November 20th, 2021

Quick Stock Overview

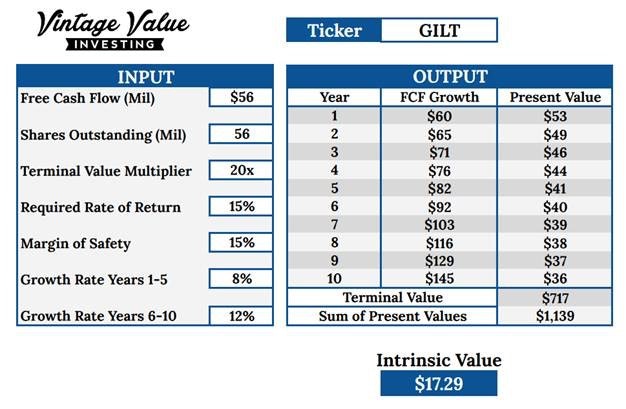

Ticker: GILT

Source: www.stockrover.com

Key Data

- Sector: Technologies

- Sales ($M): 85,594

- Industry: Communication equipment

- Net Cash per share: $0.99

- Market Capitalization ($M): 476

- Equity per share: $4.05

- Price to sales: 2.6

- P/E: 10.2

- Price to Free Cash Flow: 8.5

- ROIC: 19.4%

- Dividend yield: 11.7%

- Free cash flow / share: $0.99

Investment Thesis

The Space Tech Comeback

You may not know this, but I am an avid space enthusiast. Even though I ended up working for the US Navy, space has always been something I have been especially fascinated with.

I think it’s safe to say that progress within the space industry has been disappointing for a long time. In my short 28 years of life, we have made so little progress in space that it seems impossible to accomplish anything of importance.

After Armstrong’s first steps on the moon in 1969 and after the last man on the moon in 1972, the space industry has stagnated, with at best incremental improvements. Yes, we put some rovers on Mars and constructed a few satellites. By far the most valuable space innovation has been the GPS. As a result, public enthusiasm for space technology has declined.

Global warming, social and political issues have dominated the world’s attention for a long time. Talks of space expansion were reserved for more optimistic times.

Thanks to the private sector, this perception has changed. We began with SpaceX founded by Elon Musk, then Blue Origin founded by Jeff Bezos. By cutting launch costs drastically, these two billionaires have re-energized the space industry.

Even if many see it as a waste of resources, I am delighted to see some life brought back to a field so long dominated by bureaucracy and conglomerates. Now NASA plans to return to the moon with the Artemis mission and the Chinese and Russians are planning their own permanent moon base.

Musk still wants to go to Mars, and Bezos wants to build a space habitat in Earth orbit. At the same time, the Russians are trying to stay in the race, and the Chinese are feverishly catching up with the other space giants.

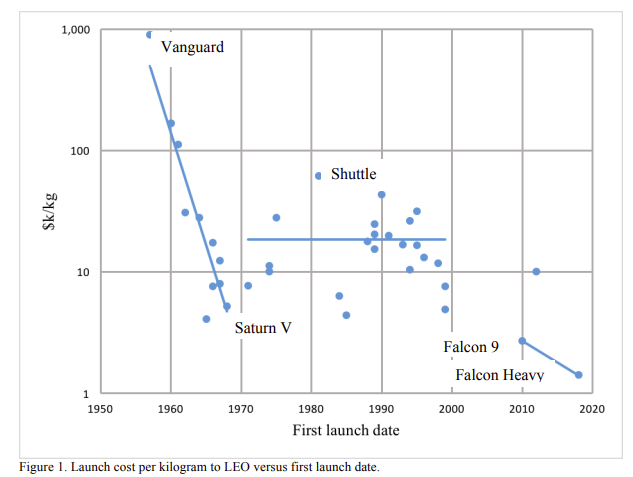

All participants are developing new launchers to reach these lofty goals. In addition to being larger, they are much cheaper as well. In just a decade, it went from $54,500 per kg to $2,720 per kg; a 20-fold decrease!

This is largely due to re-usability. Up until recently, rockets were destroyed upon launch. Think of it this way: every time United Airlines offered a commercial flight, the company simply scrapped the plane afterwards.

