August 8th, 2021

Quick Stock Overview

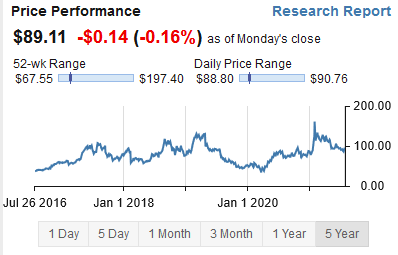

Ticker: IRBT

Source: www.stockrover.com

Key Data

- Sector: Technology

- Sales ($M): 1,541

- Industry: Consumer electronics

- Net Cash per share: 15.42

- Market Capitalization ($M): 2,503

- Equity per share: $29.33

- Employees: 1,267

- Debt / Equity: 0.1

Investment Thesis

The Rising Tide of Automation

One big investment theme of the 2020s will be automation. There is no shortage of sensational headlines about the marvels or devastation that robots and automation will bring to the world economy. Millions labor jobs have already been decimated by robots, and millions more will be replaced in the future.

Source: www.cnbc.com

Source: www.forbes.com

But really, any discussion about automation in any form could do. It can be autonomous cars taking jobs from tens of millions of trucks, taxi and Uber drivers. From people-less factory, (like this in this pretty amazing compilation of videos),automation of clerical tasks in offices, or cashier-less supermarkets, it seems not one job category is safe from the imminent army of robots coming to destroy jobs.

This topic will usually drift to the political, with discussions about capitalism, tech monopolies, Universal Basic Income (UBI), and so on. Everyone will have an opinion, debate heatedly and no one will agree at the end.

All in all, this is a topic where someone can choose to be enthusiastic or pessimistic, but it’s always controversial. And not very fun to think about.

Or is it?

There is one category of “work” that no one would be sad to see gone and done by a robot. One that virtually everybody experiences regularly, and no one enjoys.

Of course, I am talking about domestic tasks. Would it not be awesome to have a robotic butler to take care of everything while you watch a movie on the sofa.

Usually, in science-fiction story, domestic robots are vaguely humanoid and able to talk to us and understand complex tasks. Remember iRobot with Will Smith?

This design can raise some questions about the robots’ real abilities. It is something humans have been wondering about since at least Isaac Asimov robots. From benevolent helpers to merciless killers in Terminator and Matrix, robots are firmly part of our imagination about “the future”.

And maybe we are getting there with Atlas from Boston Dynamics as a notable example. You decide if you find it amazing or scary, I myself have mixed feelings about it.

Never mind the technological complexity or the cost associated with such an amazing machine. Do we truly really want a somewhat creepy human-size robot in our homes, after a lifetime of watching movies about robot uprising?

What people actually want is not so much a robotic butler, but to be freed of the most annoying and menial tasks. Things like cleaning the house, keeping the garden tidy, doing the laundry, etc. How many days of our lives are spent fighting dust and dog hairs, cutting grass, or painting the house?

Would it not be nice to press a button and enjoy our weekends?

This might resonate less with apartment dwellers in downtown rentals, but for hundreds of millions of homeowners in the suburbs, the hassle to keep the house clean and the grass short is a very real annoyance. Add a dog or cat, or a decent sized yard to take care of, and it turns into a never-ending problem.

There is a saying in marketing that “no one buys a drill; they buy the hole”. What matters is getting the job done, not having the most versatile and able robot possible.

The Domestic Tasks Automation

So, what does automation look like for domestic tasks?

Spoiler alert, it is really hard to imagine him as your new robotic overlords. It is even a little bit cute if anything.

Not that impressive right? I mean, I am sure you have heard of Roomba, maybe even considered buying one? Or one of the many clones’ other electronic firms released after, seeing the success of the original product.

I can think of three people close to me that personally own one. We even got my mom one for Christmas last year!

The first versions of the Roomba were frankly limited. Not that smart, not that efficient, not enough battery duration, you name it. But the thing is … it did not matter. Why?

Because the product became a sensation and captured the imagination of overworked and tired homemakers.

If you do not see the point of these devices, just look back at the pictures above. Notice anything? In half of the pictures, there are pets, kids, or both. The first ones will drop hairs … everywhere … every day… The second ones will simply make your schedule busy enough to make vacuuming a hassle. Combine the two, and you have a good description of a very large base of potential customers eager to save precious time and energy. House owner with kids and/or pets.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A Solid Core

A Very Solid Brand Name

In technology, there is a strong advantage a being the first at something. and/or dominate the market. This is how a brand became synonymous with an entire concept.

