Banks have been investing heavily in AI. According to Allied Market Research, the business value of AI in banks was around $3.88 billion back in 2020, and they predict that by 2030, that figure may hit $64.03 billion[1].

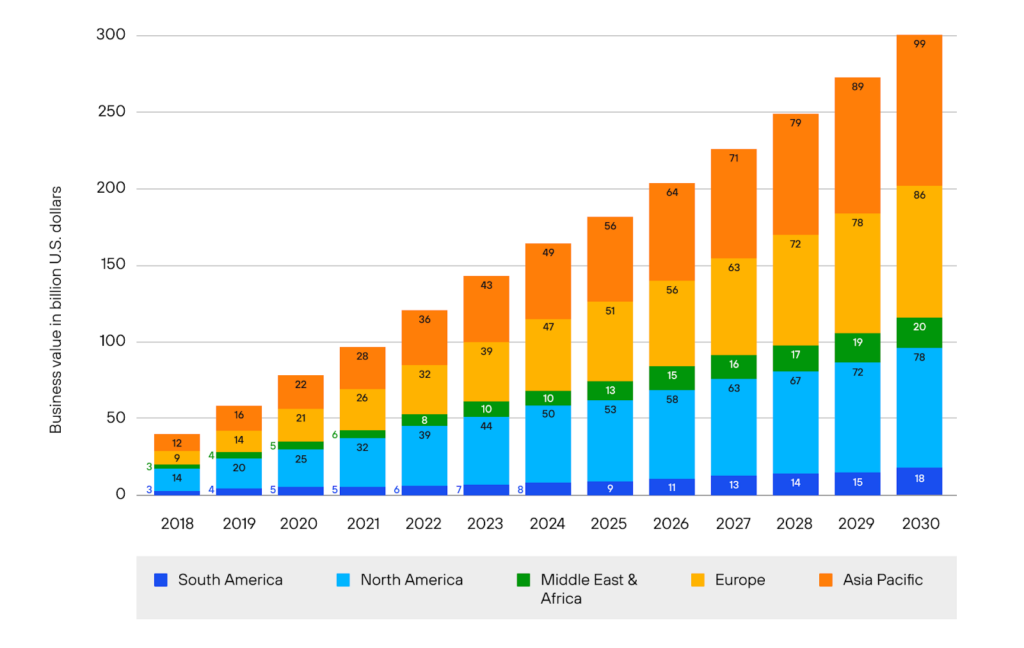

That $64.03 billion figure is near the low end of the spectrum. According to Statista, the number is closer to $300 billion, with the Asia Pacific region alone accounting for $99 billion[2]!

But, where is all of this business value coming from, and what is driving banks to invest so aggressively in this growing technology?

To answer that latter question, we must first take a quick look at banks and how they work.

The Modern Banking Environment

Banks are integral to our economy. They circulate money, redistribute risk, and ensure the wheels of capitalism are always greased and moving forward.

🏦 Banks perform three main functions:

- They serve customers and take in deposits from them.

- They give out loans and manage risks.

- They facilitate transactions.

For a bank to succeed and be profitable, it needs to remain compliant and observant of federal and state regulations. Otherwise, it might have to pay large fines and penalties, which in some cases can be ruinous.

However, in today’s competitive environment, remaining compliant isn’t enough for a bank to remain profitable.

The Competitiveness of the Banking Sector

Increased competition is one of the factors that have been driving decisions within the financial and banking sector.

For one thing, over the past two decades, banks that used to own a large portion of the financial sector have had to watch their different services get taken over by hip millennials and tech startups that offer better payment solutions, more personalized consumer lending products, and overall better customer experiences.

Moreover, several big tech companies have been getting into the game. Telecommunications giants have started offering their customers digital financial services. These services integrate well with the giant’s previously-existing suite of products and services, making the financial offering all the more attractive.

As if all of this wasn’t enough, banks are already having a hard time competing amongst themselves. Not only are there a lot of banks competing for the same consumer, but this stiff competition has also led to profit margins being flat for the past few decades.