Imagine the cost!

SpaceX changed that, and the rest of the industry is following them. The later fully reusable and larger rockets like the Falcon Heavy (and soon-ish the Starship) should bring costs even lower.

Source: ttu-ir.tdl.org

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

The Satellite Boom

Often, people think that satellites cost a lot because of the very complex technology in them. But that’s not true. It is common for the launch cost to be as high as that of the satellite. Hence, reducing the cost of a kilo in orbit by a significant amount is important.

In the past decade, global launches averaged around 25-30 per year. For its Starlink project, SpaceX alone is building 120 (lightweight) satellites each month. Within a few years, Starlink hopes to offer high-speed Internet from satellites in Low Earth Orbit (LEO) anywhere on earth.

No fewer than 42,000 satellites will be launched simultaneously for this purpose. A similar plan has been laid out by Blue Origin and Amazon, with “just” 3,236 satellites planned. As you can see, the sky is no longer the limit for satellites.

I have been wondering how to invest in this trend for a while. However, Blue Origin and SpaceX are private companies. Since their backers are the richest men on Earth, they have no need to raise more funds through an IPO. Musk is notoriously volatile when it comes to public governance, and Bezos is attracted to the absolute control he has as the sole owner.

As a result, I had given up on trying to profit from the new space race since the main culprit was outside the public investing universe. This is until recently a company popped up on one of my screens.

Gilat Satellite Network manufactures equipment for satellite communication systems. As I delved deeper into the company’s business profile and financial metrics, I became more and more interested.

So, let’s jump into orbit …

Chapter 1: Making Sense Of Satellite Telecommunications

A Key Component of Telecommunication

There are three main components of satellite telecommunications. They are the satellite manufacturers, the launchers to launch them into orbit, and the ground-based operators.

The focus of this report will be on the ground. Essentially, satellites are connected to the rest of the world’s communication network (internet fiber, mobile networks, etc.). The signal travels through small antennas and dedicated electronics.

Some of Gilat antennas

Ground stations are also responsible for coordinating and optimizing the flow of data from and toward space. In this video, from 22:30 to 23:30, you can see an example of pointing the beams in the right directions, changing satellites, when necessary, etc.

Obviously, this is a very complex and technical field. The explanation of how it works would extend far beyond this report. An engineering degree is probably the minimum requirement to understand that. I will also avoid acronyms whenever possible.

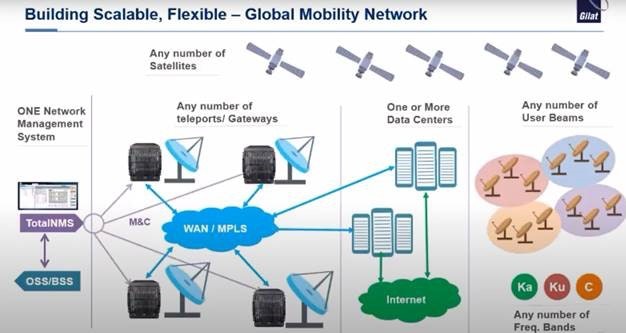

Here is a slide from the company to illustrate why I think explaining each component one by one would make this report unreadable.

As a business model, however, it can be understood.

Telecom operators need the expertise and equipment provided by companies like Gilat to handle exchanges with satellite constellations. The product’s benefits are easy to understand, even if we aren’t experts in its technology.

Access to data and connection everywhere, at all times.

Gilat charges a fee for providing it.

Due to the rapid changes in the market, these fees will soon multiply.

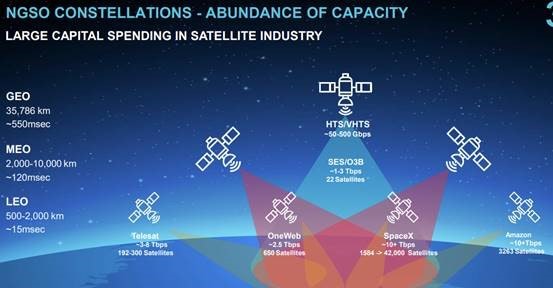

The Roaring LEO

With the move away from geosynchronous satellites, the industry is experiencing a great deal of change. Until recently, the main way to put a satellite into a distant orbit was to keep it hovering above the same area of Earth all the time. When you have a few dozen satellites orbiting the Earth, you have worldwide coverage.

