October 15th, 2021

Quick Stock Overview

Ticker: PAYS

Source: www.tikr.com

Key Data

- Sector: Industrials

- Sales ($M): 20

- Industry: Specialty business services

- Net Cash per share: $0.05

- Market Capitalization ($M): 129

- Equity per share: $0.23

- Price to sales: 6.4

- P/E: -0.2

Investment Thesis

Back To Capital-Efficient Companies

Having covered a string of large and complex companies, I wanted to focus on smaller, easier-to-understand companies. The recent turmoil in the energy sector has given us a great opportunity, which I have explored quite extensively for a few reports, including gas midstream, renewables, and two utilities.

But ultimately, I intend for my portfolio to include some longer-term compounders that can generate more profits by reinvesting their profits.

A business with low capital requirements is even better. Investors can protect themselves from inflation so long as the business benefits from it. The alternative is to follow Buffett’s example of buying businesses with a very low capital requirement

“The best businesses during inflation are the businesses that you buy once and then you don’t have to keep making capital investments subsequently,”

Following a lengthy screening process, I think I have found a financial service provider I am interested in. It’s Paysign, a company that sells prepaid cards primarily to the healthcare industry. Despite the fact that the company has a small headcount (70 employees), it has experienced rapid growth in recent years.

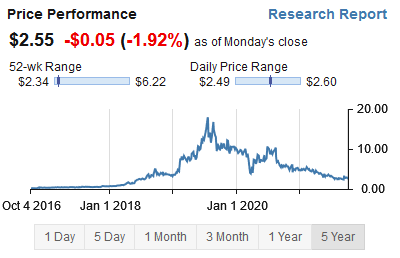

Hard Hit by Covid

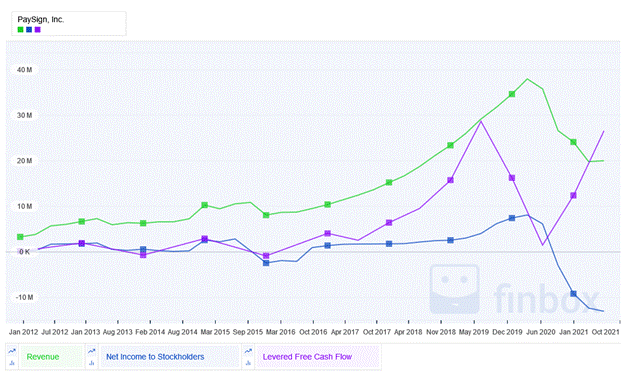

It appeared as if 2019 would be a record year for Paysign, with the company’s revenues soaring, free cash flow expanding rapidly, and profitability increasing significantly. Exactly when every startup dreams of reaching the exponential phase, the entire system crashed down in 2020 due to…well you know what.

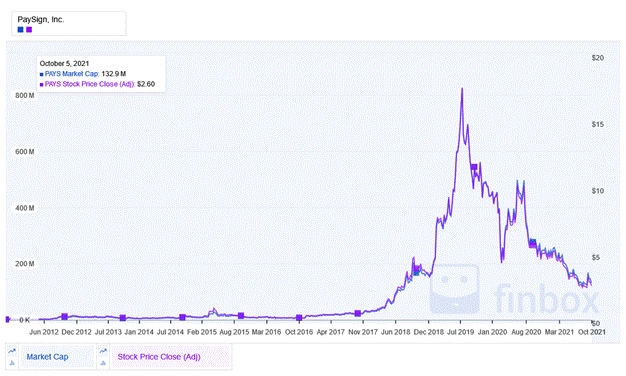

From the company’s market cap and share price, you can see that it enjoyed a beautiful upward trend. A few months later, Covid disrupted the growth pattern of the company, shattering its valuation in the process.

