Overview: We surveyed over 600 Americans to learn about their perceptions of financial advice and its worth. What we found is that when it comes to financial advice, consumers aren’t clear on what is going on, what they are receiving, and what its value is.

Are financial advisors worth it? Many consumers aren’t sure, often because they aren’t sure what financial advisors do. Financial advice is a fragmented industry, only halfway to being an established profession.

Consumers have traditionally associated financial advice with high-end investment advisors and financial planners that serve affluent clients. Most users don’t recognize that credit counselors, housing counselors, financial therapists, and other professionals who work with financially stressed clients are also financial advisors.

The definition and role of financial advisors are changing and evolving. We conducted this survey to understand if consumer attitudes toward financial advisors are also changing, and what this means for the future of financial advice.

Key Findings

Most clients (75%) recognize that the potential of financial advice goes beyond delivering investment returns and into the realm of goals fulfillment. Learn more

Most respondents (78%) believe that only some advisors are worth the fees they charge. This implies that pricing pressure is not too far away for others! Learn more

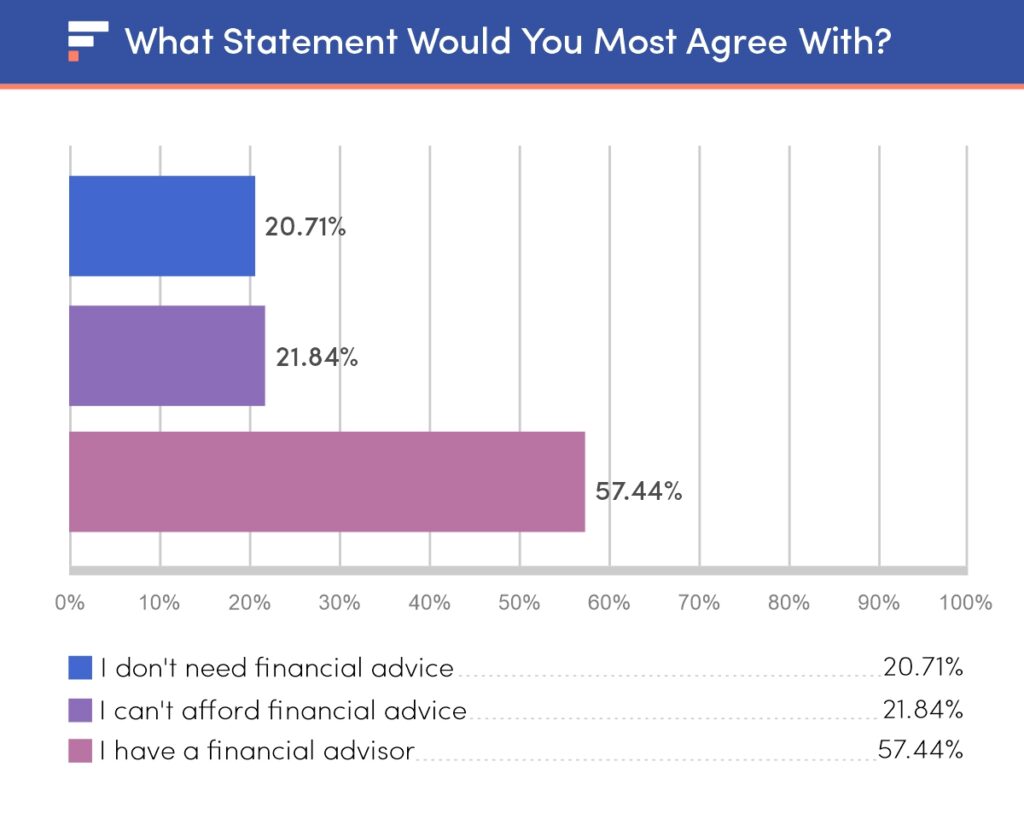

57% of respondents believe they have a financial advisor (although the term covers many different types of advice). Of the remainder, many appear to lack sufficient assets to qualify for advice under the prevailing asset-based fee model. Learn more