In this case, the problem is that geosynchronous orbit (GEO) is 35,000 kilometers away from the Earth. In terms of communication, this is a problem, since the signal has to travel a long distance back and forth. Due to the huge distance, data travels at a low speed.

Television broadcast satellites did not have this problem since they usually receive only one input (the TV program) and transmit only one output (the TV show) over a vast area. This was also fine for satellite pictures, monitoring an oil rig, and other data.

As data travels up and down from multiple sources on the ground, it is not so great for Internet data transfer. In this case, slowness is synonymous with poor quality. Consumers and businesses want and need high-speed, low-latency Internet.

GEO satellites are just not good enough for modern purposes. A satellite Internet connection might allow you to send an email and (slowly) browse the web, but you can’t stream, play games, or make a group Zoom call.

It was also expensive because GEO orbits were rare and large, heavy satellites were required. Imagine how much money we used to spend on phone bills and how bad the performances were with 56k modems, but with modern needs.

“The industry conversation has changed from requiring megabits per second to gigabits per second.

The Internet is no longer mainly the provider of content, but the platform for considerable data sharing requiring high bandwidth”

Source: Gilat Investor Presentation

The trend is now towards non-geostationary orbits (NGSOs), especially low Earth orbit satellites (LEOs), to solve the problem.

That’s a mouthful of acronyms. The idea is for you to understand that we are moving from a few large, very distant, and expensive GEO satellites to a swarm of smaller, much closer, and cheaper LEO satellites.

A Whole New Gigantic Market

Instead of ground-based mobile phone towers, LEO satellite constellation will provide 4G/5G connectivity via satellites.

Not only is this a huge increase in satellites to manage, but it also means an exploding market. Previously, this was an expensive service for remote areas, but now it will compete with Internet companies like AT&T for most rural areas.

While SpaceX’s Starlink is the most ambitious LEO constellation, Amazon, OneWeb, and Telesat are also working on it. You can count on other companies or countries wanting to grab a piece of this pie soon as well.

It will simply have no competitors in developing countries. Neither in price nor in performance. Outside of the main cities already covered by cell phone operators, developing countries’ countryside is likely to immediately switch to satellite internet.

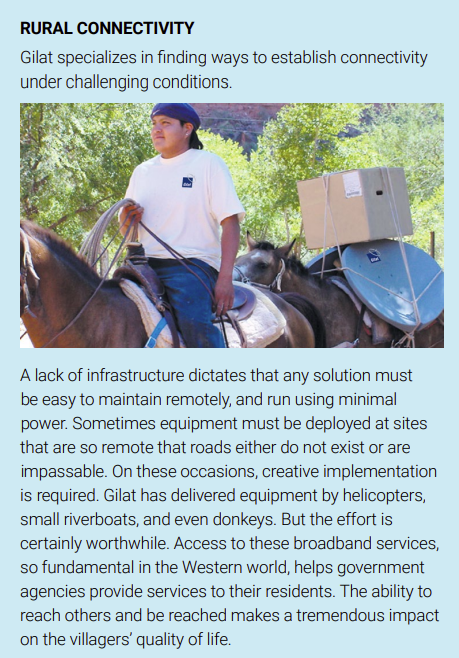

This is similar to the way mobile internet took over before landline Internet ever became available. The country of Peru, a very mountainous country with remote regions, falls into this category. Through a partnership with Gilat, it is bringing the Internet to millions of people. The Peru project could serve as a template for similar projects in many other nations. Southeast Asia, for instance, would be a suitable candidate.

Additionally, I appreciated the company’s problem-solving abilities. Somehow or another, the devices need to be deployed. It does not matter if the equipment is delivered by riverboat or even by donkey!