But not so fast. I was initially attracted to Paysign due to its good free cash flow (and price to free cash flow) even though it had negative earnings. Only one of two scenarios was likely to be true, so I dug deeper:

- The free cash flow was temporary or an accounting fluke, and the company was deeply in trouble, or…

- There were likely temporary negative earnings, and the market price had yet to realize it, so we are able to buy it at a discount

As a result, I went on to learn more about Paysign’s business in an attempt to improve my understanding of it.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A Lifesaving Niche

Focus On Healthcare

On the surface, Paysign is a provider of prepaid debit and credit cards. While not particularly bad business, it is a rather competitive sector like most Fintechs.

So, what are Paysign’s competitive advantages?

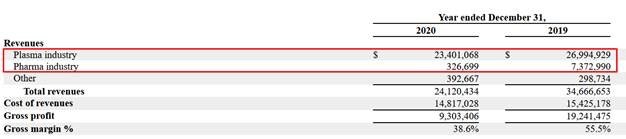

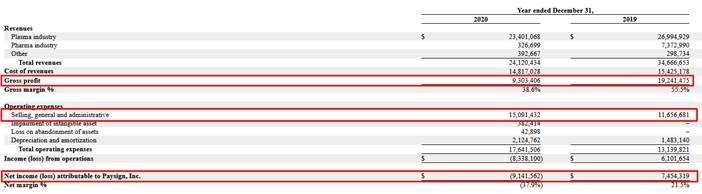

Paysign generates most of its revenue from the healthcare industry, especially from plasma. As for the pharmaceutical industry, it had good results, too, but with Covid, this revenue stream has virtually disappeared.

The main product of Paysign is its prepaid cards that can be used at various retail outlets. Its technology allows it to tailor to any client’s specifications, from buying only from a specific location, or from a limited list of sellers.

The Plasma Business

A US plasma donation center compensates its donors with money, historically in the form of cash or checks. Many plasma donation centers looked for other solutions due to the logistical difficulty of managing the check and keeping the cash safe.

Paysign identified this unique market need in 2011, and it is still its primary source of revenue.

Currently, the company is used by 356 plasma donation centers in the USA or 36% of the industry. Management expects this number to jump to 400 by the end of the year (as opposed to 290 a year ago), or approximately 15% yearly growth.

By being the predominant solution in the sector, and customizing its solution to the specific needs of plasma centers, Paysign is likely to be able to keep growing for some time, at least until it reaches 60-80% of the market.

It is estimated that plasma centers generate $5,500 to $6,500 per month on average. Although more plasma centers are using the Paysign solutions, this number has been slightly reduced by Covid (-$3M of revenues in total). This can be partly attributed to the U.S. southern border closing.

However, considering how vital plasma donations are for a large number of lifesaving treatments, this is an impressive revenue line.

The Pharmaceutical / Co-Pay Business

Let’s talk about co-pays.

For those who are unfamiliar with the concept of co-pay, I recommend reading this article. Usually, this refers to the amount a patient has to pay on top of his health insurance coverage. Premiums can quickly reach levels that seriously affect patients’ finances or even prevent them from buying life-saving medicine.

Pharma companies are aware of the problem and have set up co-pay assistance programs to help patients. The patient signs up with the manufacturer and receives a co-pay card.

Essentially, pharmaceutical companies provide payment assistance to make expensive medications more affordable for people who need them. The method is somewhat controversial, as copay is used by insurance companies to encourage patients to use cheaper medicines instead of expensive ones.

In short, pharmaceutical companies are attempting to reduce the use of specific drugs by expressing their concerns to insurance companies.

I am not willing to debate whether this is or is not a proper response to the medical affordability issues in the American healthcare system, since that would take us far away from the purpose of this report. I have no ethical problems with companies helping patients access these vital drugs, but at the same time, the solution seems rather complicated at first glance.

Pharmaceutical companies prefer to find a service provider that can send and manage co-pay cards for them instead of doing it themselves. This is what Paysign does in its “pharma” segment.

Many insurers waived co-pays during the pandemic, resulting in the quasi-disappearance of the business in 2020.

People also avoided pharmacies and medical consultations, resulting in very low turnover for co-pay card systems. During this period, Paysign revenues decreased from $7.3M to $0.3M.

