India has just become the most populous country on Earth. And with strong demographic growth, unlike China, India looks set to keep that title for at least a few decades.

This could, in the future, make it one of the largest economies in the world, or maybe even the largest. It is currently poor on a per capita basis. So there are plenty of challenges in India, but also huge growth potential.

Could India replicate China’s success and become a major economic power? And how can investors look to benefit from such a scenario?

India Overview

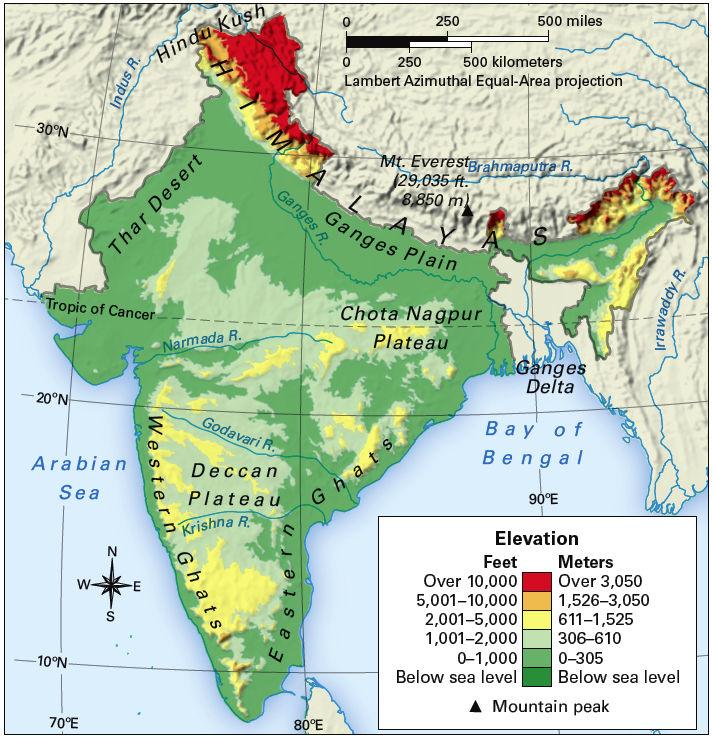

By most metrics, India is a giant. It has 1.4 billion people, is ranked as the 5th largest economy in the world, and has a territory of 3.2 million square kilometers, or a full 2% of the world’s landmass, making it the 7th largest country.

It is bordered to its North by the Himalayan mountains, from which the all-important Ganges river flows, feeding a massive fertile plain. The south is dominated by hills and low mountains. The country is bordered to the North by China, Bhutan, and Nepal, to the West by arch-rival Pakistan, and to the East by Bangladesh and Myanmar.

India is a democracy, and a complex patchwork of ethnicity, religion, languages, cultures, and social orders. This makes it a very hard country for foreigners to understand and analyze. This extreme diversity is both a source of strength and weakness and is reflected in the federal nature of the country.