Source: www.gilat.com

Chapter 2: Gilat’s operations

The Main Segments

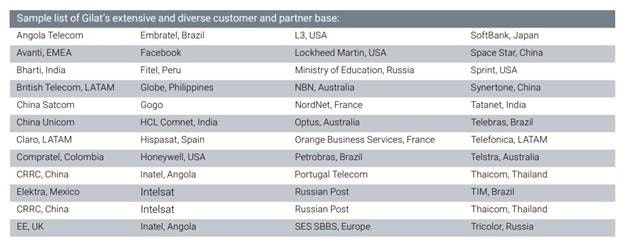

Gilat’s activities are divided into different segments, each of which caters to a different type of client. As a result, the company can use the same basic connectivity technology but tailor it to the needs of each user.

The company has developed a large customer base over 30 years, expanding with the whole satellite industry. There are a lot of impressive clients for Gilat, including Facebook, Petrobras, Lockheed Martin, and Softbank.

The company mostly makes money in the Americas, with the rest of the world accounting for about a third of its revenues.

Cellular

https://www.gilat.com/solutions/cellular/

A mobile phone service operator can use this service to deploy their mobile network over satellites. It is also known as Cellular Backhauling, or CBH. A satellite-based solution is used in place of a traditional mobile phone tower.

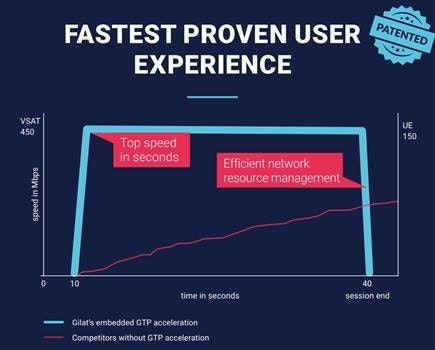

Up until recently, the main market here was 3G backhaul. One of the company’s notable achievements was deploying 3G connections to Brazil and Canada. Now the company is focusing on more internet-friendly 4G. To describe Gilat as dominant would be an understatement. The company controls 80% of the CHB 4G market!

The reason Gilat’s dominance is due to GTP (General Tunneling Protocol) is that it allows connections to be established very quickly, instead of requiring a sluggish process. With Gilat patents, there is no need to wait 40 seconds for the connection to reach full speed.

In an age when LEO satellites have become commonplace, phone companies will increasingly use Gilat technology to connect rural areas instead of traditional towers.

Mobility

https://www.gilat.com/solutions/mobility/

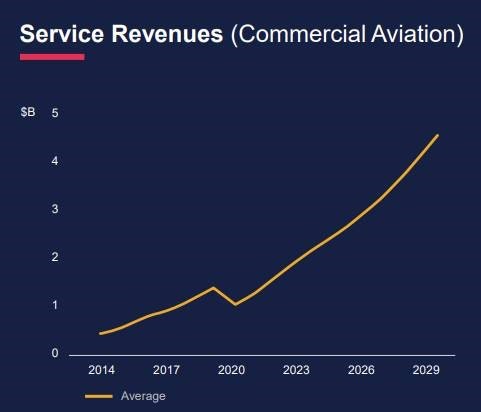

Delivery of the Internet to moving targets is a difficult technical challenge. This is particularly true if you want uninterrupted data transmission. If you are doing it far away from the mobile network, it will be even more so.

If it weren’t for satellites, it would be impossible to deliver Internet at sea (merchant ships and cruise ships) or in high-speed trains and planes.

The market has also doubled since 2015 and continues to grow quickly. By 2025, it should grow another 20-30%. In-flight entertainment increasingly includes free WiFi, and internet access is increasingly essential for ships.

Internet of Things (IoT)

https://www.gilat.com/solutions/iot/

I am not the most enthusiastic about the Internet of Things. As a rule, I prefer my personal items to be “dumb” and functional, as opposed to smart and connected. I don’t need my fridge to run on Windows and be connected to the Internet.

But there is one field where IoT makes perfect sense, and that is in industrial settings (IIoT). Gilat uses pipeline monitoring on its website as the perfect example. Gilat systems monitor 700 locations for leaks or potential issues so that Philips 66 can respond quickly.

An always-on monitoring system based in the sky is the best option for sensitive or dangerous activities.