Co-pays and their associated problems for patients are unlikely to disappear anytime soon, however. Insurance companies are slowly reintroducing copays.

Pharma companies seem to agree. Paysign onboarded six new copay programs just last quarter and renewed its contract with a major pharmaceutical hub.

Paysign’s losses in 2020 are largely attributed to the sudden disappearance of co-pay revenues. The market is slowly returning to normal, so the sector should become a growth engine for the company by 2022.

Other Segments

In truth, the rest of Paysign’s operations are quite small and I don’t believe they are worth much attention at the moment. While they have generated a few hundreds of thousands of dollars in revenue from the hospitality and retail sectors, these seem to mostly be an afterthought and not the priority of the management team.

Chapter 2: The Path to Recovery

The Ongoing Growth

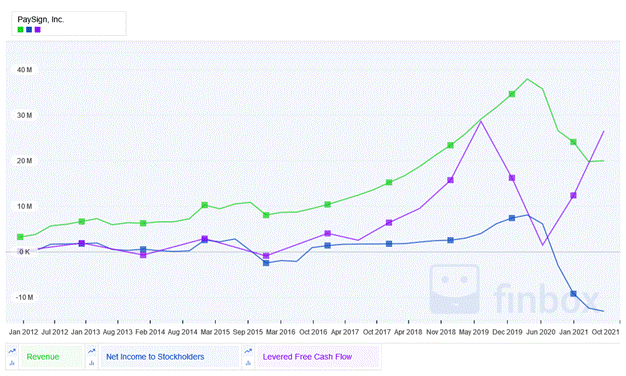

To be honest, the revenues and profits that Paysign has generated since 2020 do not reflect fully improving business, contrary to the free cash flow

But there is some good news!

Firstly, Paysign’s grip over plasma donation centers is gaining speed rapidly. The company could easily double its revenue in this sector if it had roughly a thousand centers in the USA. As a result, both a 15% market share growth rate can be maintained up until 70 – 80% market control, and profitability can be increased once Covid effects subside.

Secondly, with vaccination coverage among US citizens increasing, and insurers bringing back co-pays, the co-pay sector may return to normal. Co-pay assistance programs will therefore be available to pharmaceutical companies again.

What interests me most about this company, however, is its competitive situation regarding copay services. Management isn’t very candid about it and has failed to mention any direct competitors. I couldn’t tell what portion of the segment co-pay and what portion plasma center was before 2019, so I cannot compare the two segments historically.

It appears the copay segment entered the market in 2015, indicating that this business line grew to $7M within 4 years. Paysign’s co-pay support program is already scheduled to launch in 2021, so I expect revenue growth to continue (at least 5-10%), though I am not sure how unique or good the company’s offering is.

The Clinical Trials Opportunities

However, management at Paysign occasionally mentions one area of the company’s business that, in my opinion, could grow into the company’s third segment.

Prepaid cards are already used by the plasma donation centers as a practical and efficient way to thank the individuals participating in life-saving medicine production for their contributions.

Similarly, in clinical trials, patients are routinely compensated for their participation in trials. Cash or checks have been used historically for these payments, similar to the way plasma centers manage their reward programs.

There is already a growing network of pharmaceutical companies using Paysign’s card for co-pay support programs. Especially for new and complex medicines, these co-pay programs work great. Paysign should leverage their relationship with these innovative pharmaceutical companies to offer pre-paid cards for their clinical trials.

As I said, management mentions clinical trial opportunities, but for now they’ve bundled them with “other business.” As it stands, most of the copay contracts with pharmaceutical companies are at best 3-4 years old.

Because it takes so long for a clinical trial to be planned, launched, and executed, Paysign has only now begun offering its services for newly designed clinical trials.

The existing base of clients acquired with co-pay offers has a lot of potential to expand Paysign’s business.

The Other Markets

Another segment of growth is biological donation centers. So far, Paysign has focused on becoming the biggest plasma donation center. However, there are lots of other industries that might also need to modernize their reward system away from cash and checks and into digital systems.

