce exposure.

In general, it’s worth adopting a more systematic approach. A contrarian tactic is to buy options when the market goes through a euphoric period and momentum hits historically high levels. This may not seem like the time to buy options, but there are two advantages. Firstly, you get to lock in gains by setting your strike at a higher-than-normal level. And secondly, this is when demand is low and implied volatility is at its lowest – so options are at their cheapest.

With short selling, you can take the opposite approach, and build up a short position as the index falls through key moving averages – the 50-day, 100-day and 200-day for example. This will give you more protection as the index falls, and you won’t have to make predictions. You would then buy back the short positions as the index rises again. Ultimately there will be a cost to this strategy, but the cost will increase as the severity of the correction increases. You won’t be over-hedged if the correction is shallow, and you won’t be underhedged if it turns into a full-blown crash.

The alternative approach – including safe haven assets and alternative investments in your portfolio – means you don’t have to try to time the market. It also means you will have some protection if a black swan event comes along.

Hedging Costs

Hedging stocks is all about weighing up various risks and costs. Besides the obvious risk of loss, you will need to consider the potential psychological cost of a loss, and how that may affect your decision making. Investors often make their worst decisions when their portfolio takes a big knock. This is when the full value of hedging can become apparent. When it comes to costs, you will need to consider the actual hedging cost (option premiums and trading costs) as well as the opportunity cost of limiting upside, and slippage (which increases during periods of volatility).

Conclusion on Portfolio Hedging

You can’t eliminate portfolio risk entirely, and you should probably avoid the temptation of trying too. If you take away all the risk, you’ll probably limit your returns severely. At the same time, it’s important to reduce unnecessary risk – and portfolio hedging is one way to do this.

Ultimately, there is no such thing as a perfect hedge, perfectly executed. To avoid placing too much importance on any one decision, it’s often worth combing several different approaches to hedging. What is your view on hedging a portfolio and what are your favorite hedging strategies? Share your thoughts in the comments below.

I am also looking for a very profitable hedging strategy. I need a good scalping EA or manual strategy. Have you had any luck in finding?

Can you please share your hedging strategies, hedging experiences with bots EA etc.? Is it possible to make consistent profits with hedging?

I mainly hedge through diversification to reduce exposure more so than offsetting within the same asset class. I’d be interested to hear some more thoughts on this. I’m aware of the use of options for hedging purposes but I’m yet to exercise this.

Thank you for your reply Andy. I’m now testing a hedging system based on mathematical formulas (currency correlations) and working on the millipede system which I studied for a long time.

I don’t like hedging because at the end you will always lose your money via SWAP and commissions. So why hedge?

In my opinion, hedging a portfolio should not be seen as a way of making money, but rather as insurance. It may well make sense to temporarily hedge a portfolio against risk in case of market turbulence or important events that can cause volatility.

However, this is subjective and depends on the investor’s risk tolerance. While some investors focus on capital preservation and hedge their portfolios, others simply sit tight during corrections and bear markets. In either case, hedging should be something temporary. If you are constantly hedging your portfolio, you are likely to lose money or miss out on a lot of upside potential.