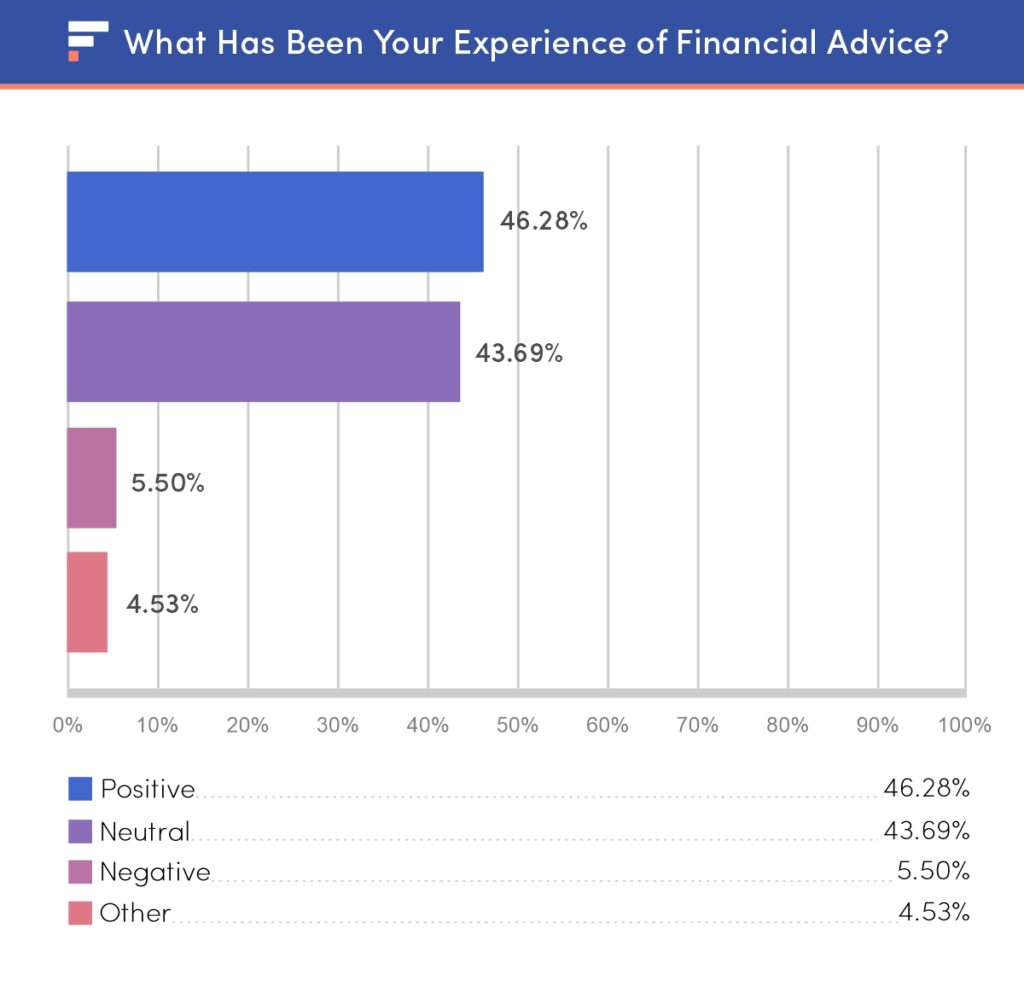

While only 5% of respondents reported that their experience of financial advice had been ‘Negative’ (which is encouraging) and nearly half (48%) selected ‘Positive’, a surprisingly large group (42%) opted for ‘Neutral’ (which is less encouraging). Learn more

Only 11% of definitions indicated an explicitly skeptical or jaded attitude to the value of financial advice. The remainder emphasizes the role of the financial advisor as a ‘navigator’ in an increasingly complex world. Learn more

Consumers aren’t clear about what financial advice is, because financial advice is a fragmented industry, only halfway to being an established profession.

Introduction

Financial advisors are not like other professionals. With a lawyer, accountant, or a doctor, you have a sense that they have been through a common set of hurdles (medical school, the bar exam) and you can trust them to maintain certain standards.

A lawyer, for example, can be expected not to break client privilege, just as the doctor can be trusted not to prescribe inappropriate medication. If they do either of these things, they run the risk of being disbarred or struck from the register, after which they will no longer hold professional status.

A profession is different from an industry. In an industry, the aim of the provider is to sell you as much of a given product or service as possible. A double-glazing salesman doesn’t have a fiduciary duty to ensure you get the best double glazing at the lowest price – that’s your job as a consumer. As the lawyers might put it, the principle of ‘caveat emptor’ (buyer beware) applies.

Financial advice is – currently – somewhere in between profession and industry. Advisors don’t have the same professional standing that a doctor or surgeon might have, but at the same time, they enjoy more prestige than the car salesman or estate agent.

A big part of the problem is that people don’t have a clear view of what financial advice is. And this is no wonder, for three reasons:

- The financial advisor community is highly fragmented. Since there is no single route to professional status, anyone can claim the role of ‘wealth advisor’, even if they have no qualifications at all. Consequently, the community contains the whole gamut – from actual salesmen pushing financial products to genuine experts who integrate knowledge from multiple domains to solve complex financial problems.