Blood, platelets, eggs, sperms, breast milk, and hair can all be donated. I know it’s not everyone’s cup of tea, but it’s a massive market, providing patients with much-needed supplies.

Paysign offers a strong plasma-related product offering. This technology can quickly be transferred to other markets for biological donations.

Paysign could use this to get its foot in the door for providing prepaid cards as a reward for clinical trials not just by pharmaceutical companies, but also medical institutions.

It’s hard to say how fast Paysign could grow in each of those segments. However, each would be pretty capital-efficient since most of the technology R&D and support is already in place and the plasma and co-pay businesses are paying for it.

Any incremental growth would help to boost margins.

For reference in 2019, gross margins were at 55% and net margins were at 21%. Margins are pretty good but could be better considering the potential to leverage the technology to reach more clients.

The People Behind Paysign

I talked a lot about the company’s activities and possible new markets. Now let’s talk about management. Ultimately, they will make or break any change in the company.

Mark Newcomer, Co-Founder / CEO

Mark’s been working at Paysign since the company merged with 3PEA Technology 20 years ago. Interestingly, despite his background in payment solutions, he graduated with a degree in Bioscience (the field that deals with diagnostics and medicine techniques, like… plasma collection).

It’s great to see a technically oriented CEO running a company that will constantly deal with clients who are themselves doctors, pharmacists, and biologists. It might not seem like a big deal, but technical-minded pros will always prefer to speak to one of their own than a financial or corporate profile.

Matt Lanford, President / COO

Before joining Paysign in 2019, Mr. Lanford held numerous positions in payments processing, including at Citigroup and Mastercard. Mr. Lanford has a bachelor’s degree in computer science, which makes him a good fit to handle future expansion of the product line, given his IT background and experience in payment processing.

Matthew Turner, Vice President, Patient Affordability Services

Initially, I was confused about his role, but I discovered he was previously employed by TrialCard before 2019, a company that offers co-pays and clinical trial support, as well as being a competitor of Paysign. Clearly, this is what we want to poach from our competition to expand co-pays and enter the clinical trial market.

It’s great to see that the management team of the company is already in place.

Jeffery Barker, CFO

Mr. Barker joined the Paysign team in February 2021. Previously, he was a leader in the payment processing industry at Global Payment, worth $45 billion. The CFO position was also filled by top talent in the industry, which is great to see.

Chapter 3: Crushing Paysign Numbers

A Solid Base for Future Growth

Paysign’s robustness and profitability shone through during Covid, which was a challenging test for them. While co-pay revenues were interrupted overnight and plasma business declined, the company managed to keep its balance sheet very solid.

The company’s net assets dropped from $20M to $15M in 2019, primarily due to moving to a new headquarters and adding a $4M lease liability. Cash on hand stands at $7.8M in 2020 (and $6.6M last quarter) and there is no long-term debt.

It’s definitely enough cash to weather the pandemic storm and even take on any opportunities that come up in the next 2-3 years.

Judging Growth Potential and Risks

I think Paysign needs to be divided into three distinct parts. As each part has its own risk profile and expected growth profile, I will value each separately.

Plasma is by far the strongest segment and it’s growing 15% year over year. Profitability is already on its way back to pre-covid levels. Paysign is the biggest player in the industry, and it’s likely that they will control most of it in just a few years.

Next is the co-pay segment. Because insurers stopped offering co-pay waivers during the pandemic, we can reasonably expect this segment to come back to its 2019 levels by next year or the one after. With new co-pay programs coming in 2021 and the future renewal of existing relationships, it looks like the business will keep growing.

What size the addressable market is and how strong the competition is are still up in the air. Furthermore, co-pays by insurers are a very American thing, and any reform could change it overnight.

But government rarely works fast.

As long as healthcare reforms take a while, this isn’t a big deal. But if everyone hates the current system, Paysign may have a serious problem in 5-10 years.

Then there’s the new segments, from other donations to clinical trials to non-healthcare growth. I’d say this part of the company is just getting started. Keeping that in mind, Paysign’s net income in 2019 was $7M.