For instance: We “Google” something. Every plastic box is a “Tupperware” container. Robot vacuum cleaners are simply “Roomba”. A friend of mine has a “Roomba from Samsung” to handle the cleaning of hairs from his two dogs.

The best advantage (or in value investing term, moat) such position will give a company is better pricing power. If an entire class of devices is defined by a brand name, you automatically assume that said brand is the best option.

Others might have special features, or be cheaper, but the “real” one is the most recognized brand. This also gives some free marketing, as each time someone mentions some of these devices, they will mention the brand.

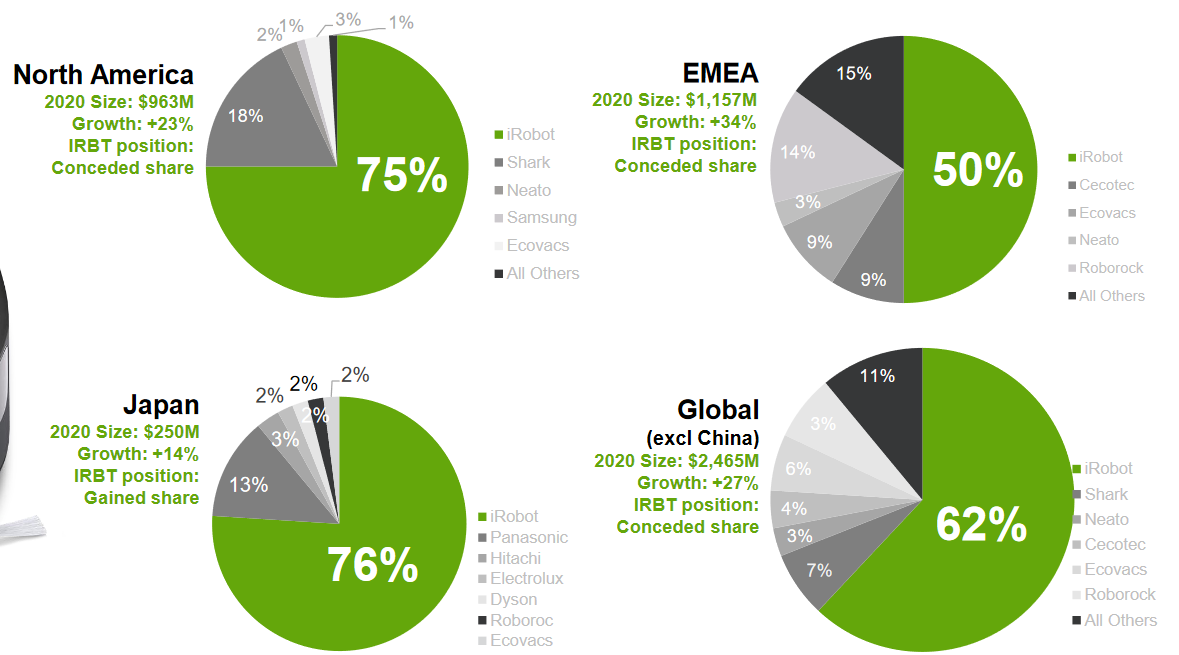

Roomba is a typical example of an early developer of new technology, becoming a namesake for the entire category. The company has been losing a bit of market share lately, but still controls 3-5x more of the market than its next best competitor.

In this industry, there is iRobot, and then everybody else. The only market where iRobot does not have more than 50% of the market seems to be China, which prefers cheaper, locally made models.

Source: www.investor.irobot.com

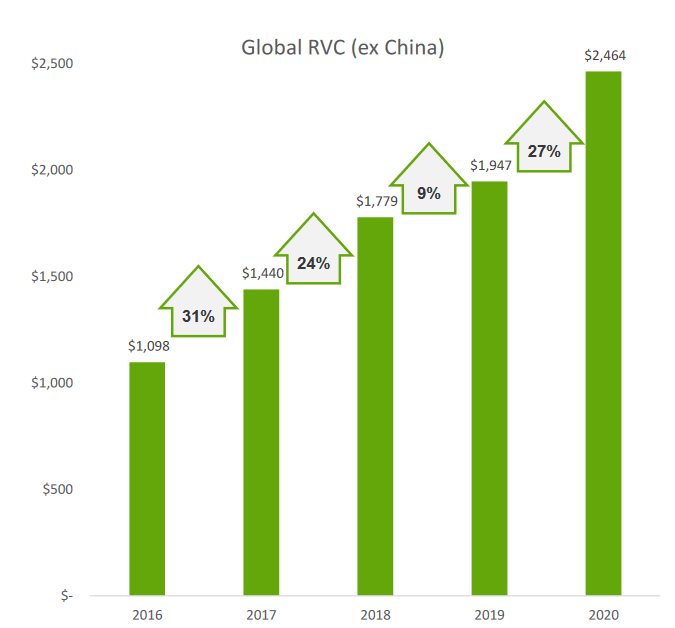

Does dominant but stable or declining market share mean the company is stagnating? Not at all. The market is growing at 25% or more almost every year, leaving plenty of room for new competitors without hurting iRobot revenues.