- There aren’t a lot of movies or TV shows about financial advisors. This may sound like a minor point, until you consider how many legal and medical dramas have been produced. By contrast, there is no clear view of a financial advisor in the public consciousness. Financial advice is, sadly, not particularly dramatic, and so Hollywood tends to focus on Wall Street capers and corporate high-jinks, rather than tax-loss harvesting for Mr. and Mrs. Jones.

- Financial advice has evolved considerably in recent decades. For our grandparents, “financial advice” consisted of a broker helping you to buy and sell individual stocks and bonds. Today, market timing and investment selection is only part of investment management, which is itself only a part of the broader field of wealth management as practiced by its more advanced practitioners today. It covers many related fields, some of which overlap with law (estate planning) and accounting (tax strategy). It is more akin to problem-solving than market-trading, and requires a completely different skillset

The fragmented and undefined market for financial advice is a big problem for consumers and genuine financial advisors. The lack of clarity around financial advice allows a lot of genuinely bad actors to continue to operate under its cover, typically at the expense of unwitting clients who lose money on dubious financial products, and honest advisors whose reputation suffers from the taint of association.

This may be changing. One of the benefits of the internet age is the transparency it has brought to many industries that previously depended on or traded upon secrecy.

The financial crisis of 2008 opened many eyes to the borderline (and actual) fraud that is routinely perpetrated by the institutions who are charged with our financial wellbeing. A better informed and more demanding consumer could be just what the financial advice industry/profession needs to encourage it to raise its game.

The Results

The survey was conducted in October 2021 and consists of responses from around 620 participants from across the USA. The respondents were all from households earning above $100k in annual income. We asked the respondents to answer the following questions:

- What Is the Point of Having a Financial Advisor?

- Are Financial Advisors Worth Their Fees?

- Do You Have a Financial Advisor? Do You Need One?

- What Has Been Your Experience of Financial Advice?

- How Would You Define the Value of a Financial Advisor in One Sentence?

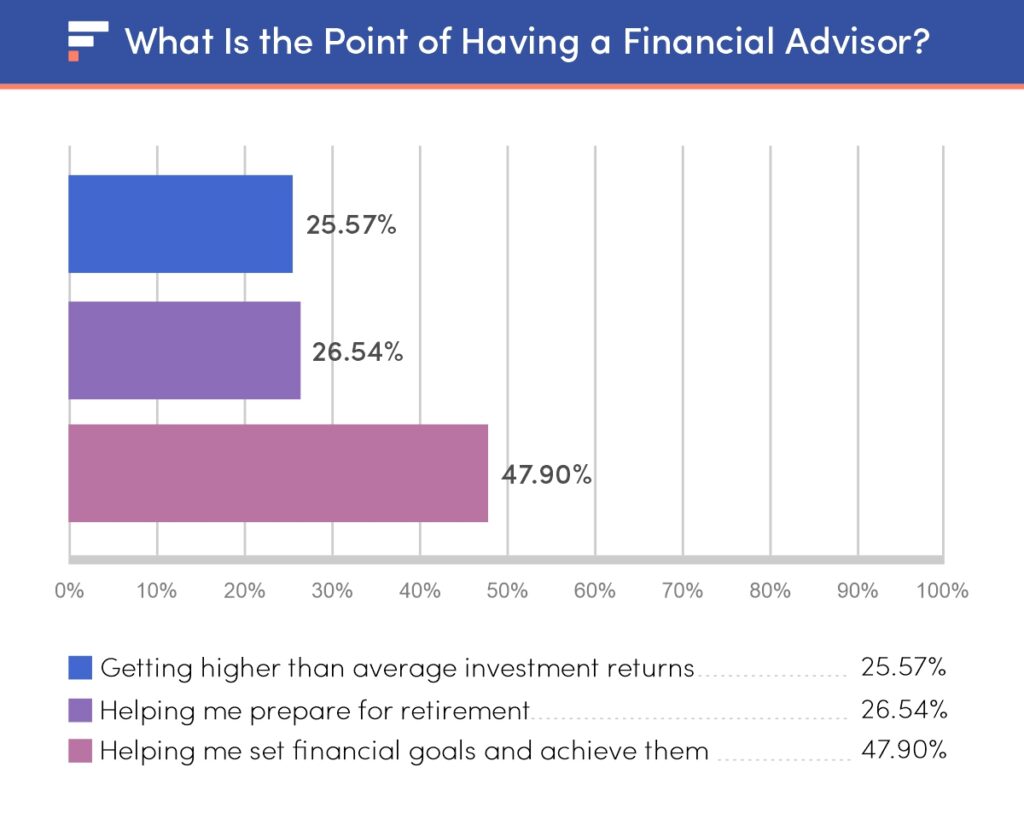

What Is the Point of Having a Financial Advisor?