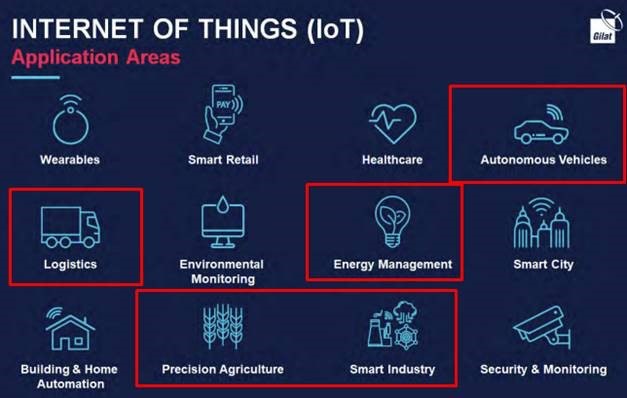

Gilat provides a useful infographic depicting all the possible applications. My two favorites are:

- The industrial/energy/agriculture segment

- The logistics and autonomous vehicles segment

Source: www.gilat.com

Industry and energy applications make the most sense to me as they need powerful remote connections and top-notch reliability.

In the future, Gilat will see a lot of growth from the logistics and autonomous vehicle sectors. The over-the-air update and constant connectivity of Tesla cars will become industry norms. Even more so with self-driving vehicles and delivery robots (as I detailed in my previous report on Deutsche Post).

In addition to spotless connections, same-day delivery logistics will also become increasingly complex. Gilat is prepared to assist. Click here for more information about each application.

Industry & Broadband

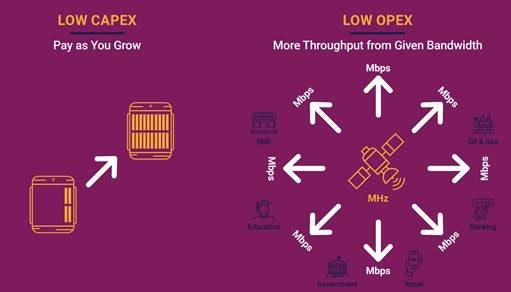

Flexibility is an essential part of Gilat’s offer. There are benefits on both sides.

To start their connection process, the client requires a low initial capital expenditure, but can scale up as they grow.

By spreading the costs between many, many clients, Gilat is able to amortize the massive operational costs and technological complexity.

Therefore, Gilat has multiple business moats, such as economies of scale, lower costs, and the ability to develop more patented technologies at a lower cost per user.

Source: www.gilat.com

As a leader in the field, it has the capacity to provide extra capacity when needed by its clients.

Source: www.gilat.com

The segment includes multiple sub-segments:

l Remote education and E-Learning

l 24-hour news channels (and live broadcast from anywhere)

l Residential broadband (home Internet for isolated places).

I find the last segment to be the most interesting. There are many regions that are too remote for 4G networks to be properly deployed. In these regions, getting a stable home Internet connection is either difficult, expensive, or downright impossible.

Up until recently, satellite broadband was too slow to be anything other than a last resort. Once LEO constellations are in place, this will not be an issue.

New Yorkers will still get their Internet through ground-based solutions. However, people living in low-density areas, such as the Rocky Mountains, the Alps, Northern, Central Canada, Scandinavia and most of Russia, are likely to switch to satellite Internet.

By establishing advanced remote work in scenic and cheaper villages, these areas will become more livable and modern.

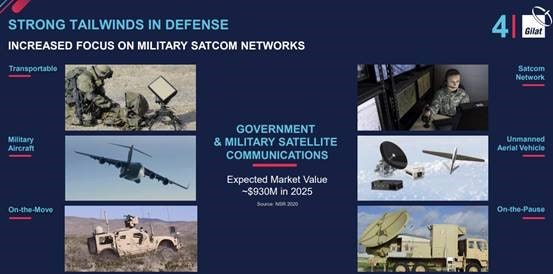

Military

https://www.gilat.com/solutions/defense-and-government/

Last but not least, satellite communication is obviously used by military and government agencies. Historically, this is the first sector to extensively use satellites.

Almost all military operations today rely on satellites, including imagery, telecommunications, and GPS-guided missiles. It surprised me to learn that this is a relatively small market, with less than $1B expected by 2025, compared to $10B in the mobility sector.