Source: www.investor.irobot.com

An Owner Led Company

iRobot was founded in 1990, it still have as a CEO the founder, Colin M Angle. 32 years of steady stewardship really paid off. Mr. Angle is now 53, so he is likely to stay onboard for foreseeable future.

His profile is probably one of the most technical you can find among CEOs. A MIT graduate, he previously worked at NASA’s Jet Propulsion Laboratory where he designed rovers. I can see how this level of advanced semi-autonomous vehicle ultimately translated into iRobot product line. So really, Roomba are just one more innovation that spawned from NASA research and talent pool.

The connection to USA’s public spending goes even deeper, as iRobot designed its first commercial product, the PackBot, with funding from DARPA in 1998. This was following several years of research since 1991 with the Genghis and Ariel robot, first experiment to explore robot abilities to move in the real world. iRobot would then go to develop the first Roomba in 2002.

Ariel and Genghis robots, iRobot first prototypes.

Pack bot at work in the Football World Cup

Financials As Solid as The Brand

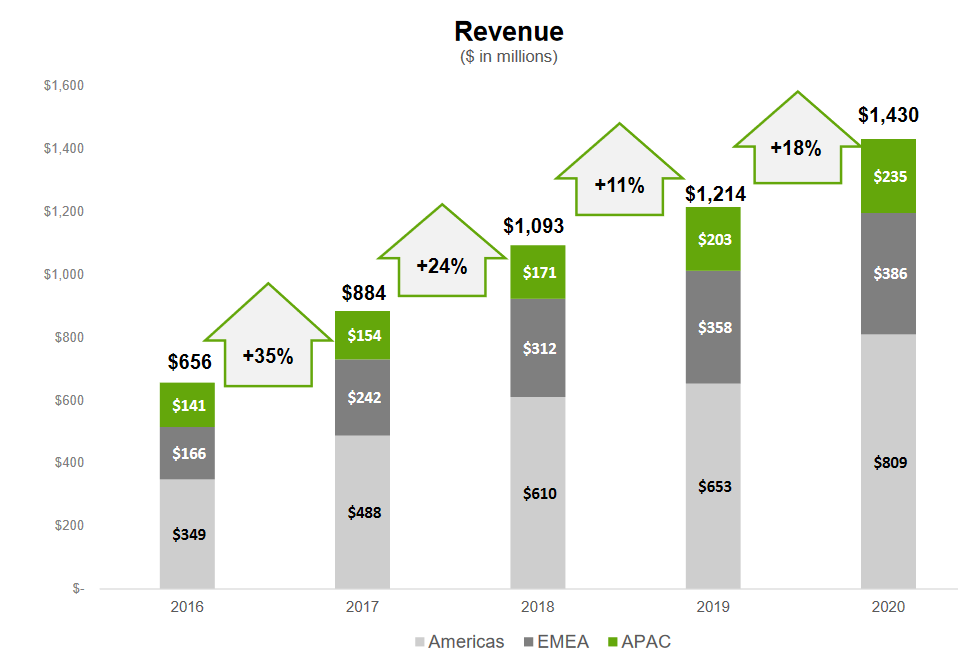

In Q1 2021, the sales of iRobot’s vacuums generated $270M.This was 58% growth from Q1 2020! Part of it is undoubtedly COVID-related, but still very impressive.

On top of that come the newer segment of mopping robots with $33M. And this is not the only new sector the company is expanding into, but we will see that in the next chapter.

Source: www.investor.irobot.com

There are at the moment 19 million vacuum robots in the US, a number that could easily double in the short term, and much more than that in the long run. The growth of robot vacuum is also helped by the digitalization of home, with the latest Roomba made compatible with both Alexa and Google Home.

Just the last quarter, the company generated $29M from operations, adding to its cash treasure chest for a total amount of $500M. This is quite large considering the whole market cap is only $2.5 B. The company have also no debt, so truly, the “real” market cap is more like $2 B.

