S.M.A.R.T. financial goals can help us turn aspirations into achievements. Initially, we’re thrilled about setting our financial targets, but as soon as we hit a few bumps in the road, we get discouraged. S.M.A.R.T. financial goals help us overcome the challenges and stay committed to success.

What Are S.M.A.R.T. Financial Goals?

You’re probably already familiar with the S.M.A.R.T. formula: specific, measurable, achievable, realistic, and time-based. But did you know can use those factors to increase your chance of achieving your financial goals?

Let’s look at each of those factors and how you can use it.

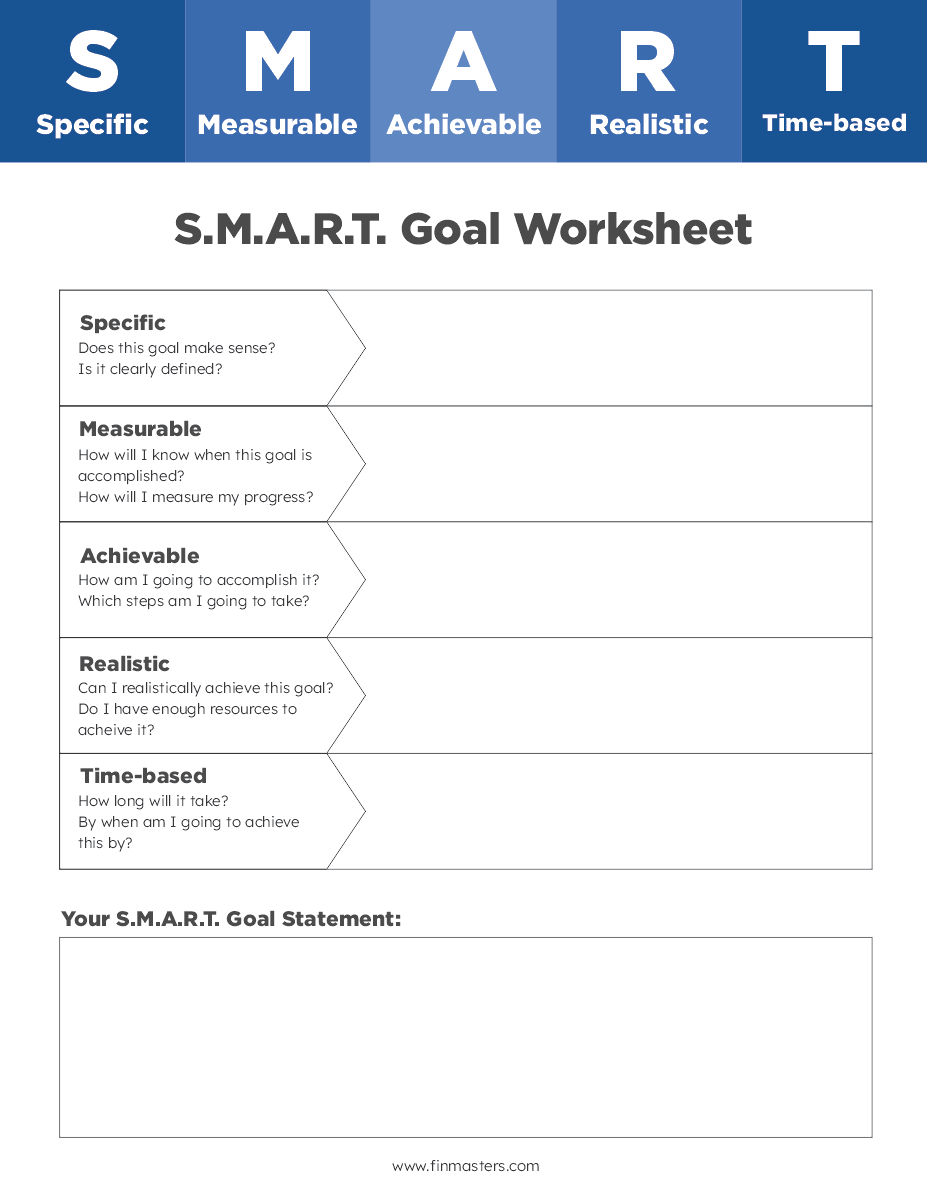

| Specific | Your goal has to be specific, not generic or vague. Be clear on what you want to accomplish and ask yourself how this goal will put you in a better financial situation. You can't get what you want if you don't know what you want. |