This is a lot of cash the company can use to market itself. Paysign could use its profit to quickly acquire new clients and replicate its plasma success in new markets if it would increase its headcount from 70 to 80-90 people.

Valuation

Earnings Growth- Plasma Segment

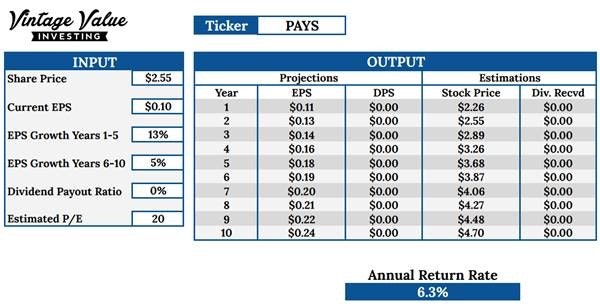

I want to start by valuing Paysign’s plasma business separately, because it has the most visibility into current revenues and potential growth. The company should keep growing fast for a while until it reaches saturation.

I’m using the earning growth method and the 2019 numbers (since they’re more representative of 2021 and 2022 activity, and if anything, understate the number of plasma centers Paysigns’ clients are).

Plasma revenue accounted for 77% of total revenue, and I’ll devote the same amount of operating expenses and cost of revenue to plasma. The stand-alone plasma business would earn $27M revenue – $11.8M cost of revenue – $10.1M operating expense = $5.1M earnings or $0.1 per share.

From just the plasma business, we can calculate a 6.3% return rate. Paysign returns can be anchored on the plasma operation, which seems like a pretty solid minimum.

Remember, I used the 2019 number, while there are quite a few more plasma centers now than there were in 2019, so I am probably underestimating the base case here.

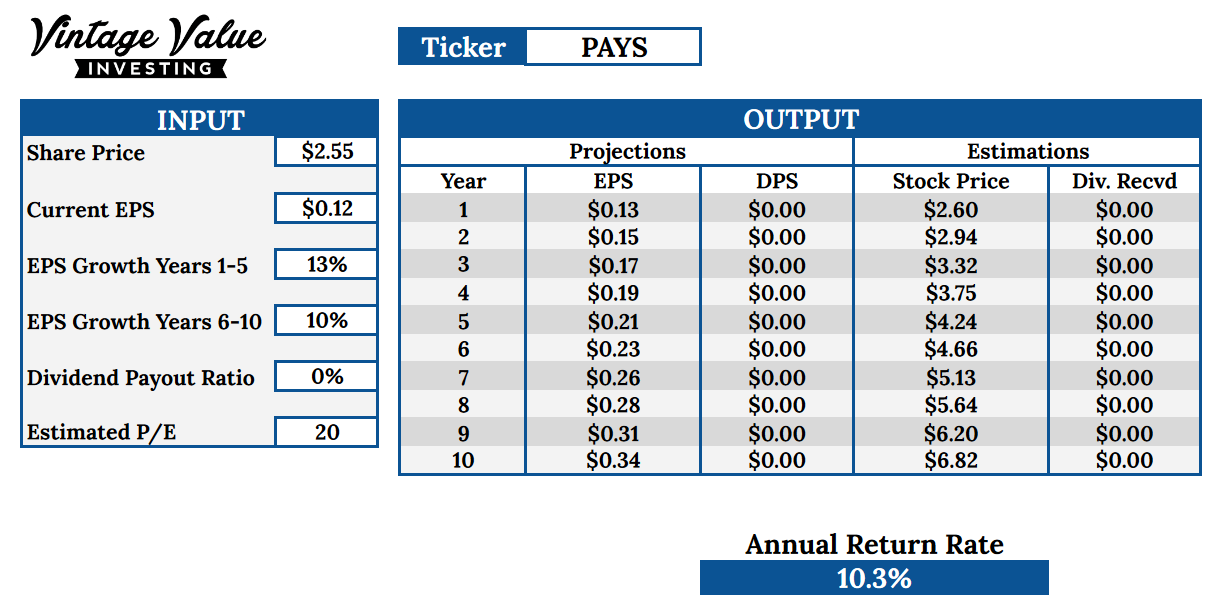

Earnings Growth – Co-Pay Segment

Despite the fact that the co-pay segment is much smaller, if we calculate the company return including it, we add:

Revenue of $7.3M – cost of revenue of $3.5M – operating expense of $3M = $0.8M. Or + $0.015 EPS.