IRBT’s P/E is now a modest 15, but once corrected for cash on the balance sheet, it is instead 12; something very low for a company with steady growth. Growth was not profitless like so many other tech companies, with net income increasing 15% yearly.

Source: www.finbox.com

Chapter 2: The Growth Ahead

Improvements To the Existing Business

So, we now know how solid the vacuum segment for iRobot and its Roomba is. But is it all the company has to offer? Will it slowly evolve into a slower and more steady technological company that doles out dividends to its shareholders?

I don’t think so. If this was the case, iRobot could still be a good investment, but not an outstanding one. At some point, the vacuum market will be mostly robotized, and growth would stop.

Luckily for us, iRobot management is very open about its plans for the future. One side of future growth is simply to run things more efficiently. Trade wars with China and tariffs have hurt the company’s profit margins in the last few years. This resulted in relocating some of the factories to Malaysia, a costly and slow process getting finished this year.

Higher sales volume also allowed the company to become more efficient in manufacturing and supplying parts.

New Vacuum Products and Offers

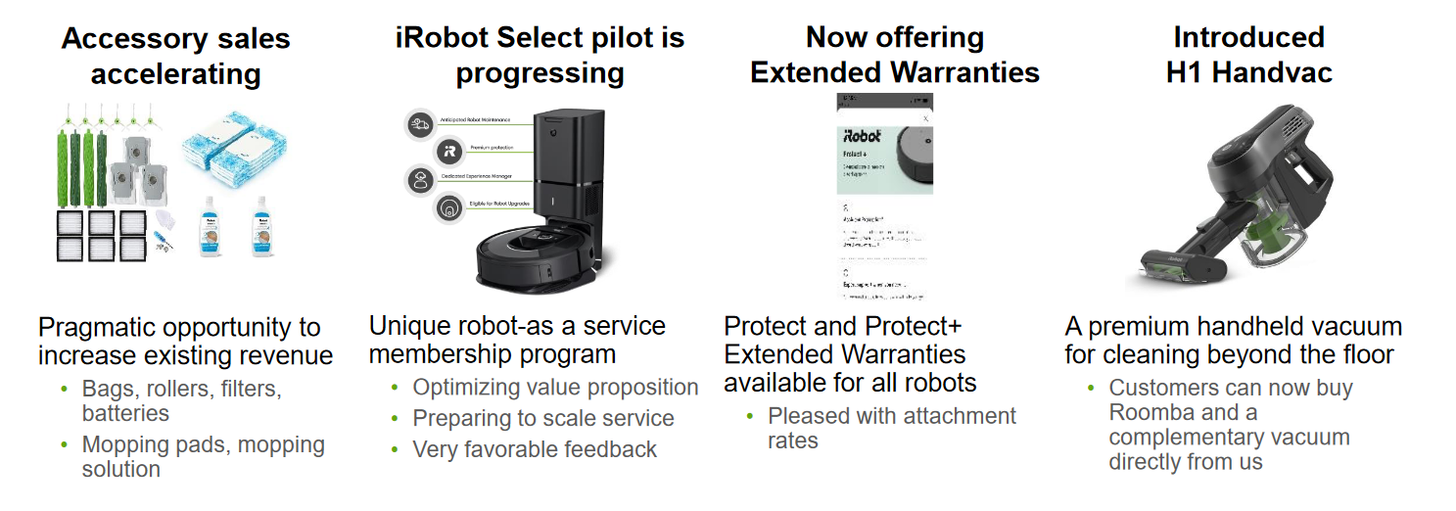

iRobot is also extending its product offer, with for example a handheld vacuum for the corners and furniture the robot cannot reach. It is also strongly investing in improving its technology, with 11% of its revenues invest in R&D.

Extended warranties have also finally been offered, something most consumer electronic sellers know to be a good source of virtually free money (they are always overcharged compared to the real cost).

And finally, RaaS, or Robot-as-a-Service, is now a real thing and not a sci-fi movie title. In practice, it is the option to rent instead of buying a Roomba. Considering the high price point can be a deterrence, especially if you are not sure it will work in your home, this should drive up both revenues and future sales.