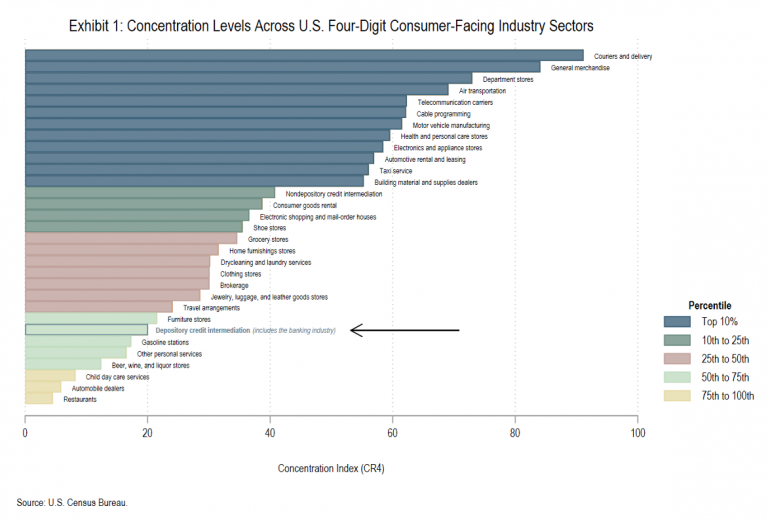

The above image shows the concentration levels of different industries within the US. The less concentrated an industry is, the more competitors there are in the market. And, the banking industry lies in the third quartile in terms of concentration.

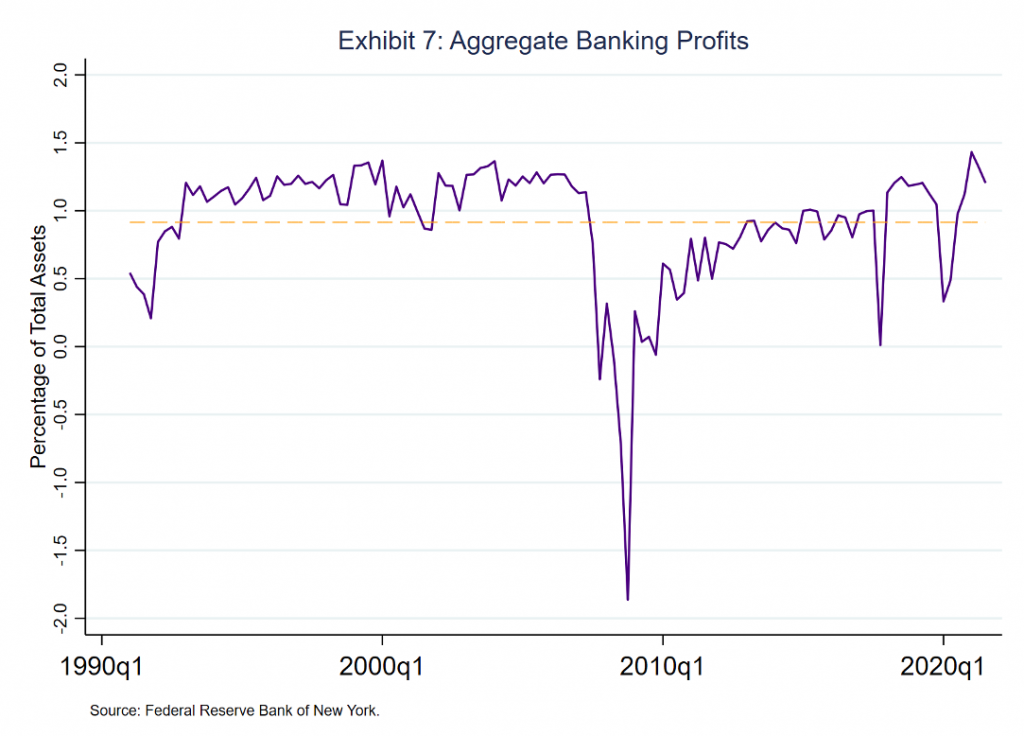

As you can see, profits in relation to total assets have been almost stable over the past 3 decades.

Thanks to this competitive environment, banks have been looking for any advantage they can get, leading them to AI.

Why Is Everybody Talking About AI?

AI has been around for a while. The idea first appeared on the scene back in the 1940s and picked up steam between 1957 and 1974. Even before the new millennium, AI was advanced enough to beat the best chess player in the world at his own game.

However, it wasn’t until this last decade that everybody has been talking about how AI is changing the world, particularly that of finance.

So, why the sudden peak in interest?

Big Data

As technology advanced, every piece of equipment got smarter: your phone understood your voice commands, your car learned how to drive itself, and your home started to anticipate your needs before you even had to express them. But, all this intelligence also meant that we were producing gargantuan amounts of data, which brought on an explosion of Big Data.

To wrangle all of this data, we need advanced, computerized models that can tame billions of data points and extract useful insights from them. Enter AI.