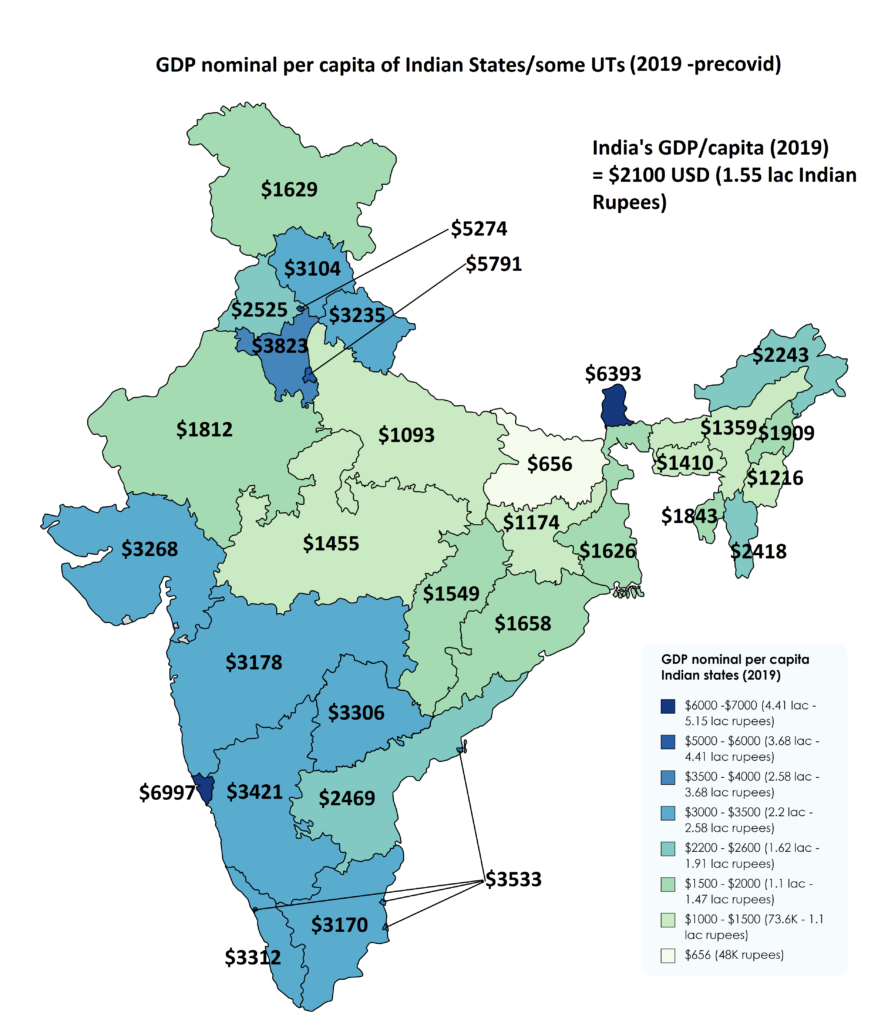

The level of development, culture, and lifestyle can vary significantly inside the country and between different states. As a rule of thumb, the Northern states are poorer than the Southern ones, with the exception of the states surrounding Dehli, the region containing the capital New Dehli. The richest state is on the Western coast, Goa, a former Portuguese colony.

Relations with its neighbors rank from poor (China) to very poor (Pakistan) to moderately okay (Bangladesh, Myanmar). Due to these overall poor relations, India is mostly looking overseas for partners and allies, notably in the West.

The position as the “world’s largest democracy” and a key partner in Asia against China, as part of the “Quad“ (Australia, USA, Japan, India), is a key component of India’s geopolitical alignment. It is nevertheless part of multiple China-oriented organizations, including the SCO (Shanghai Cooperation Organization) and the BRICS (Brazil, Russia, India, China, and South Africa).

India’s economy is dominated by the service sector (55.6% of GDP), followed by the industrial sector (26.3%) and the agricultural sector (18.1%). Some of the leading industries are telecommunications, automotive, and pharmaceuticals. Some of the leading services are software, customer management, and financial/fintech.

The economy is still growing very quickly, with a “slow” year being a forecasted 4.8% growth in 2024, compared to 7% in 2022. The country is somewhat dependent on imports for energy and also relies heavily on domestic coal production for generating electricity.

The Indian model of development has been to “leapfrog” directly toward a service economy, without first building heavy industries, with mixed results. While this created plenty of jobs and allowed growth, it created success in the IT industry; it also left the country with poor infrastructure, like clogged roads, outdated railroad systems, an unstable electric grid, and poor sanitation. A new emerging model is to focus on growing the economy while also boosting infrastructure investments.

Another hindrance to growth is a notoriously massive and all-encompassing bureaucracy. In the words of President Obama:

Despite its genuine economic progress, though, India remained a chaotic and impoverished place: largely divided by religion and caste, captive to the whims of corrupt local officials and power brokers, hamstrung by a parochial bureaucracy that was resistant to change.