Source: www.investor.irobot.com

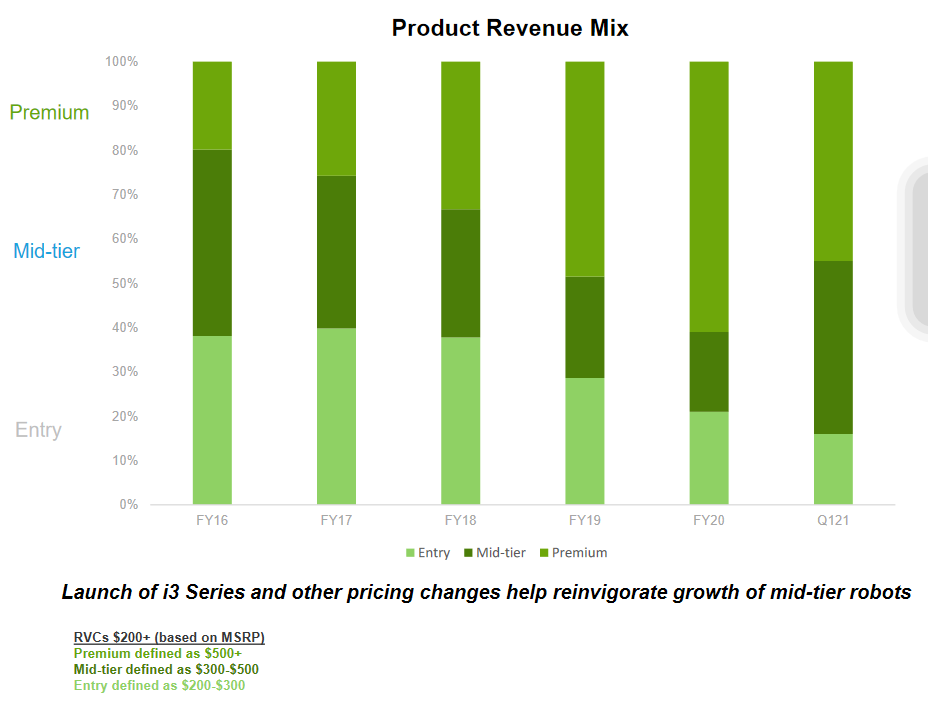

On top of new products comes the progressive adoption of more expensive models. People are (understandably) somewhat reluctant to pay 3-6x more for a robot vacuum than a normal vacuum cleaner.

Here’s the thing: once consumers buy the basic model, they love it. They would never give up the effortless cleaning and all the extra time it creates. But the more basic models might be a little too weak to perfectly clean the carpets? Or, more likely, too dumb to not get stuck in the corner, or avoid the dog’s water bowl.

Once convinced about the product potential, people are much more willing to consider the middle and higher price range if it can allow the robot to do its job without any supervision.

This is exactly what iRobot observed, with premium and mid-tier price range now the large majority of sales, compared to 2016 when adoption was only starting to pick up. Not only the retention rate of previous clients is great, but they tend to buy more expansive models over time.

Source: www.investor.irobot.com

Is The Grass Greener Somewhere Else?

Extension to the house cleaning sector will only bring iRobot so far. There is only so much budget people will put into vacuum cleaners, no matter how smart or practical.

This is why the company is looking for greener pastures (pun intended) in a new sector: Lawn mowing.

Robotic lawnmowers are now where robotic vacuums were five years ago. They are getting more popular, and people are starting to see their neighbors using them, which is instilling consumer confidence.

iRobot is not oblivious to this trend, as the technology is essentially the same, except a lawnmower blade replaces the vacuum system. They had initially planned to launch the Terra robot lawnmower in 2020, but postponed it due to COVID-related delays.

iRobot Terra lawnmower

The company was already in the middle of relocating its production to Malaysia, so risking disrupting even more its supply chain with a new type of device would have been too much.

I imagine easily that management also wanted to see the effect of COVID on sales before risking launching in the largest new market in a decade.

The new launch date for the Terra is not yet decided, and management seems to have become quite discrete about it. I suspect that they used the extra time to do a redesign on the Terra.

Most robotic lawnmowers use a system of cable to delineate the area that should be cut (the grass) and the area that should not (the flowers and bushes). This means that while the technology works, it will not be working for all garden designs. It also means that the initial setup of a robotic lawn mower is quite a hassle, and will take at best several hours, if not days, for the most elaborate gardens.

The most expensive systems bypass this with GPS mapping, but this adds $600-$1,000 to the bill, making it a not so attractive option for most homeowners (it is mostly used currently by parks and corporations).

In comparison, Roomba already uses smarter systems that learn to avoid “sensitive areas” through a process similar to machine learning. If you tell it to avoid somewhere, it will “learn” to do so in the future too. This is already in place for the vacuum models.

The initial design of the Terra was supposed to use wireless beacons, instead of the more clunky cable system. But I imagine that with the recent release of more advanced AI for the home Roomba, the Terra went back to the drawing board to incorporate it and make it truly unique, and the best product on the market.