Not so long ago financial advice was limited to advising investors on what stock to buy or when to make a trade. There are still advisors who focus on security selection and market timing as their main source of added value, but they are better termed ‘asset managers’ in that their goal is simply to maximize risk-adjusted returns.

Even if it is achievable, simply targeting higher returns is a narrow set of objectives and does not take into account the point of investing, which is not ‘to become richer’ but to provide a means of achieving one’s goals.

The baseline goal for most people is ensuring that they accumulate assets to remain self-sufficient after retirement. With the rise of the baby boomer generation, the financial advice industry has developed a suite of products and services to help meet this need. For the advisor, retirees are attractive clients because they are typically in a position of substantial wealth, having saved consistently over the course of a lifetime.

However, ‘retirement management’ is only marginally broader than ‘asset management’ as a definition of financial advice, since it restricts advice to those aged 55 and over (with sufficient wealth to invest). Since everyone has financial needs, financial advice should ideally address people at all life stages, and encompass many questions besides retirement.

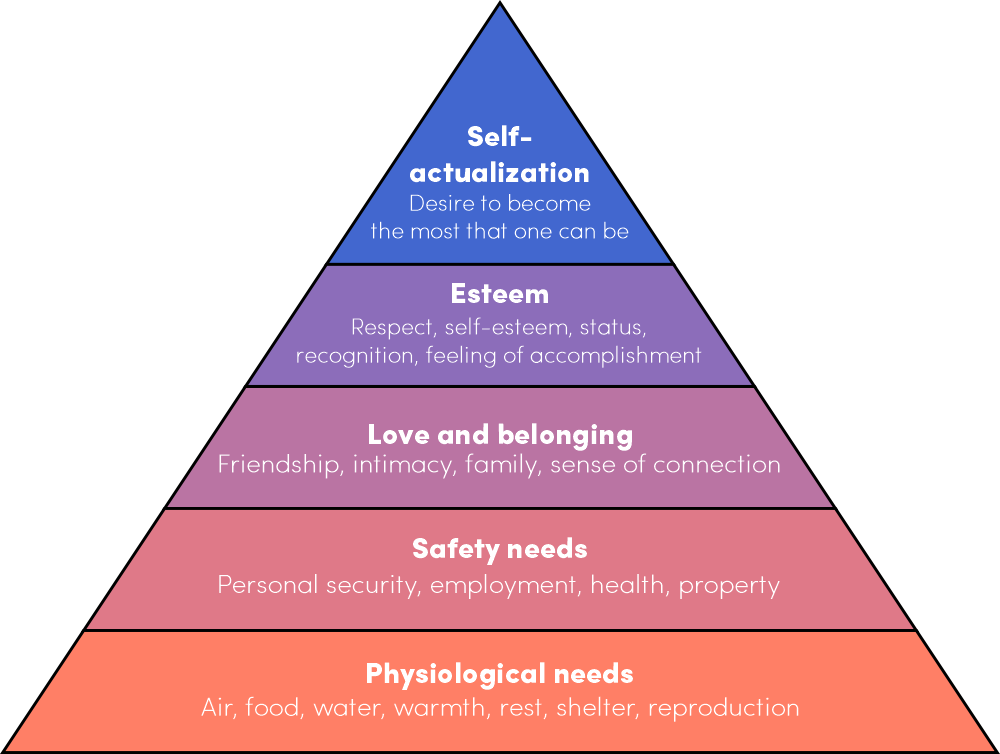

The popular framework developed by Maslow sets out a hierarchy of needs, beginning with fulfilling bare necessities (such as food and shelter) and progressing upwards to needs more related to fulfillment and self-actualization (e.g. achieving one’s potential) than mere survival.

The evolved advisor (also known as a comprehensive financial planner) helps a client on every level of the Maslow hierarchy and will begin the relationship by understanding his or her aspirations and goals relating to career, family, and legacy.

Home-buying, credit and debt management, and college savings plans are all important financial topics that warrant advice and are typically most pertinent for a client in their early or mid-career. A truly holistic advisor, therefore, serves clients of every age and supports them at every stage.

