Bonds are an important asset class, and almost any balanced investment portfolio contains a bond allocation. Bond investing is often a good idea for beginners, especially if you are seeking to invest in relatively stable income-generating assets.

When you buy a bond, you are lending money to the entity that issued the bond. You receive interest payments in return. You can hold the bond until it matures and then get your money back, or you can sell it before maturity.

Here’s everything you need to know before you start investing in bonds.

Types of Bonds

You can invest in different types of bonds, depending on your portfolio requirements and your risk appetite. The major bond types that you should consider include:

🏛 Treasury Bonds

The US government issues these bonds. When you buy treasury bonds you are lending money to the US government. Treasury bonds carry a very low risk of default, and as a result, they offer a relatively low interest rate.

🏘 Municipal Bonds

US states, cities, towns, or other government entities issue municipal bonds. The issuer usually has a specific public project they want to finance through these bonds. These are also very secure. Interest rates are higher than those on treasury bonds, but still relatively low.

🏢 Corporate Bonds

Private companies issue these bonds to raise money. The risk of default is relatively higher in corporate bonds, so they offer relatively higher interest rates. Corporate bonds range from highly rated bonds from major companies, which carry low risk and pay low interest rates, to very risky high-yield bonds from small or unstable companies.

About Bonds: the Key Concepts

It is important to understand the features that distinguish different types of bonds. This will help you make choices that match your investment needs.

Maturity

The maturity date of a bond is a key consideration because individual investment horizons may differ. On the date of maturity, the issuer’s bond obligation is over, and you will get back the principal amount of the bond.

👉 Short-term bonds typically mature within 1-3 years, medium-term bonds range from 4-10 years, and long-term bonds have maturities exceeding 10 years.

Secured vs. Unsecured Bonds

If a bond is secured, the issuer will pledge certain assets as collateral to the investors. If the issuer defaults on their repayment obligation the collateral can be used to pay the debt.

Unsecured bonds, also known as debentures, do not have any collateral backing them. As a result, the risk of the bondholder is significantly higher.

Coupon

The yearly or half-yearly interest paid on the bond to the investors is represented by the coupon amount. The coupon is also known as the nominal yield or the coupon rate of the bond.

👉 To calculate a particular bond’s coupon rate, you can simply divide the yearly interest payment amount by the bond’s face value.

Taxation

When comparing the actual yield between two types of bonds, you should always factor in the taxation.

👉 Treasury bonds are subject to federal income tax but exempt from state and local taxes. Municipal bonds are generally tax-exempt at the federal level. In a tax-exempt bond, both the interest income and any capital gain from selling the bond will not attract any tax. However, the interest rates for tax-exempt bonds are usually lower.

👉 Corporate bonds are almost always a taxable investment, but their interest rates are usually higher.

Callability

Some types of bonds can be paid off by the issuer before maturity. If the prevailing interest rate environment allows the bond issuer to borrow at a lower rate, they may choose to call these bonds. From the bondholder’s perspective, the advantage of callable bonds is that the coupon rate will usually be more attractive.

You will hear these terms in any discussion of bonds. Understanding them will help you select the right bonds for your portfolio.

📘 Our complete guide to investing basics: Investing For Beginners

Bond Prices and Interest Rates

Bond investing is closely tied to interest rates. Interest is how you earn money on bonds, and understanding interest is a core part of understanding bonds.

Bonds and interest rates have an inverse relationship.

👆 If interest rates rise after a particular bond was issued, its market price will usually decline. This happens because the coupon rates of new bonds are likely to be higher because of the higher current interest rate, which makes the previous bonds less attractive for buyers.

👇 If interest rates are going down, the market price of the previously issued bonds will increase. As a result, an existing bondholder might be able to sell the bond for more than their buying price.

You can also understand the correlation between bonds and interest rates in terms of price and yield. The yield represents the return on the bond investment expressed as an annual percentage. The price is the current market value of the bond, which is based on the amount of the bond and the expected interest income for the remaining time until maturity.