Because of the 2020 Terra’s cancellation, most comments about iRobot are focused on the vacuum product line. I think this is a mistake, as the return of the Terra, maybe in an upgraded version, is likely to become the next big thing for the company.

The robotic lawnmower market is already growing at 12% a year, despite the offer being far from being attractive: prices are high, setup is really difficult. On top of that, the people the most likely to invest time or money in their garden are the ones with more complex designs and landscaping. And the existing robot lawnmowers simply cannot be trusted to not stray and mow down cherished flower beds and rare plants.

Even with all these limitations, the robotic lawnmower market was already worth $737 million in 2021. If iRobot could capture just 30% of this market (a short target compared to the vacuum segment), it would add around than $221 million of revenue. This would add another 15% to iRobot’s current income and a new source for growth.

Even with troublesome or imperfect geofencing, robotic lawnmowers offer more than just less garden work. They are almost completely silent, which make for good neighbors on Sunday mornings.

Fuel lawn mowers have especially inefficient and polluting engine, to the point that one hour of lawn mowing generate as much pollution as driving a car 100 miles. Robots are in comparison electric, meaning a lot less emissions, something that might get government subsidies in the future. With approximately 20 millions acres of lawn in just USA, this is actually a LOT of pollution right in residential areas.

But I doubt the current robotic lawnmower market tell the whole story.

With the image of quality associated with the Roomba brand and the company’s advances in AI, the market is poised for explosive growth. Especially in the segment of the population the most likely to have been frustrated with iRobot competition. Many of them already using a Roomba indoors for that matter.

As soon as a product they actually can trust gets released, they are likely to give it a try. The Robot-as-a-Service offer recently launched will come in handy for an initial test to convince the skeptics.

Chapter 3: Tumultuous Stock Price Activity

The Short Story

The last year has seen a flurry of speculative activity from both professional and retail investors. None got more attention and headlines than the short squeezes created by a group of Redditors in r/WallStreetBets, managing to corner several hedge funds.

In simple terms, a short squeeze can occur when a fund is shorting a stock and the stock price rise. If it keeps rising, the fund is exposed to margin calls. If it cannot keep covering the rising cost of margin calls, it is forced to buy the stock at any price, pumping it up even further.

Notably, GameStop or AMC have been the most prominent stocks exposed to this. Both were quasi-bankrupted companies whose stock, that due to market manipulations, rose to pretty crazy highs.

What does all this have to do with iRobot? Surprisingly, iRobot fell victim to this shorting scheme early this year.

In January, it rose by as much as 50% in a day. That’s the insanely high black bar on the top of the late January 2021 high in the graph below. Of course, buying at the lowest in the middle of the COVID panic was probably best, but hindsight is 20/20.

The pessimistic opinions about iRobot in March 2020 were the reason for a lot of short interests on the stock. Looking back, I found this article at peak pessimism, that quite literally called the bottom. To sum it up, consensus was negative about tariff-related issues (soon solved with the move to Malaysia), COVID, competition and negative momentum, all making it a “stock to avoid for now”. This article was really a bell ringing for any contrarian looking for an entry point.

Source: www.finbox.com

As you can see, things have calmed down a little since, and the stock price is back to its 2017 levels. To me, this makes very little sense, as the 2021 iRobot is a radically different company than 2017 one.

Here are four things iRobot has accomplished since 2017 that make it a more valuable company today:

- Almost doubled revenues

- Limited exposure to the USA-China trade war

- Increased the value of its customers and brand

- Preparing to take on a whole new market.

But the effect of the short squeeze is for but a moment and the fundamentals are irrelevant to the stock price.

Speculation is seemingly the only game in town these days.

Two Possible Outcomes

Can iRobot stock go even more down, pushed by short-sellers, and abandoned by speculators? Well, obviously yes. Could it go crazy again and explode +50% overnight because it became a meme stock? Yes, again.

Now, you know me, I am not a big fan of crazy speculations and favors instead a steady and “slow” compounding at 15% a year. So, I would never consider iRobot as an investable company based on speculative activity alone.

But as I see it, iRobot is a great growth company that accidentally happens to also be the center of speculative activities. So, regarding the short squeeze situation, I can imagine 2 possibilities:

Possibility #1.

The speculation is over, and less narrative-driven investors will replace the hedge funds and the Redditors battling for iRobot. In this case, everything else in this report still holds, and iRobot is likely to keep growing at 15-20%/year riding the wave of robotization. Even with poor execution from management, this could happen because its market is still growing quickly.