In the long run, this increases the growth prospects, since the co-pay segment won’t reach saturation, unlike the plasma market. We’re getting better returns at 10% with those extra earnings and long-term growth.

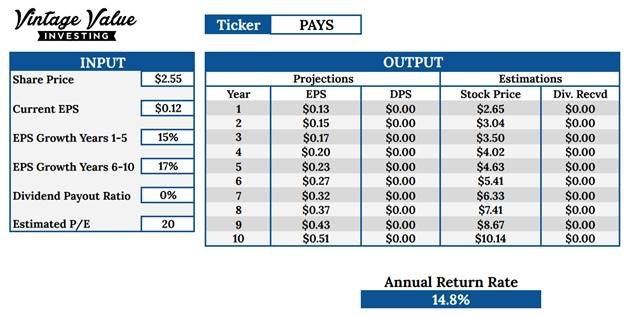

Earning Growth – Other Markets

Like I said, it’s hard to put a number on very prospective markets.

Still, I think the real value of Paysign is hidden here.

This is simply due to the fact that the biological donation market is several times larger than the plasma market alone.

Currently, clinical trials aren’t even a serious source of revenue for Paysign (a typical study costs $12M, and the industry spends $95B/year, so even a small percentage of patient remuneration can move the needle).

In addition, Paysign’s technology could be used by other venues. Paysign could control the technology directly or license it to others.

Combined, I think this should boost the company’s growth prospects, a little bit in the short-term, and a lot more in the long run. With this extra growth potential, the expected return rate goes way up.

Discounted Cash Flow

In the case of Paysign, I’d rely mostly on the earning growth method. Mostly because cash flow is a little too irregular for a precise number to be given.

Nevertheless, I was curious how the company looked using the depressed cash flow of 2020. I think a 15x value multiplier is conservative for a fintech with a ton of potential.

The intrinsic value is above the current price, so the return should be 15%. The earnings growth valuation method would confirm the valuation in this case even if it’s a tad less robust.

Conclusion

Tech and fintech companies have benefited greatly from the pandemic, boosting their valuations to sky-high levels. It also means that some of these companies, from Wise to Robinhood, might be a little overpriced right now, and carry a lot of risk.

The financial industry is going to be massively disrupted by new technologies that make payments faster and more efficient. But I don’t want to overpay for it.

Also, I prefer companies which operate in profitable niches, rather than ones that grab headlines but don’t have a solid moat and don’t make any money.

Right now, the only way a value investor can catch a good fintech company is to find one where the market doesn’t already price in the growth. Qiwi, the Russian company I covered already, was dismissed by investors because of its potential.

Paysign is a different story. As a result of Covid, the growth pattern was broken, and Paysign was priced like a “normal” company instead of an exponentially growing Fintech. I believe this is misguided.

Plasma industry dominance is increasing every day for Paysign. Co-pay business should soon return and some more. From clinical trials to biological donations, it has a large addressable market in pharmaceutical payments waiting to be explored.

Paysign’s price isn’t reflecting its growth for what I think might be a short period. It won’t take long for revenue to stabilize and free cash flow to increase. Here are the numbers again:

In the end, the value of a company is determined by how much cash it generates minus how much it needs to spend to maintain or grow its operations. Paysign is growing and it’s cheap. It will pay off at some point because its free cash flow is growing.

It is therefore different from those expensive, but growing fintech companies. It’s anyone’s guess when the market will notice Paysign’s recovery, but I think relying on strong fundamentals would be a better strategy than hoping markets get even more irrational.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in PAYS and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.