Gilat seems to have the advantage here due to its product design, with an advantageous SWaP profile (Size, Weight, and Power). Gilat’s antennas and systems are light, small, and nimble enough to operate in front-line conditions, as well as on UAVs and vehicles.

In addition, the antenna and other electronics are described as “robust, ruggedized, and designed to operate in harsh environments“.

As an Israeli company, I also expect Gilat to have plenty of opportunities to test and demonstrate its products. Furthermore, I imagine it will also benefit from connections with foreign American and European allies.

Government

https://www.gilat.com/solution/public-safety/

Among Gilat’s services is the provision of emergency and disaster response systems for the government. Satellites are ideal for restoring communication lines after earthquakes, hurricanes, floods, and other disasters that destroy land-based systems. In addition to working well for the military, they are also effective for first responders.

Also, the company signed a deal directly with the government to provide Internet access to the population. An example of this is the agreement with Peru. As a result of this deal, Gilat will be able to generate initial revenue for building the network, as well as recurring and steady revenue for operating it.

This business model intrigues me. Per’s government pays upfront the capital expenditures for the system, and Gilat charges $50M/year for its operation. While most subscription-based business models require large initial capital expenditures, Gilat’s government contracts appear to have the capital expense covered by the local authorities.

Management

https://www.gilat.com/about-gilat/management/

As a company like Gilat is so dependent on proper execution and technical ability, I wanted to briefly review the management team.

Adi Sfadia, CEO

Since 2004, he has been involved with telecom and VoIP, mostly as a CFO. Sfadia’s financial background is not a technical profile but should ensure that Gilat’s capital is allocated effectively during its growth.

Ron Levi, COO

It appears that Mr. Levi, who holds diplomas in both computer engineering and management, is the ideal candidate to lead Gilat’s daily operations. His entire career was spent in telecom, including companies acquired by Cisco.

Noam Rosenfield, Senior Vice-President R&D

An Israeli Defense Forces former commander of cyber defense. Additionally, he headed the R&D efforts of Verint, a leading cyber intelligence solutions provider. In addition to handling the very sensitive infrastructure managed by Gilat, he also brings a software angle to the more telecom hardware profile of the rest of the board.

Chapter 3: The Company’s Future

The Key Growth Advantages

Gilat is in a perfect position to participate in the growth of satellite communication. Because LEO constellations are multiplying rapidly, the addressable market will expand much faster than most analysts think.

What was once a growing but also stable industry is now going to be the next big investment topic. In these volatile and profitable times, space is trendy again.

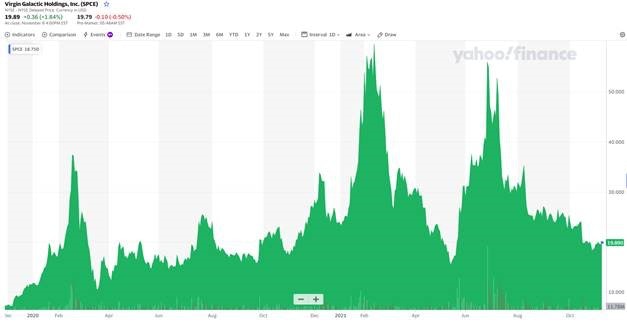

Consider Virgin Galactic, one of the three top private space companies (along with SpaceX and Blue Origin) that recently went public. A company with only a prototype and no income has been on a wild ride, from $7.20 at IPO to a high of $59 today.

With space investing becoming a popular investing trend again, I fully expect the whole sector to gain more attention. After the LEO constellations of Internet satellites are launched, Space Internet will be the next big thing. And Gilat is leading the way in building land-based receivers.

The Moats

In terms of investments, the telecommunications industry is known for being technology-driven and conservative. National telecom companies prefer working with other well-established firms.

Gilat is responsible for 80% of 4G satellite-mobile network connectivity. A company with this pedigree and all the right connections can grab a piece of the space-based 5G pie.

It will also have the ability to spread its R&D and capex costs, giving it a durable price advantage. The company sold 1.6 million satellite terminals in 100 countries.

The combination of a strong reputation, established relationships, economies of scale, and better technologies gives Gilat a powerful moat to remain competitive.