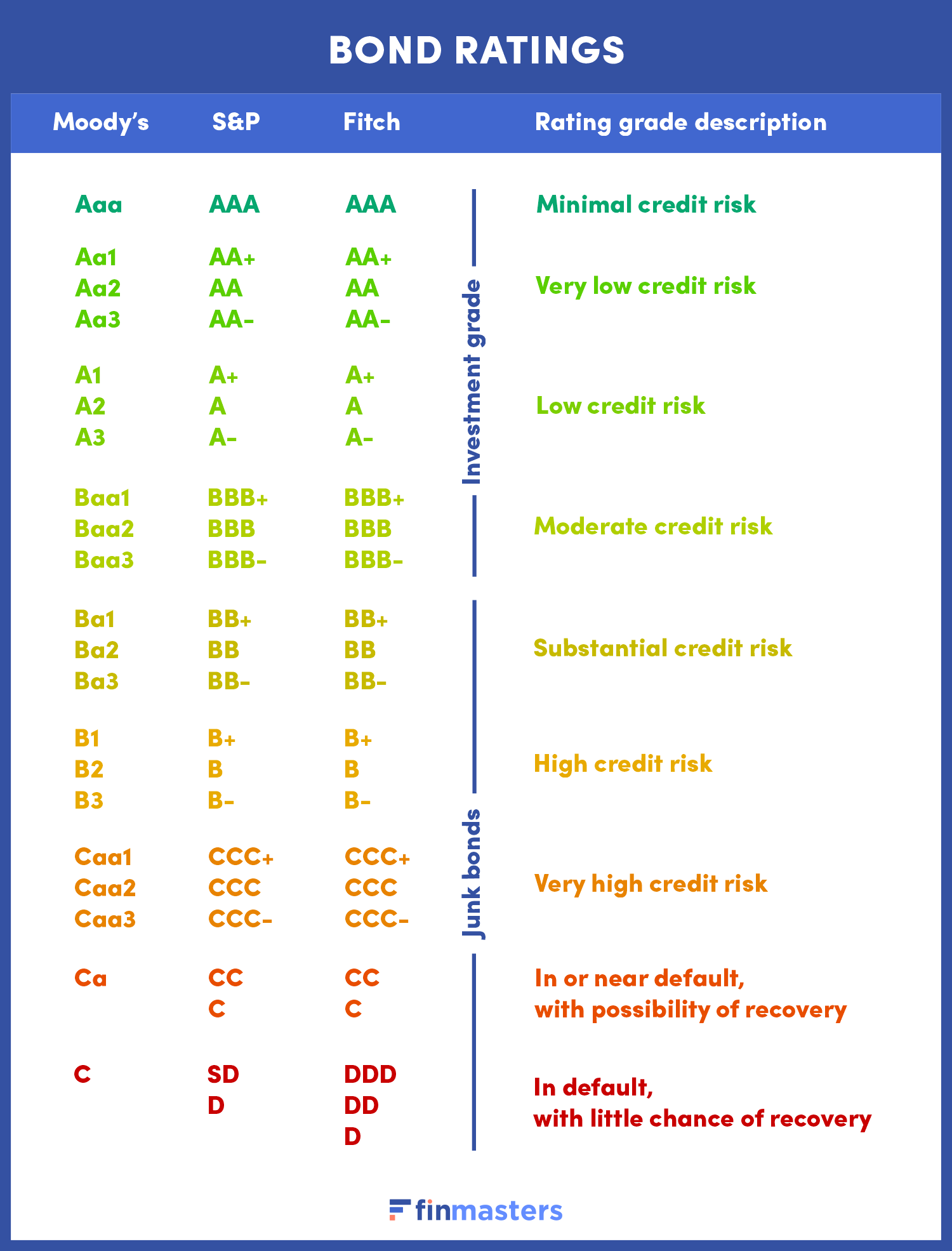

Bond Ratings, Risk, and Yield

Globally recognized ratings agencies, such as Standard & Poor’s, Moody’s, and Fitch independently evaluate how creditworthy a particular bond is. These raters use multiple parameters to assess the bond issuer’s financial health and assign ratings. Any downgrade or upgrade in ratings can affect the market price of the bonds.

Bond ratings fall into two broad categories:

- Investment-grade bonds have a rating of Baa3/BBB- or higher.