The Availability of the Necessary Infrastructure

Even though the mathematical models powering AI have been around for a while, we didn’t have the necessary infrastructure to benefit from them until recently.

So, what does AI need to flourish?

According to Leaseweb, a company that offers AI infrastructure, there are five main requirements:

- CPUs and GPUs powerful enough to provide AI with the necessary computing power to glide along rather than crawl.

- The ability to store mountains of data, providing the AI models with the very nutrients required for them to develop into healthy contributors.

- Networks that are efficient enough to empower specific AI models, such as deep-learning algorithms, that rely on dara-intensivef communications.

- Formidable cyber security, protecting all the stored data and ensuring that bad data doesn’t make it into the mix.

- Cost-effective solutions, making AI models accessible to everybody rather than just big companies.

So we live in a world where we are producing a lot of data, and we have the tools and infrastructure to analyze all of it.

But, what exactly can AI do to benefit banks?

The Different Functions of AI

There are several different roles AI can play within the banking sector.

Forecasting

Financial forecasting is critical to any business, and banks are no exception. For banks, solid forecasting means better management and smoother supervision. Banks deal with risk, and forecasting is a primary tool for mitigating risk.

Financial forecasting is also very difficult. It requires the use of advanced econometric tools and demands a large number of data points to produce anything remotely useful.

AI is great at handling data, making it an excellent tool to help with financial forecasting.

Natural Language Processing

Natural language processing, NLP for short, is a field of AI that explores how we can teach computers to not only understand the language but also to communicate with us as another human being would.

If you have heard of ChatGPT, or tried it out, then you have been exposed to the power of NLP.

However, how can NLP help financial institutions in general and banks in specific?

The most straightforward application involves chatbots, tools to facilitate the communication process between banks and their customers.

Another application involves analyzing financial documents. For example, instead of spending countless employee hours going over every document that gets sent, a bank could employ NLP to analyze these documents, make sure they are compliant, and extract any necessary information from them.

Image Recognition

Just like AI can recognize text and speech, it can also recognize images.

You have already used AI-powered image recognition if you have ever tried using Google’s search image function, where you upload a photo onto Google and ask it to tell you where this image came from or to find you similar images.

Banks have a lot to gain from image recognition.

For instance, when providing online services, banks need to make sure that the people they are dealing with are who they say they are. To that end, banks use image and facial recognition software to confirm the identity of the user.

A perfect case in point is how the Spanish Caixabank enables its customers to withdraw money from the ATM with the use of facial recognition software instead of needing a pin code.

Anomaly Detection

As mentioned earlier, AI is great at finding insights and patterns in large data sets. But, that also means that when something breaks a set pattern, i.e., becomes an anomaly, AI is great at spotting that too.

And, why does that matter?

Because in the world of banking and finance, an anomaly can highlight that a certain transaction is risky for some reason, if not downright fraudulent. So, when AI detects an anomaly, it shows bank regulators where they need to pay more attention.

Task Automation

Automating tasks can improve operating efficiency. This reduces manual labor, boosts productivity, and just fattens the bottom line. And, today, there are countless automation tools for us to lean on, from Siri and Alexa on our phones to Zapier and IFTTT online.

Banks can reap huge rewards from automation as well. For example, having digitized banking documents using NLP and image recognition, banks can then take the data from those documents to update their books and ledgers, streamlining the entire accounting process.

Having gone over some of the functions that AI can perform, let’s take a look at how banks can benefit from this.

How Banks Benefit From AI

To streamline this conversation, let’s explore the impact of AI technology along the following three pillars:

1. Serving Customers and Taking In Deposits

While one of the primary functions of a bank may be to take in deposits, there are countless ancillary services banks need to provide if they want to compete in today’s market.

For instance, banks need to provide payment solutions, ATM services, and online banking. (In fact, some banks specialize specifically in online banking)

So, with that said, let’s see how AI can improve banks’ services.

Voice Banking

Simply, voice banking gives the customer the ability to access banking services with nothing but their voice and words. It incorporates the use of AI; specifically, voice bots that rely on Natural Language Processing.

To be clear, voice banking is not the same as an IVR system. For example, the right AI system can recognize a customer’s emotions and assign priority accordingly. It can also provide a personalized experience based on the collected data on the customer. And, this is not to mention how voice banking can take care of everyday tasks, such as answering frequently asked questions and resolving simple customer complaints.

Over and above, voice banking can also act as a security layer, leveraging the user’s unique voice as a form of biometric security. It will be able to verify the validity of a transaction through the user’s unique voiceprint while increasing accessibility and streamlining the entire process.