The Techs

As I mentioned previously, I believe it is beyond my capabilities and the scope of this report to dwell on the engineering itself. Gilat, however, has a few unique technologies that set it apart from its competitors:

l The “Elastic Era” connection system; a specialized infrastructure able to handle LEO satellite high-speed orbits in the sky.

l Layer-2 accelerated data. This simplifies the process of integrating satellite connections into mobile networks.

l Fastest airborne modems available on the market

l 5G-ready CBH (Cellular) devices and infrastructure

I won’t pretend to understand it all. There’s no need for me to.

When it comes to overly technical industries, I refrain from second guessing the technology. As an alternative, I can rely on the purchases decisions of people who are way smarter than me, such as engineers at mobile operators or people who handle defense procurement.

I think a product is the right choice if almost all the experts who have worked in the sector for their entire lives choose it.

Financials

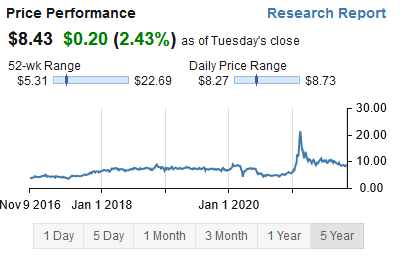

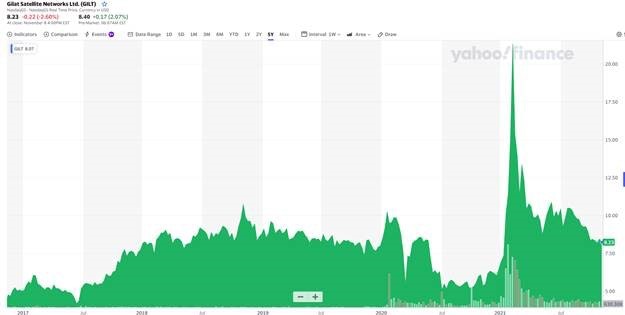

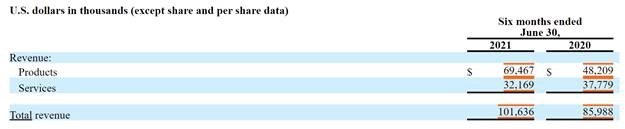

Gilat had a disappointing year in 2020. There was little flying, cruise ships stayed at the docks, oil & gas were in disarray, and many clients delayed investment until they could see the economic outlook more clearly. Revenue declined significantly, especially from product sales.

As a result of this very poor 2020, the stock price fell from +/- $8 to $5. A new line of 5G-ready antennas was announced in February 2021 and the stock rose like a rocket.

Due to the short attention span of today’s markets, the focus has instead been on “disappointing” quarterly results. It seemed that the new product would be sold instantly, rather than being carefully and slowly considered for the next round of investments by Gilat’s clients. Considering the bureaucracy of telecoms, that was not a possibility.

This presents us with an opportunity. The future growth of Gilat was already factored in at $20+ / share. At $8, not so much. Thankfully, the company’s revenues are improving in the first half of 2021.

Because of this, a company is selling cheaply despite excellent growth prospects. For the company as it is now, all metrics and ratios scream cheap. There is also no debt, and the dividend yield is 12%!

I expect Gilat to outperform the market in the long run due to the additional great growth prospects. It might take a little while, however, for revenues to increase as a result of the slow decision-making of its clients and the ongoing deployment of LEO constellations.

- P/E: 10.2

- Price to Sales: 2.6

- Price to Free cash flow: 8.4

- Price to Book: 2.1

- Debt: 0

- Equity per share: $4.05

- Dividend Yield: 12%

- ROIC: 19.4%

Chapter 4: Valuation

Considering Gilat’s financial ratios are more in line with a no-growth company, I expect Gilat to be undervalued. But by how much?

