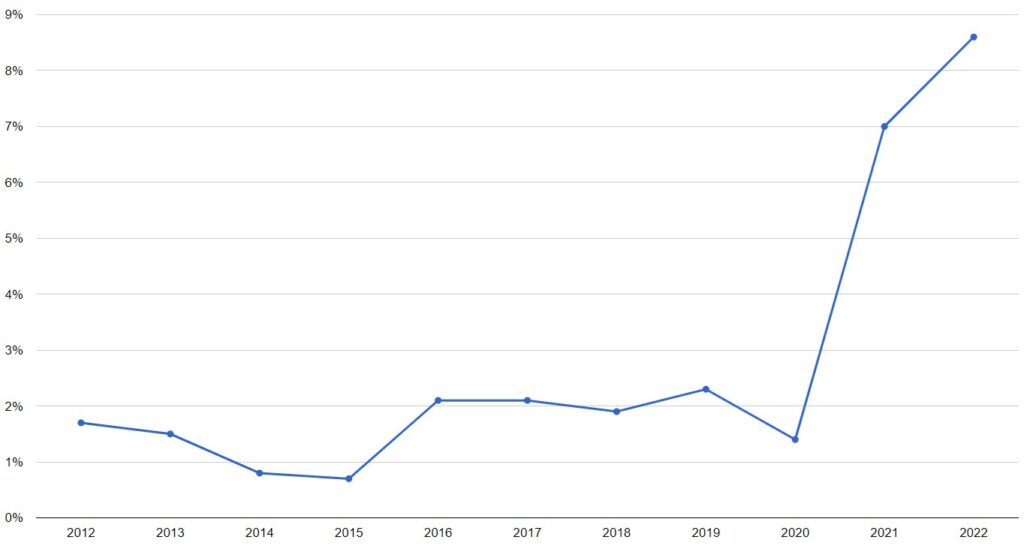

Inflation has become the dominant economic trend of 2022. Prices began spiking in 2021, and in 2022 inflation reached 8.6%. Rising prices have had a significant impact on American consumers.

Price increases have been largely driven by increases in the prices of key needs like gasoline, electricity, food, and household goods, hitting Americans solidly in the pocket.

Many Americans have never experienced serious inflation before. This price surge follows almost 30 years of relatively low inflation, with the last serious spike coming in 1980. That has left many consumers struggling to cope with a new and unfamiliar reality.

Chart: United States Annual Inflation Rates (2012 – 2022)

We’ve all seen articles advising people on how to cope with inflation, but what are American consumers actually feeling, and what are they actually doing to keep up?

We wanted to know, so we asked.

Key Findings

- 95.7% of Americans, regardless of their income level, say they are worried about rising prices and are doing something in response.

- The rising prices of gas, food, utilities, and housing have had the most significant impact on people’s finances.

- The most widespread financial choices made as the result of rising prices are delaying buying a car, canceling vacations, and delaying paying down debt.

- Over 15% of Americans already had to borrow money or take on credit in order to cover expenses.

- 50% of people of all genders, ages, and income groups are cutting back on dining out and driving less than normal.

- 16% of people say that they had to get a second job or take on a gig in order to keep up with the prices.

Survey: The Impact of Rising Prices on Financial Choices and Behaviors

We asked a nationally distributed group of Americans a series of questions designed to assess their perceptions of inflation and what they are doing in response to price increases.

Q: How Worried Are You About Rising Prices?

A huge majority of respondents, 95.67% of them, were either “somewhat worried” or “very worried” about rising prices, with an absolute majority in the “very worried” category.

These proportions held up very consistently across gender, age, and income lines

As you might expect, the highest percentage of “very worried” responses came from the lowest income bracket and the lowest percentage came from the highest income bracket. What’s unexpected is that even in the highest income bracket only 3.85% say they aren’t worried at all.

Takeaway: Low-income Americans are most concerned about rising prices, but concern is present through all income brackets, even the highest ones surveyed.

Q: Have the Rising Prices of Gas and Other Consumer Goods Made You Rethink You Financial Choices or Changed How You Spend Money?

Over 50% indicated that inflation has forced them to reconsider the way they manage their finances, and under 10% replied that they had not found any change to be necessary.