Possibility #2.

The speculation keep going, with wide swings coming in waves. For reference, we can look at how GameStop stock prices have been doing this year. If this is the case, we can expect iRobot to shoot up again at some random date in the future. Then, it will probably be time to sell, cash in a 30-50-100% profit for the year, and come back when things cooled down again.

Source: www.finance.yahoo.com

Is It Still a Company for Value Investors?

I think there is some misconception about value investing when it comes to highly speculated stocks. Key tenets of value investing are to focus on the company’s real value and fundamentals and know to be patient. This causes a lot of value investors to stay away from “speculative” stocks.

But another tenet is to use the unstable moods of Mr. Market to our advantage. If, post short squeeze, other people want to sell us iRobot at a real P/E of 12 and ignore the likely future growth; this is great!

If in a few months, speculation goes rampant again and the stock double, we should enjoy that Mr. Market got exuberant and gave us a 100% yearly return and call it a day.

A value investor does not count on speculation to make him money. He buys businesses below their real value, something made easier by speculation. Most of the time, a value investor return will come from the real-world performance of the business he bought.

And sometimes, speculation will offer him such a high price that he will just accept this gift thankfully and move onto a new undervalued company. Both cases are still value investing, as both cases use the moods of Mr. Market to our advantage.

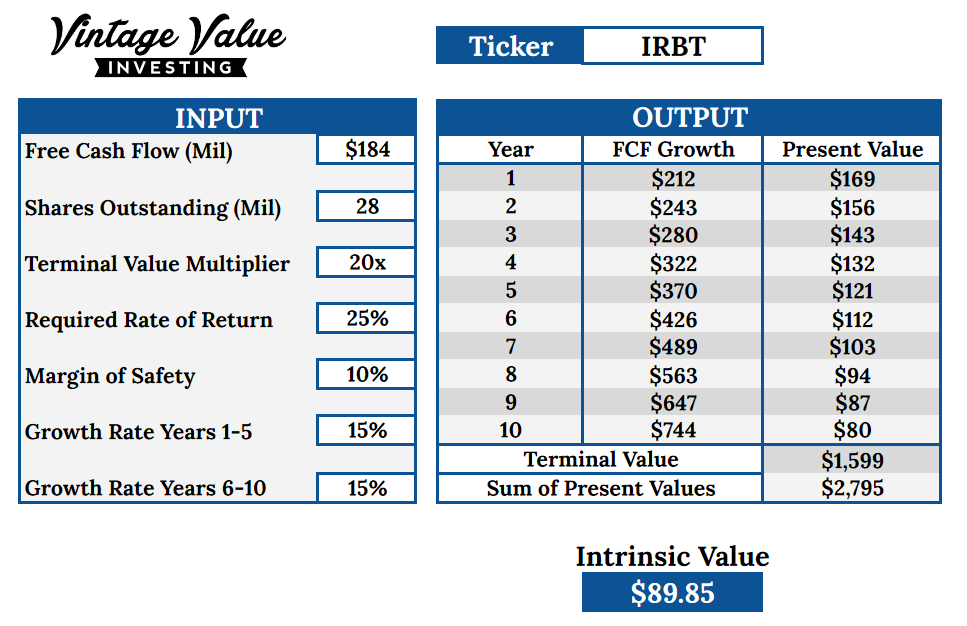

Chapter 4: Valuation

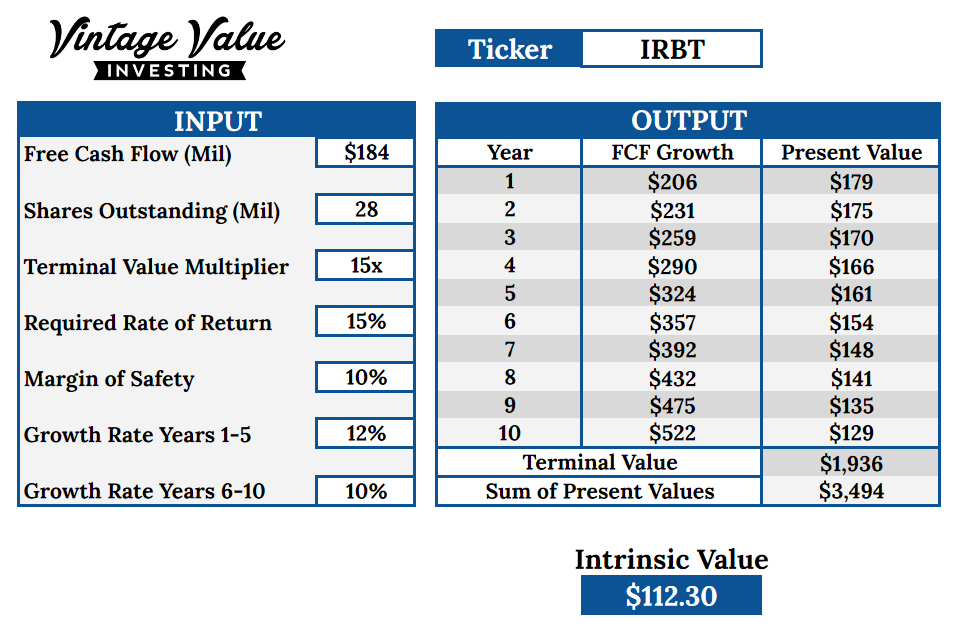

I decided to use the Discounted Free Cash Flow method to value iRobot. As the company is likely to keep growing for at the very least the next 10 years, I think this method is rather adequate.

With a return on invested capital mostly stable between 13-19% over the last decade, I feel I can trust management to make smart decisions about how to reinvest the free cash flow into more growth. The company still being led by its founder, which is an extra nice element about management abilities.

Free cash flow grew in the last decade by 19% annually. I honestly do not feel that this would change anytime soon, but I picked a lower growth rate just to stay on the safe side. Similarly, the final value multiple of 15 is probably a bit conservative.

Even with a target of 15% rate of return, the stock would be significantly undervalued at the current $88 and have an intrinsic value of $112. Funnily enough, it means it was not overvalued, but just at fair value the day after the highs of the short squeeze. So irrespective of speculative activity, iRobot seems to be a good prospect for a consumer electronic growth stock.

I wanted to see how far the stock returns could go if all the stars aligned and the free cash flow growth continue unhindered. With 15% growth in the next 10 years and a bit more realistic multiplier, this could go up to a 25% of return. Not bad at all!

Conclusion

I have been thinking for a while about how to play some secular long trends. Automation is one trend that will impact us all, like it or not.