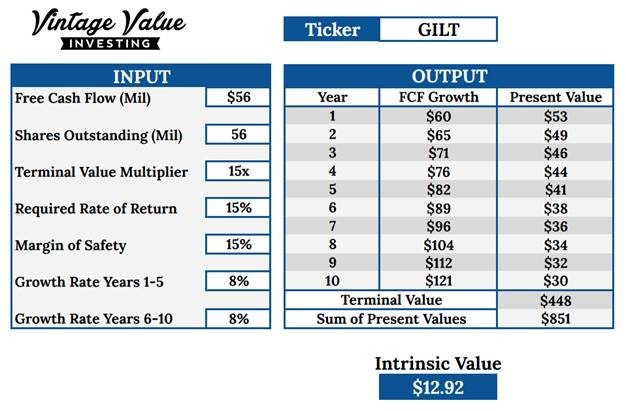

Discounted Cash Flow

Discounted cash flow is the most relevant valuation method for Gilat, as the majority of the company’s value will be in its future free cash flow once the satellite-based 5G Internet revolution begins.

The company has historically traded a price to free cash flow ratio of 10-20, with periodic spikes at much higher levels. The current ratio of 8.3 is very low by comparison.

There is no doubt that space enthusiasm will make a comeback in the near future. This is true each time SpaceX flies a fully civilian crew, Virgin Galactic takes a test flight, or when The Artemis mission brings us back to the Moon. At the very least, this should return the terminal value multiplier of Gilat to its historical norm.

Free cash flow grew by 8% over the last decade, so I will use that, even if that is probably too low, as I ignore the LEO-based Internet growth.

Even with these conservative assumptions, I still get a value for Gilat of almost $13, well above the current $8.23.

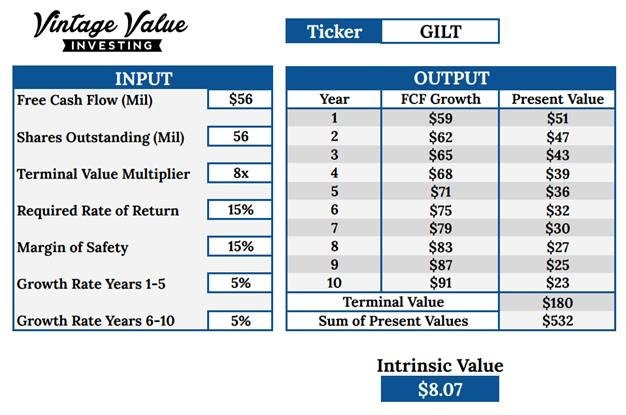

I was also curious to find out what could justify the current price.

We would need the value multiplier to never return to its historical level. Annual growth would need to drop from 8% to 5%. This still leaves a margin of safety of 15%.

The entire report was written under the assumption that satellite communication is about to boom. The valuation (at the moment) is so low that the business growth of Gilat has to slow down in order to justify it!

However, I see a bull case, where growth accelerates beyond the historical trend. An exploding mass consumer market can easily justify the switch from large airlines, oil & gas companies, and the military.

In the event that Gilat only experiences additional growth in five years, this still indicates a substantial undervaluation of the stock: intrinsic value would be more than twice what the stock currently trades for!

Conclusion

My interest in Gilat was sparked by the strong financials on my screener, but I had no clue what Gilat did.

I was intrigued by the satellite communication segment, but I was wary of the competition from SpaceX’s Starlink and similar companies.

I expected a business like ViaSat, which operates GEO satellites. The business model is still profitable, but also declining and in danger of extinction.

The current valuation would have justified the current valuation, making the company a typical value trap.

So I was genuinely surprised when I saw their presentation and found out that the switch to LEO satellites was actually an opportunity for Gilat.

As far as I can tell, the current valuation is more a function of short-term “disappointing” quarters. Covid’s aftermath seems to be holding back the company’s short-term results. In the long run, the company is still well positioned.

The current core business will continue to grow. Mobility continues to grow rapidly. The need for mobile connections has never been greater. Industry IoT is going to become a standard in many more industries. Sat-comm spending in the military is not going away.

Add to this very solid foundation the emerging but soon to be large and well-established residential satellite Internet.

At the current valuation, the businesses should provide a comfortable 15% annual return. However, if I am right, Gilat in the residential internet market is perfectly positioned to grab a leading position and expand its market share.

Growth in the core operation, expanding markets, a growing moat, and a sector poised to become a darling for investors, all at a discount. What’s not to like about Gilat?

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in GILT and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.