When we look at a detailed breakdown, we see that people from age 30 to age 60 had the highest rate of positive responses, suggesting that people in age brackets likely to have families are feeling substantial stress.

In the income breakdown, we see that – as expected – people with higher incomes are least likely to have had to reassess financial choices, with one anomaly in the $125,000 to $149,000 bracket.

It may seem initially surprising that fewer people in the $10,000 to $24,000 bracket saw the need to change than in the next higher income bracket, but that may be because people with incomes that low were already doing everything in their power to reduce spending.

Q: The Rise of Prices in What Category Has Had the Most Significant Impact on Your Day-to-Day Life?

Here the leading roles played by gas, food, utilities, and housing are entirely expected, as these are expenses that most people can’t cut out and they are also areas in which price increases have been most pronounced.

Q: Which Of the Following Financial Choices, If Any, Have You Made Because of Rising Prices?

Here, again, we see expected results. Looking for ways to cut costs is a generic statement that includes most of the subsequent options, so it naturally has the highest positive response rate. Delaying buying a car makes sense, given the extraordinary increase in the prices of both new and used cars, and delaying a home purchase is a natural decision with both interest rates and prices rising.

Delaying debt payments and borrowing money are also common, but they are risky options that indicate that substantial numbers of people could find themselves in more trouble in the near future.

The detailed breakdown is, naturally, more revealing, if not always easy to explain. All ages, genders, and income levels saw from 68% to 82% looking for ways to cut costs and save.

Higher-income people were most likely to have delayed buying a car (though it was common at all income levels), presumably because they are more likely to already own serviceable vehicles. People between 18 and 44 were, not surprisingly, more likely to have postponed a wedding.

Some figures are less easy to explain – the $125,000 to $149,000 income group seemed to run up a high rate of responses in an unusual number of categories – and would require more research to explain or dismiss as statistical anomalies.

Q: Which of the Following, If Any, Have You Done to Save Money as Prices Rise?

Here we see a predictable dominance of saving methods that involve reducing or eliminating discretionary expenses and looking for better deals. Those are normally the first steps people take under pricing pressure.

In the detailed breakdown, we again see remarkable consistency across groups in many areas. All genders, ages, and income groups saw around 50% cutting back on dining out (not good news for restaurants). A large majority of categories saw between 40% and 50% choosing to drive less.

Higher-income Americans reported taking steps to reduce spending at nearly the same – and sometimes greater – rates than groups with lower incomes. We might not expect to see 70% of respondents with incomes between $175,000 and $199,000 shopping around for better prices and almost 60% using coupons and discounts, but that’s what the numbers showed.

What Do The Numbers Reveal?

We won’t pretend that this survey is the last word on the topic. The sample size is limited and there are many more questions that could be asked. At the same time, the figures do point to some conclusions.

The clearest takeaway is that both concern over rising prices and concrete actions based on that concern cut across the full spectrum of respondents. Even respondents in the higher income brackets demonstrated concern over rising prices and indicated that they were making changes in their spending and money management habits to adapt.

Another takeaway is that a significant number of people across all income and age brackets have already taken the most obvious steps toward managing inflation. They are already shopping for bargains and cutting back on discretionary expenses.

That leaves the question of what comes next if inflation continues. Significant numbers of people are already delaying debt payments, taking on debt, and cutting back on investing. Those numbers are likely to grow. These may be rational or even necessary steps in the short term, but they can have risky long-term implications.

The last conclusion is something most of us already know. Inflation is a serious burden and it’s getting worse. We all have to deal with it in our own way according to our own needs and capacity. We’re all going to be watching carefully to see how long this goes on and whether traditional methods like rising interest rates can stop it.

Understanding inflation can help, but for the average consumer, the focus has to be on coping. We hope this survey will give some indication of how others are doing that!

About This Survey

The survey responses were collected from May 19 to May 20, 2022, via SurveyMonkey, with a total of 578 participants from across the USA. Respondents represent a national sample balanced by census data of age, gender, income level, and region. The survey had a margin of error +/- 4.159% with a 95% confidence level.

Copyright Information:

All the data included in this study is available via public domain. This means all statistics may be copied without permission. We do, however, appreciate citation as the source via a link.