We know that many jobs will be automated away. We also know the road ahead will be bumpy, with likely backlash from the general public and/or governments. However, how to invest in automation is not that clear.

An extra problem about predicting the future of innovation is picking the winner. While it was obvious automobiles were going to replace horses, finding which of the thousands of automotive companies was going to become Ford or GM, and which was going to die on the way, was far from easy. Most technological revolutions played out this way, from railroad to cars to internet companies.

So instead of trying to forecast much more complex automation innovations, like self-driving cars, why not do it differently? Let’s find a lucrative, quickly growing niche market where technological issues about automation have already been solved.

A sector with a clear winner controlling 50-75% of the market, and where automation is welcomed and not feared.

The domestic robot market and iRobot seem to be the safest and easiest way to bet on automation, at least on the consumer side. The recent speculative interest is potentially a way to make a quick buck, but the real value of iRobot is in its brand, its growth, and the low multiples at which the stock sells for right now.

With time, components and technology will keep getting cheaper and better, almost guaranteeing the constant growth of the market. With lower prices, the trouble of doing it manually will be less and less worth it, up to the point where even a minimum wage worker will be better off not wasting his time. Corporate use of robot cleaners is also likely to increase.

It is likely that in 10-20 years, all vacuum cleaners will be robotic, and small hand-held devices will be used to finish the trickiest corners. The same is true for robotic lawnmowers. This gives iRobot an addressable market of tens if not hundreds of billions, where its brand will be by far the most recognized.

The future is likely to be robotic, but not so much creepy humanoid robots, but more likely cute little droids roaming around. The same trend is at play for many other customer-facing robots, like food and parcel deliveries.

A friend of mine lives in Estonia, a European startup hub, and no less than two local startups are following the path of iRobot. No one feels threatened either by the Starship Technology delivery robot, roaming around to deliver ice cream or a pizza. Or by the Cleveron parcel delivery robot.

For that matter, the cash-rich iRobot might even look at such startups and use its $500 million cash for acquisition and expansion in further other markets. Or launch its own, adapting the same technology that made the Roomba so efficient.

For now, the tight focus on vacuum and soon lawnmowers is commendable, but five years down the road, I see the potential for further growth in new sectors.

Droids on the roads and sidewalks, and Roomba in the houses and gardens, the workless Sci-Fi Utopia is maybe just around the corner, and we are simply not realizing it…yet…

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in IRBT and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.