Personalization

With the right AI, banks can offer their customers a personalized experience. After all, since banks collect swathes of data on each customer, they can use AI to analyze this data and to provide specific recommendations based on the customer’s unique behavior.

Better yet, banks can tailor these personalized suggestions based on the customers’ expressed goals. For example, if a customer says that they want to save for a big budget purchase, say a downpayment on a new house, then the bank might suggest a specific account or plan that takes into consideration both the expressed objective and the surrounding data, such as the customer’s income, their spending habits, and so on.

In other words, banks can provide each customer with a financial advisor who fits perfectly in their pocket. And, in the not-too-distant future, that very same financial advisor will not only suggest how you can better manage your money but will also do your taxes come April 15.

2. Giving out Loans and Managing Risks

The other main function of banks is to give out loans, be it in the form of credit cards to consumers, mortgages to homeowners, or business loans to companies big and small.

However, seeing as giving out loans is a risky process, banks need to actively manage their risk. This includes deciding the creditworthiness of each applicant and figuring out whether all the information presented is legitimate or not.

Fortunately, AI can provide plenty of help here.

Risk Assessment and Credit Risk Management

AI can play a huge role in risk management. It can tell banks how likely a particular applicant is to default on a loan as well as how severe the ensuing loss would be. As a result, banks will be in a better position to approve or decline the loan.

This is just the tip of the iceberg. AI systems can play an active role in collections, engaging with customers and helping them meet their debt obligations. Additionally, when a warning sign appears on the horizon, such as a customer who is about to default, AI systems can spot those early on and notify the bank.

Preventing Fraud and Cyber Attacks

To better manage their risks, banks need to be vigilant when it comes to protecting themselves and their customers. To that end, banks invest a lot in detecting fraud, spotting fake transactions, and assessing which loan applications are accurate and which are bogus. Moreover, they are happy to pay millions to beef up their cyber security and protect themselves from hackers.

The good news is that AI can help with these arduous tasks.

AI systems have become skilled at detecting and preventing fraud. As we saw earlier, AI and machine learning algorithms are quick to notice when anything breaks an established pattern within a data set. These anomaly-spotting algorithms are not only accurate and efficient, but they are also scalable, which means they can handle the incoming data growing in size.

Similarly, AI can help banks ward off cyber attacks. For instance, NLP-powered systems can spot vulnerabilities and stop them before they impact internal systems. As a case in point, one of the simplest ways hackers attack companies is through malicious links placed in emails, and AI can stop this by monitoring ingoing and outgoing emails and identifying any links that seem risky.

3. Staying Compliant

Seeing as banks deal with a lot of sensitive information, not to mention our money and livelihood, they have to follow strict rules and regulations enforced on them both at the state level and the federal level.

The flipside here is that banks now have to tussle with another type of risk: compliance risk. Simply, compliance risk is the possibility that a company or financial institution will have to pay penalties or fines to the government because it failed to comply with the regulations.