If we examine the survey results, we see – encouragingly – that a majority of clients see financial advice as more than simply ‘getting higher returns’. The largest response group (49%) believes that the value of advice is more related to setting and achieving goals, moving the value of the service further towards the higher end of the Maslow pyramid.

Later in Question 5 (“How would you define the value of a financial advisor in one sentence?”) those who answered ‘Getting higher than average returns’ in this question tended to define the value of financial advice in terms of the portfolio, the market, and outperformance.

Those who answered ‘Helping me set and achieve financial goals’ on the other hand, were more likely to mention other concerns such as plans for their children, tax implications of financial decisions, and support with their business.

The overall conclusion is that people are aware that advisors can, or at least should, be broader in their scope of services than simply delivering excess returns (or as mere ‘conduits’ as one skeptical respondent put it, presumably referring to the practice of pushing financial products).

As consumers become more assertive in this regard, it is to be hoped that the population of financial advisors will begin to resemble this updated set of expectations.

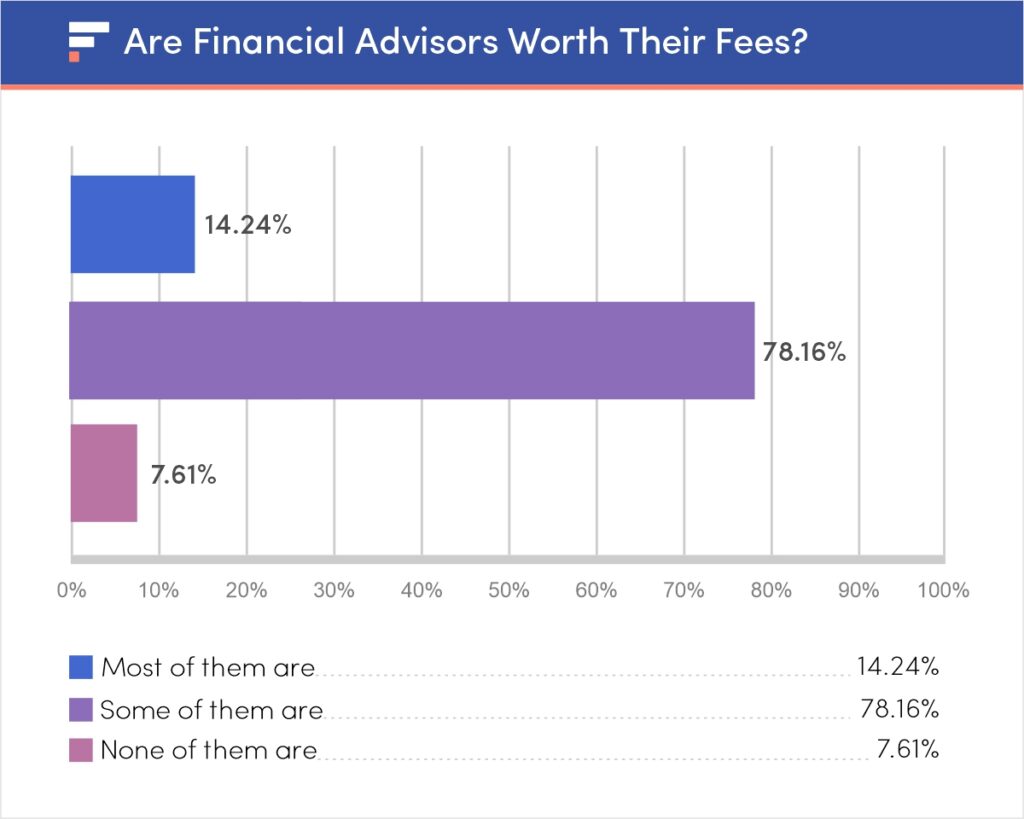

Are Financial Advisors Worth Their Fees?

Because the value of a financial advisor is such a confusing topic, it is only natural that the question of value in relation to fees is similarly fraught.

There’s a growing debate over how advisors should charge consumers for advice. In some cases, this is due to regulation (MiFID in Europe, Reg BI in the US). There is also an ongoing internal debate within the advice community as to which is the best fee model (typically, it must be said, conducted in terms of what is best for the advisor!).

Consumers are notably absent from the debate. To use the words of one executive, financial advice is ‘sold not bought’ – that is to say, people are expected not to understand the product or the fee structure, and take whatever they are given (or whatever the regulator allows).

This is likely to change in the future due to the heightened transparency of the digital age. People have access to lower-cost investment options (e.g. through Robo-advisors). While these are unlikely to replace human financial advisors as initially feared, it is nonetheless placing pressure on fees.