- High-yield or junk bonds have a rating of Ba1/BB+ or below.

👉 The first rule of bond investing for beginners is to assess a bond’s risk tolerance and consider the possibility of payment default before investing.

Non-investment grade bonds or junk bonds pay high interest rates, and may catch the fancy of many new investors.

Junk bonds can seem like a compelling proposition when you consider the promise of receiving substantial checks in the mail. However, if the issuer goes bankrupt, you may stand to lose your entire investment. If you are not sure of what you are doing, play safe and stick to AAA-rated bonds.

Different rating companies use different rating systems, so you may see ratings that seem different. Understanding bond ratings will give you a better picture of how bonds are evaluated.

Managing Risk Through Bond Diversification

Bond diversification is a logical way to spread your risk, particularly if you have a significantly large bond portfolio. You could diversify your portfolio by choosing bonds from different geographies (within and outside the US), different types (government, municipal, corporate, zero-coupon, callable, and inflation-protected), maturity period, and credit quality (bond rating).

💡 Considering the relative safety of US government and municipal bonds, and the inherently lower volatility in this asset class, even a less diversified bond portfolio could sometimes serve the purpose in your overall investment portfolio.

If you are retired or only a few years away from retirement, it is usually better to minimize your risk rather than trying to maximize yield.

Bond Funds and ETFs

Bond investing for beginners as well as for more experienced investors can be simplified when you invest through bond funds and ETFs. A bond mutual fund, popularly known as bond fund, will pool money from a large number of investors to buy bonds. This provides diversification and professional fund management to an individual investor.

A bond fund may specialize in municipal bonds, corporate bonds, or non-investment grade bonds.

It is also possible to invest in bond ETFs, which an individual investor can buy just like stocks. If you are looking for a more effective risk-reward approach to bond investing, a bond ETF might be a judicious choice.

📘 Our complete guide to mutual fund investing basics: Mutual Fund Investing For Beginners

Bond Fees

The relative financial performance of a bond fund will be affected by the fee you may have to pay, especially when the prevailing interest rates are low.

👉 Active bond funds are being regularly traded, called, and maturing. Active fund managers will charge a higher fee, and may sometimes struggle to add value over and above the higher expense ratio.

👉 Passively managed funds, on the other hand, will mostly have a low turnover. Passive bond funds will have a lower cost because of their minimal management expenses.

Each time you sell or buy a bond, you pay a commission known as a bond spread. Higher bond spreads can reduce your returns.

Risks of Bond Investing

Bonds are an excellent investment vehicle, especially when you want to generate an income. However, bond investing for beginners requires that you learn of the potential risks and pitfalls of different types of bonds. Here are some of the key risks that you should take into account before investing in bonds:

Interest Rate Risks

If the interest rates start increasing, your existing bond investments may start losing their market value. That’s because new bond issuances at higher interest rates will be more attractive for investors compared to your existing bonds, which you locked in at lower rates.

Callable Bond Risks

In a market environment where the interest rates are falling, the issuer of callable bonds may exercise the option to call the bonds. This way the issuer no longer has to pay you the high interest which you have originally locked-in. In this situation, you could be left with excess cash that you may find difficult to reinvest at a comparable interest rate.

Risks of Bond Default

When you invest in bonds, you are simply lending money to the issuer as debt. If the bond issuer goes bankrupt, you could lose your entire principal amount invested. Corporate bonds, in particular, are inherently risky. They are not guaranteed by the US government or any government entity. You are solely dependent on the bond issuer’s ability to repay.

Should You Invest in Bonds?

If you have your finances under control and you are committed to learning and investing responsibly, investing in bonds can be a good decision. Before you go ahead with a particular bond investment, you must carefully weigh whether it is in sync with your portfolio goals and investment philosophy. When you want to mitigate the volatility in your portfolio or create a steady income, investing in bonds may be a prudent choice.

Younger investors often give more weight to stocks rather than bonds in their portfolio. As you near your retirement, the balance should probably tilt more in favor of bonds. Your financial position, income levels age, and risk tolerance all influence your bond allocation.

📘 Our complete guide to stock investing basics: Stock Investing For Beginners