India’s Strengths

With China now a world power able to directly rival the USA, India gets a lot of attention as the “next China”. The comparison makes sense as India has many features in common with China a few decades ago:

- A massive and growing population: The average Indian is just 28 years old. The large population provides a deep labor pool and a large internal market.

- A good level of education: India is ranked 32 in the education ranking, putting it at the level of Poland (26), Portugal (25), and Brazil (36). Combined with the population size, this provides an enormous pool of skilled professionals whose talents are largely underused, leading to large-scale outmigration. India has the largest ever adolescent and youth population and the third-largest group of scientists and technicians in the world.

- A solid saving rate at 31% of Gross National Income, above Germany’s (27%) and below China’s (45%), providing capital for economic development.

- Upcoming plans for infrastructure: aware of the problem, the government is planning a massive infrastructure build-up through the “National Industrial Corridor Program“. This should boost public spending and the overall efficiency of the economy.

India’s Weaknesses

The main weaknesses and threats to India’s economy are not so much economic as political and social.

- Internal divisions:

- Religious tensions between the Hindu majority and Muslims, Christian, and Sikh minorities, led to frequent clashes, riots, forced conversion, and repressions.

- Social divisions: urban vs. rural, men vs. women, poor inter-caste relations, the rivalry between states, there is no shortage of fracture lines in Indian society.

- Geopolitical rivalries: India is frequently clashing with its neighbors. Since the 1947 partition of India, the country has been at war with Pakistan 4 times, most recently in 1999, with ongoing tensions over the status of the Kashmir region. The China-India border is another flash point, with a clash between the two’s armies as recently as December 2022. Both Pakistan and China are nuclear powers.

- Inefficient state and bureaucracy: even if democratic, the Indian state is relatively corrupt (ranked 85th on 180). This hinders entrepreneurship, initiative, and infrastructure building.

Middle-Income Trap

For many emerging economies, the danger of the middle-income trap is a serious one. This is where an economy develops up to a point, but then hits the ceiling and is unable to go up in the value chain.

“a country in the middle-income trap has lost its competitive edge in the export of manufactured goods due to rising wages, but is unable to keep up with more developed economies in the high-value-added market.“

To some extent, India could look affected on a surface level. At the same time, its performance in high-value sectors like IT does not fit well with the middle-income trap thesis, as such Indian exports are competitive. Base commodities export is not a key part of the economy.

So solving corruption and internal tensions, and reducing bureaucracy should boost growth as the pre-existing base of high-performing specialists and industry is already in place.

Timing the Market?

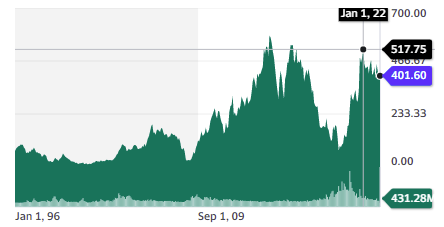

The Nifty50, an index gathering the 50 largest companies in India, has recently hit an all-time high in early 2022 at 18,400, or a 6.5x performance since 2009. So there might be an argument that some of India’s potential performance is already priced in.

In 2021, at lower stock market levels, the Reserve Bank of India was warning of a potential bubble. So while the long-term trajectory of India seems to be one of growth and development, some caution is advised in terms of market timing.

Company Spotlights

At this stage of growth, it is unclear which company could be the future Indian Alibaba, Huawei, or TSMC. So instead of making uncertain bets on technology and Indian development, large companies that will grow with the economy are probably a safer bet until more national champions emerge.

Reliance Industry (RIGD.IL)

The company is India’s largest conglomerate and one of the country’s most profitable companies, employing around 30,000 people. It is mostly active in telecommunication (mobile network & broadband) and energy & petrochemicals (especially refineries), but also retail.

India is still underequipped in cars and digital appliances, and economic development is likely to benefit Reliance. Internet penetration is just 47%, leaving 742 million with no use of the Internet in 2022. An extra 250 million new smartphone users are expected by 2026.