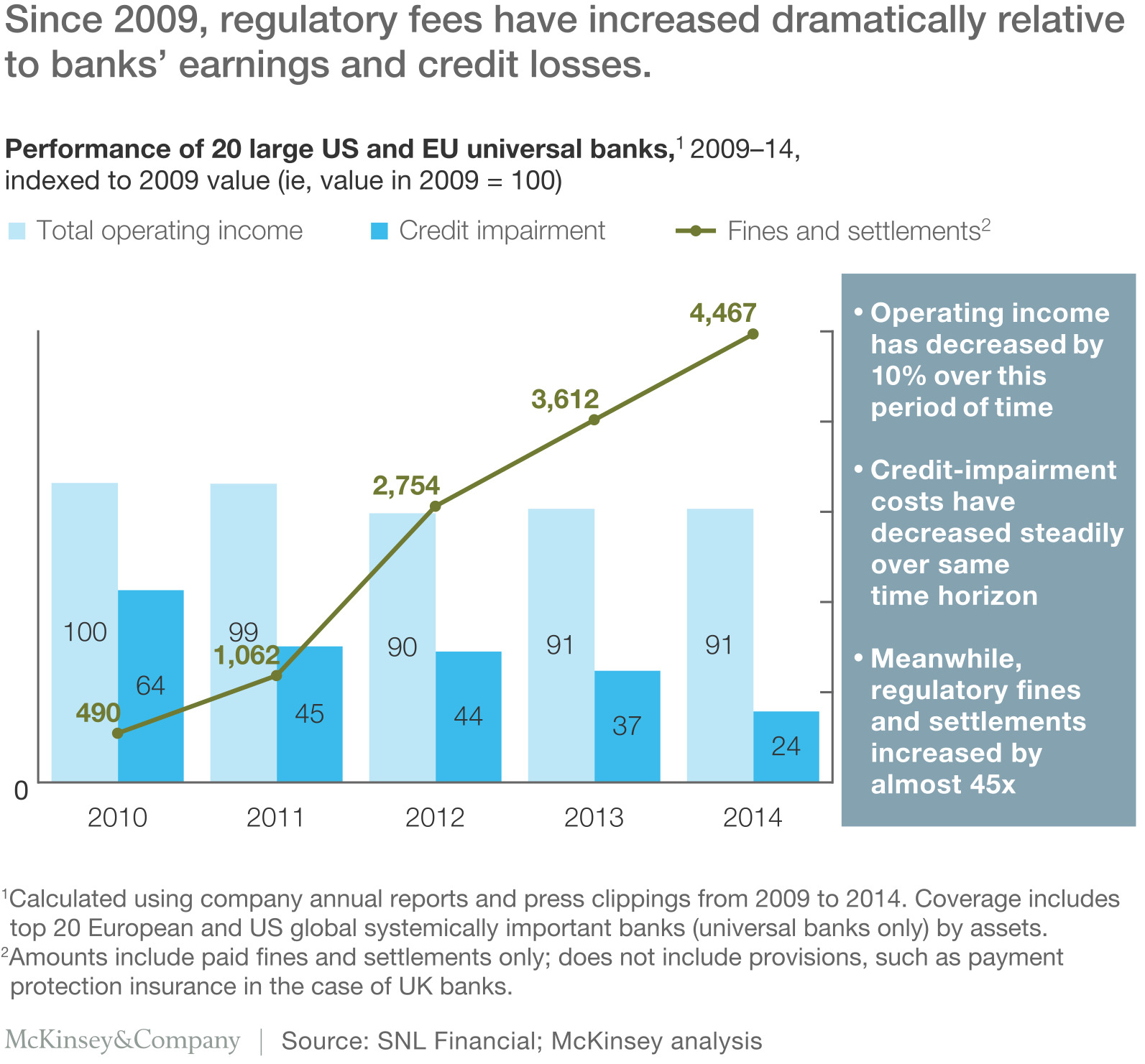

Accordingly, banks pay a lot of money, called regulatory fees, to stay within the lines. The problem is that these regulatory fees have been going up for the past few years, especially after the 2008 financial crisis.

Compliance issues don’t just incur fees. They have an immediate impact on share values and on the bank’s ability to attract and retain customers.

As a result, banks stand to gain from using AI to help with compliance and lower regulatory fees.

Automating Compliance Processes

Banks have to follow specific rules and processes to remain compliant. The good news is that a lot of these processes can be automated with the help of AI.

Take the process of KYC, which stands for Know Your Customer. It involves banks verifying that customers are who they say are. Think of it as a form of ID verification.

While the process of KYC makes sense from a risk management standpoint, it is actually mandatory for all banks anytime someone opens a new account. It helps the government combat money launderers, identity thieves, and individuals financing terrorism.

So, how do banks perform KYC?

Simple. They ask you for your ID, proof of residence, and any other documentation that confirms your identity. Then, a bank employee goes over that documentation, makes sure everything is in order, and checks that the ID provided is truly yours. If everything is on the level, the bank will be happy to open a bank account for you.

However, the process above can be laborious, slow, and costly if done by a human being.

This is where AI and eKYC, which stands for electronic Know Your Customer, enter the scene.

In a nutshell, with eKYC, banks verify your identity digitally. They ask you to send them pictures of your ID and all other supporting documentation through the internet. Additionally, they will ask you to send them pictures of yourself and might request that you perform certain poses.

After that, AI systems can leverage NLP and Image recognition to go over the documents, check to see if you are the owner of the ID, and ensure that everything else is compliant. All this is done with minimal to no human interaction, minimizing the costs of the process.

Keeping Up With Regulatory Changes

Part of compliance risk comes from constant regulatory changes. In other words, any time the government changes the rules, it is the bank’s responsibility to not only be aware of the change but also to understand how that change affects them.

Consequently, a bank’s compliance department works hard to keep abreast of thousands of regulatory documents and have them all housed in one central repository. And, when any rule is changed or updated, the compliance department has to notify the other bank departments how that change will affect their day-to-day.