Why? Because even if the value of financial advice has expanded from just investments to a broader range of financial topics, the fee model remains tied to the value of the portfolio in most cases, thanks to the growing dominance of the AUM fee model (charging an annual percentage fee based on the assets under management).

Advisors don’t want to move away from the AUM fee model because it is very profitable and has up to now worked well for them. If clients start to challenge the fee level, this could make the model highly unprofitable. Owing to fixed costs, a mere 30% reduction in fees can translate to a 100% decrease in profits.

What did the data show?

Advisors can take comfort from the fact that over 90% of respondents acknowledged that at least some advisors are worth their fees. This means that advisors who can demonstrate value for money are safe from fee pressure for the time being.

Viewed from another perspective though, around 85% of respondents did not agree with the statement that most financial advisors are worth the money. This could imply they believe the true proportion of ‘good’ financial advisors is fewer than half!

That’s less of an endorsement. While professional advisors may be shielded, fee pressure is very much on the cards for the financial advice ‘industry’.

Do You Have a Financial Advisor? Do You Need One?

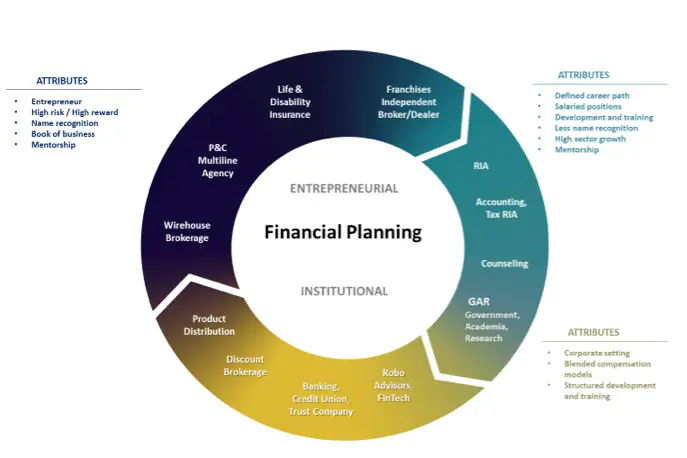

As we covered in the introduction, because there is no single recognized route to professional status, individuals of various backgrounds are able to hold themselves out as financial advisors. This makes it hard for consumers to distinguish the highly qualified from those less so.

Normally, one would use official designations (e.g CPA, MD) to determine the quality of a professional. There are so many qualifications (and of such varying quality) in the field of financial advice that the result is a confusing alphabet soup of acronyms, which in all likelihood only serves to confuse rather than inform potential clients.

In the case of the US, the reason for the confusion is historical. Professor Nathan Harness of Texas A&M has used the metaphor of different ‘tribes’ to explain the fragmentation of financial advice.

He traces each of the modern-day “tribes” back to their origin. One advisor might originate from a background in product distribution, where the aim is to maximize one’s close rate. Another might come from the world of accounting and CPAs, where the fiduciary culture is dominant.

From a client’s perspective, however, it may appear as though both individuals are performing the same function, particularly if they are using the same language. A financial plan prepared by an insurance salesperson, however, is more likely to be a vehicle to sell insurance.

The service that is provided by a financial advisor with roots in the world of accounting is more likely to be the kind of advice that most respondents to this survey say they want, wherein the advisor optimizes for the client’s long-term best interests.

All of this makes the results of the survey question somewhat difficult to interpret.

While the majority of respondents (57%) believe they have a financial advisor, it is difficult to know which tribe the advisor comes from or what type of advice is being delivered. From our perspective, the proportion of those receiving true financial advice (in the comprehensive sense) is likely to be far lower than 57%.

The fact that 20% of participants don’t believe they need a financial advisor gives a clearer message. By examining how they answered Question 5 (“How would you define the value of financial advice in a single sentence?”), we can examine the rationale behind their responses.

Interestingly, only some of these responses were from true “skeptics” who believe that financial advice is a waste of time. Rather, this group consisted mainly of respondents who believed they were able to handle matters for themselves (more about this later). In other words, advice is a valuable service for those who need it.

The group that said they ‘can’t afford a financial advisor’ is also significant.

As advisors have moved to an AUM-based pricing approach, it has become necessary to restrict access to those who have sufficient assets to manage (typically 500k or above), otherwise the fees are too low to pay for the service.

This cut-off point eliminates a large portion of the population below retirement age (who either lack the assets or do not have them available to hand over to be managed), including those who might otherwise have been happy to pay by other means (e.g. % of salary, by the hour).