With a P/E of 23.6, Reliance does not seem cheap, but not overpriced either.

Its ownership of licenses for mobile and land-based Internet is likely going to prove quite valuable on the last spur of Internet utilization growth in India. This is one case where a slow liberalization bureaucracy could play in favor of investors.

Tata Group (TATAMOTORS.NS)

Another extremely large Indian conglomerate, Tata is not open to direct investment at the group level. Several subsidiaries are trading separately, in fact, a total of 29 different listings. Some of the most notable are described below.

Tata Motors

The owner of the brand Daewoo, Jaguar, and Land Rover, as well as joint ventures with Stellantis and Hitachi (for heavy construction equipment). The company produces around 1.1 million vehicles per year.

The company has historically struggled to be profitable and had a few low-cost car projects failing in the past, like the Tata Nano.

It is also active in the defense sector, a segment that might benefit from a push to localize weapons supply and reduce dependency on Russian suppliers, and with India the second largest army by personnel number, just before the USA and below China.

Tata Steel (TATASTEEL.NS)

The company operates in 26 countries, with a focus on India and Europe. It produces 30 million tons of steel yearly. It intends to double its Indian production by 2030 and reach a total production of 40 million tons of steel by the same date. It also plans to double its iron mining capacity from 30 mtpa (million tons per year) to 60-65 mtpa.

Some of its business in Europe is suffering from elevated energy prices, but that might be compensated by India sourcing cheap energy from Russia.

The current P/E at 4.47 is carried by rising steel prices. The cyclicality of the industry is something potential investors have to consider.

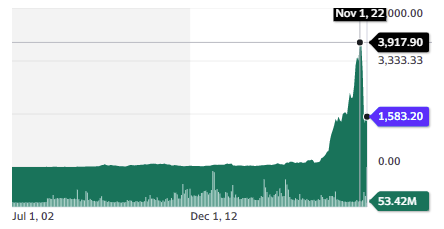

Adani Group (ADANIENT.NS)

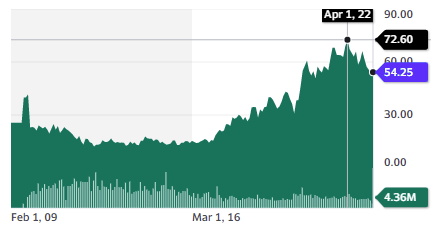

This company is worth mentioning as it is at the center of maybe the largest-ever controversy in the Indian investing landscape, which you will not fail to hear about if looking into investing in India. Its stock chart was definitely an … interesting one, from a low of INR141 in April 2020 to a high of 3,917 in November 2022, followed by a precipitous fall.

The crash was induced by a report from Hindenburg research, accusing Adani, the man behind the eponymous group, of “the largest con in corporate history“.

I will leave it to readers to judge the veracity of these accusations and if the price fall is enough to justify the obvious risks attached to this stock. The current P/E ratio is still 90.

ETFs

If you want to invest in India as a whole, an ETF might be a better option.

First Trust India NIFTY 50 Equal Weight ETF

A common way is just to target the largest companies, similar to the S&P500 in the US. In India, it is the aforementioned NIFTY 50. For this, the First Trust ETF, with equal weight for each member of the Nifty 50, can be a good option.

Columbia India Consumer ETF

This is an ETF with equal weight on consumer companies in India. This makes it a bet on the rising purchasing power of Indian consumers. It is roughly equally split between discretionary items and consumer staples.

iShares MSCI India Small-Cap ETF

While it might be too risky to stock pick along smaller Indian companies, an ETF can spread this risk over the whole market. This iShares ETF is focused on Indian small caps, with a focus on industrials, financial services, basic materials, and healthcare.

India Internet & Ecommerce ETF

Because most of India’s international competitiveness in India comes from the IT sector, this can be a center of interest for overseas investors. The largest holding of this ETF is Reliance (7.71%), followed by other IT companies and logistics, including railroads.