Banks that work in multiple states and countries may have to track regulatory changes across multiple jurisdictions at the same time.

Normally, this is an exhausting process that would take several manhours.

But, AI, specifically NLP and task automation, can pore over the documents, classifying them and highlighting any relevant changes. The right algorithms can also point out areas that might have to adapt to these changes, saving the bank from falling on the wrong side of the law.

So, What Does All This Mean For You?

We have been talking about how banks stand to gain from AI, including better services, more automated processes, and savings that are projected to reach $1 trillion by 2030.

And, with all of this money saved, banks will be able to push some of those savings to you, the consumer. As operations get automated, banks will be able to make their services cheaper and faster.

But, is it all upside?

Even though consumers should be delighted that banks are boosting their services with AI, you should also bear in mind that there are a few potholes along the road.

Data Privacy Issues

AI can be excellent at predicting and spotting patterns assuming that it has been trained on a lot of data. But, the million-dollar question is where will it get all this data from in the first place?

This is where the first problem pops up.

Customer data is surrounded by laws and regulations designed to protect you and your right to privacy. For instance, in Europe, data is subsumed under GDPR, defining the legal rights of any entity to use your data along with the necessary security and confidentiality constraints that need to be put in place.

However, in an attempt to stay competitive, some banks might feel that these rules are too restrictive and decide to skirt these regulations. As a result, these banks would compromise your privacy and security in the name of innovation and progress.

Now, I’m a big fan of forward momentum, but I think we must always calculate the cost of that motion. And, a world with no security or privacy from big institutions might be too steep a price.

However, banks don’t have to sacrifice innovation for our sake. There are multiple ways these financial institutions can stay at the cutting edge of AI while still protecting our data. For instance, they can explore avenues such as differential privacy and AI-generated synthetic data.

Cybersecurity

We talked about how AI will enable banks to beef up their cyber security, but it is also worth mentioning that hackers can also benefit from AI.

With AI, hackers have access to a suite of tools more advanced than ever before. An excellent case in point was highlighted by Brian Finch, a cybersecurity expert, when he said, “AI can be used to identify patterns in computer systems that reveal weaknesses in software or security programs, thus allowing hackers to exploit those newly discovered weaknesses.”

Another example of AI enabling hackers comes from the world of email phishing. Again, Finch says, “Security experts have noted that AI-generated phishing emails actually have higher rates of being opened — tricking possible victims into clicking on them and thus generating attacks — than manually crafted phishing emails.”

And to top it all off, this cyber arms race between hackers and financial institutions actually favors the hackers. The reason is that it is both more cost-effective and simpler to create a cyber attack than it is to defend against one.

So, if banks aren’t careful, you can expect reports of scams, hacks, and security breaches, many of which could end up impacting you.

Embedded Bias

AI will play a large role in deciding who gets loans and who ends up scrounging finances through alternative sources. But, what if the AI systems that banks use become biased somehow?

For instance, do you remember the story of the AI bot that was unleashed on the Twitterverse only to become racist and abrasive? And, it took less than 24 hours.

The point is that AI is only as good as the data that trains it. Because existing data reflect existing social biases, there’s a real risk that AI may simply replicate those biases.

So, how will AI affect disenfranchised communities and those that are almost invisible to the financial system?

For example, there is a large portion of the American population that is unbanked or slow to go digital. Unless AI system creators are careful, those people could get labeled as unbankable or just as bad financial prospects. Not only would this further these people’s financial exclusion, but it would also increase the overall economic inequality within the US.

As a result, there must always be human supervision paired with AI systems to ensure that the systems don’t skew too much in any unhealthy direction.

Inflexibility

AI has enormous capabilities, but it’s still limited by its programming. As anyone who has ever used automated customer service knows, AI can handle problems that fit its programmed flow chart very well, but completely stalls out when it has to confront a problem it’s not programmed to recognize and solve.

The risk here is that banks may become so enamored of AI that they eliminate human systems that are capable of recognizing and adjusting to problems outside their immediate routine. That could negate all of the customer service gains that AI offers.

After all, while replacing human service representatives with AI certainly saves the bank money, it doesn’t always work in favor of the customer!

Putting It All Together…

To deal with the competitive pressures squeezing their profit margins, banks have been pumping a lot of money into AI. They have been able to benefit from technologies such as NLP, Image recognition software, and task automation.

This technology has been helping banks provide a better quality of service, enabling them to better manage their risks, and ensuring that they stay compliant. Nevertheless, banks also need to proceed with caution because some possible drawbacks could harm customers instead of helping them.