One of the hallmarks of a true profession is that it is open to all – law, medicine, and accounting are services that the entire population has access to. Removing this unnecessary barrier will be key to unlocking the true potential of financial advice to create wealthy individuals rather than serve the already wealthy.

In the future, this chart may look very different, with the overwhelming majority of respondents sitting in column 3 (“I have a financial advisor”). There may also be a common consensus on what a ‘financial advisor’ is and does.

What Has Been Your Experience of Financial Advice?

Encouragingly for financial advisors, the number of ‘negative’ experiences is tiny (around 5%) versus the 47% who said their experiences had been positive.

However, 42% rated their experience as neutral, which is a very large percentage for a response that is essentially non-committal. After all, how many important things are consumers generally ‘neutral’ about?

This brings us back to the common theme in this report: when it comes to financial advice, consumers aren’t clear on what is going on, what they are receiving, and what its value is.

Digging deeper, we can look at how each group responded in Question 5 (“How would you define the value of financial advice in a single sentence?”).

Positive respondents, as might be expected, gave definitions that focused on guidance, goals, and value-added services such as tax advice. A significant minority focused on investment returns, implying that there is still a good market for advisors who lead with this as their main proposition.

Negative respondents tended to question the entire value of the financial advice offering (e.g. “A waste of time and money!”), and some comments (e.g. “Glorified salesperson”) implied that the respondent had encountered a product-salesperson who had not put the client’s interest first. While apparently rare, these negative experiences clearly engender a hostile attitude to the concept of advice in general.

Neutral respondents are the most interesting category. The skeptical comments in this category were more nuanced than in the ‘Negative’ contingent, with concerns mainly centered around uncertainty (“I do not understand how they make money”) and evoking a general sense of wariness rather than absolute disbelief. Many respondents gave clear and concise definitions of what financial advice could and should be. The problem appeared to be they had not experienced it themselves.

As remarked above, the sheer size of the neutral category is the main takeaway – and puzzle – in this question. We would argue that this indicates confusion more than anything else, leading to caution. The danger is that a lack of passionate devotees suggests vulnerability to alternative solutions that may present themselves.

How Would You Define the Value of a Financial Advisor in One Sentence?

Given that most financial advisors would struggle to answer this (trillion-dollar) question concisely and accurately, we were impressed with the range of the responses we received! Viewed in composite, it was possible to derive a fairly detailed view of the perception of financial advice in the mind of the everyday consumer.

Certain themes emerged, which we have set out below.

Investment Management Is Still a Draw for Some (For Now)

A sizable portion of the participants (17%) responded to the question purely in terms of investment results. For this group, the attraction of an advisor rests on the ability to generate higher returns than they would be able to do on their own. In the words of one respondent, “If they produce, they’re okay.”

As stated above, the idea of advice as primarily about generating high returns is becoming outdated (not least because it is statistically highly unlikely that your advisor will be able to beat the majority of other investors). But for many, the story of the market-beating advisor remains potent.

In this area, respondents seem to value advisors in three ways.

- The first is knowledge – advisors are perceived to have genuine expertise in managing money (to quote one respondent, “Navigates a complicated investment landscape that I myself do not understand”).

- Linked to this is the idea that advisors have access to ‘deals and resources’ not available to the everyday consumer, much like a mortgage broker or (in the pre-internet days) travel agent.

- Also very common was the idea that consumers could perform investing by themselves if only they had the time. In the words of one respondent, “I don’t have the time or the desire to watch the market or understand products and their implications.” The idea is that an advisor is an outsource partner who takes care of an aspect of your life on your behalf.

It remains to be seen how sustainable the investment-led proposition will be, but technology and increasingly self-reliant customer attitudes may mean that few advisors can continue to pose as stock-market gurus. For now, as we have said, this market niche appears solid.

A Broader View of Advice

Only 5% of respondents referred to retirement directly, with most people referencing broader aims. While the statements these respondents made were naturally very high-level, many were excellent descriptions of the value of a comprehensive advisor, and could even be used as marketing taglines by advice firms. For example:

- “Professional guidance on difficult decisions”

- “Helping me navigate my financial life”

- “Puts my mind at ease about my financial future”

- “Gives you confidence you are making good decisions with your money.”

- “Making sense out of mayhem.”

One respondent even raised the point that advisors potentially fulfill a gap in our current education system. “Since schools do not teach financial literacy, someone has to.” Other common ideas used to describe the value of an advisor include:

- Keeping me on track

- Keeping me from doing something stupid

- Making better financial decisions

Although ‘peace of mind’ is a cliche when talking about the benefits of financial advice, many respondents referred to the advisor as a person who “removes the worry” regarding their future. This includes in particular stressful life events such as bereavement (“Reassuring that someone will help my spouse if I die”.)