If India is to persist in relying mostly on this sector to fuel its growth, this is the ETF the most likely to capture these gains. So investing in it will depend mostly if you judge India’s plans for rebalancing toward more industries, infrastructures, and “made in India” realistic.

Conclusion

India is a country with a lot of promise. It has also acquired a bit of a laggard reputation among its peers like China, Indonesia, and Vietnam. The persistence of corruption, bureaucracy, and a divided society are the major reasons for this relative underperformance.

Some level of geopolitical risk should also be included, even if, for now, India has craftily managed to strike a balance between the nascent Western and Eurasian blocs.

Nevertheless, from an investing standpoint, India has developed a lot, just not as quickly as China, the quickest development story in the entire history of the world. And contrary to more mature emerging markets, it still has tremendous space to grow before turning “emerged”. Its unique development pattern should also protect it from the middle-income trap.

Investing targets are mostly large conglomerates for now, partially due to such corporations being more able to navigate the country’s economic system. In the longer run, investors in India will want to diversify and capture early future national champions in technology, utilities, energy, consumer goods, localized e-commerce, etc…

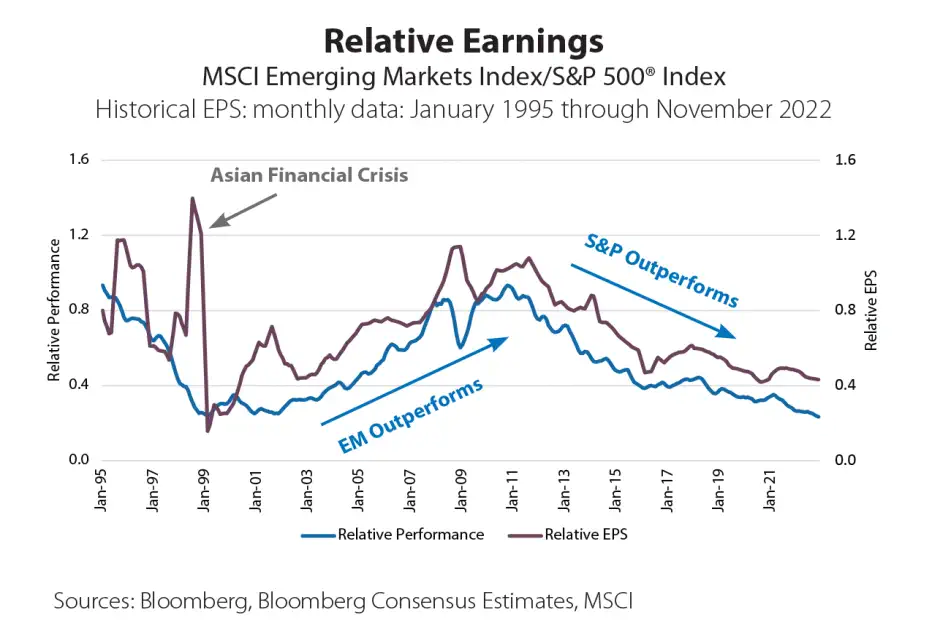

Finding Value in Emerging Markets

Stock Spotlight has regularly covered stocks in emerging markets, which can offer great companies at discounted prices. After a decade of outperformance for the US stock market, it might be time for emerging markets to shine. This cycle between emerging market (EM) vs the US tends to be roughly 10-15y long, as you can see below. With the S&P500 outperformance started in 2010, we are due for a reversal in trend.

Source: Western Southern

Past patterns may not be repeated, but the investing world still extends beyond the US, and increasing numbers of investors are considering exposure in non-US markets!

Emerging Value

This is a series focused on opportunities in emerging markets. The goal is not to discuss breaking news. Instead, we will focus on long-term trends and lasting phenomena that will impact investing in a country or region. It will also look at a selection of companies that might be worth a deeper analysis.