Navigating an Increasingly Complex World

There was a definite indication from various responses that the need for financial advice is actually increasing in today’s world, as a result of the accelerating pace of change and growing complexity of life.

This could be due to Covid, cryptocurrencies, geopolitical shifts – but the point is that for the average consumer, the world they face is not the one in which they grew up, and a trusted advisor is more important than ever.

This means that people who did not consider a financial advisor necessary before may now be changing their minds on the subject. This is even winning over former-skeptics, as we see from the comment, “A fiduciary is necessary with our government and financial institutions as unstable as they are now. As much as I dislike it, they have become necessary now for support.”

Finding the Right Advisor Can Be a Lottery

There is a paradox at the heart of the feedback. In spite of negative comments from some (more on this in the next section), it was noticeable how warmly many other respondents spoke about the good advice that they had received in the past.

As already observed, attitudes to financial advice are – by and large – more positive than negative.

The problem is that this positive attitude is undermined by the coexistence of good and bad actors in the advice category, and the difficulty of distinguishing between them as a potential client.

Two representative comments are “An honest advisor is worth their weight in gold,” or “If they’re honest and good at their job, then they’re worth working with.” These statements are endorsements of good advisors, but the fact that the writer feels the need to explicitly call out the word ‘honest’ implies that this should not be the default expectation.

Reasons for Skepticism: More About Advisors Than Advice

Only 11% of definitions indicated an explicitly skeptical or jaded attitude to the value of financial advice. These 60 responses ranged from outright cynicism (“Most advisers give the same advice to each client.”) to caution (“[The value] depends entirely on the advisor”) and grudging acceptance (“A necessary evil.”)

Believing that a service has no value and mistrusting those who provide it are two different things. Even among the skeptics, those who believe that advice is fundamentally worthless were in the minority. The questionable point for most appears to be the integrity of advisors themselves.

As one respondent put it, “He/she should be looking out for me the investor, not ways for them to make more money through me with no regard to my investment return.” Fixing the reputation of advisors by instilling a true fiduciary approach (as opposed to a sales culture) will go a long way to winning over the skeptics.

Dissatisfaction With the Fee Model

Another strain of frustration came from a sense that financial advisors are only interested in those who are already wealthy, rather than helping people become wealthy. As one respondent wryly observed, “[Financial advisors] are for people who don’t need financial advisors.”

This is connected to the point around the fee model. There is something perverse about requiring a high asset minimum in order to accept a client, like a doctor with a minimum health requirement, or a lawyer who only takes easy cases. The fact that clients are sensing this should be a warning sign.

Another telling quotation came from a respondent who is not only receiving advice but is pro-advice, not a skeptic. “Though I might be paying more than I’m getting out of it, if I didn’t have a planner I’d be more worried about retirement.”

This is interesting because, in the very act of acknowledging the value and necessity of advice, the client is in the back of her mind wondering if she is getting overcharged.

This highlights an additional problem with the asset-based fee model: calculating the value of advice as a % of the assets invested makes far less sense when the scope of advice being given is broader than just the investments. The fee goes up and down based on the value of the assets, rather than the service received, and hence clients are left wondering if they are paying the right amount.

Closing Words

To sum up, financial advice has a solid foundation but has the potential to be so much more than it currently is. Chiefly, its mission should be to restrict access to the title of “financial advisor” by revising the requirements and opening up access to advice by restructuring the fee model.

Both consumers and advisors should recognize that many of the people who most need financial advice are not in a position to pay much for it. That has created industries like credit counseling, financial therapy, and a range of services designed to provide advice to financially stressed – or financially desperate – individuals. Practitioners in this space are also financial advisors. And should be recognized as such.

While certain types of advice may be displaced in the future, the need for a financial navigator has never been greater, and it is time that the industry evolves into the profession this new world requires.

About This Survey

The survey was conducted in October 2021 and consists of responses from 618 participants from across the USA. The respondents were all from households earning above $100k in annual income.

Copyright Information:

All the data included in this study is available via public domain. This means all statistics may be copied without permission. We do, however, appreciate citation as the source via a link.

Researcher:

Matthew Jackson

Resources:

Download Summary Data (PDF)

Sign up for The Brief by finmasters, our FREE weekly newsletter and get the latest tips on how to make more money, invest better and reach your financial goals.

No spam. Ever. We commit to never sharing or selling your personal information.