| Measurable | Make your financial goal measurable by quantifying it so you can evaluate your progress and overall success. Express your goals in clear numbers, so you'll know where you are and when you've succeeded. |

| Achievable | One of the biggest obstacles to achieving a goal is setting your expectations too high. The surest way to improve your financial situation is to take achievable steps. If that means taking smaller steps, that's ok. You can always set a new goal! |

| Realistic | When setting the goal, assess the steps you plan to take to achieve the goal. Ask yourself if those steps are realistic given your current circumstances. Setting unrealistic goals usually leads to disappointment and surrender. |

| Time-based | Give yourself a time frame to achieve this goal. This will encourage you to follow through, stop procrastinating, and keep yourself accountable. |

Examples of S.M.A.R.T. Financial Goals

Let’s look at four examples of S.M.A.R.T. financial goals that illustrate how these goals can help you achieve financial freedom.

Example #1: Paying off Your Credit Card Debt

If you’ve accumulated credit card debt, you can pay it off using the S.M.A.R.T. formula.

👉 Specific

Let’s break things down. Your specific goal is to pay off your credit card debt in full.

👉 Measurable

How much money do you owe on your credit card? This figure (for example $3,000) will make your goal measurable.

Your new goal is now paying off your $3,000 credit card debt in full.

👉 Achievable

To achieve this, you will need to take actionable steps that will help you track your progress.

To successfully pay off your $3,000 debt, you will put $300 plus interest every month towards your credit card. You will also stop using it temporarily to avoid accumulating additional debt.

👉 Realistic

Assess the steps you plan to take to achieve your goal. If you’re willing to pick up extra shifts at work, cut your entertainment budget, and stop borrowing more, your goal is realistic. If you’re hoping to get a promotion or win the money on a betting app, then you may want to re-think your strategy.

👉 Time-based

By applying $300/month plus interest towards your debt, you will achieve your goal in 10 months.

Your S.M.A.R.T. financial goal is:

I will pay off my $3,000 credit card debt in 10 months by putting $300/month (plus interest) towards it. I will achieve this by cutting my entertainment budget and not using my card during this time.

Example # 2: Saving for a Down Payment on a Home

If you want to become a homeowner in the next few years, you should be saving for a down payment. Here’s how to turn that dream into a S.M.A.R.T. financial goal.

👉 Specific

Get as specific as possible. Your goal is to save enough to make a down payment on a home.

👉 Measurable

Determine exactly how much you want your down payment to be. Consider what you expect to pay for a home, and aim for 20% of that. For example, your goal may be to save $20,000 for a down payment.

👉 Achievable

$20,000 is a significant amount, so you need to set targets to make it happen. If you want to buy your home in 3 years, for example, you need to save approximately $556 monthly.

👉 Realistic

Use a budget calculator to determine how much you can save monthly. Consider practical ways to earn extra income or cut certain expenses from your budget to achieve your ideal amount.

If saving $20,000 in the time frame you’ve chosen is completely unrealistic for you, consider extending your timeline or shopping for a cheaper home.

👉 Time-based

Based on the amount you need to save and your monthly saving target, decide on a realistic time frame for your goal.

Your S.M.A.R.T. financial goal is:

I will save $20,000 in 3 years for a down payment on my future home. I will accomplish this by putting $556 into a savings account monthly.

Example # 3: Budgeting to Create an Emergency Fund

You can use the S.M.A.R.T. formula to build a rainy day fund.

👉 Specific

Determine why you want to start budgeting and how it will help you. In this case, your specific goal is to create a monthly budget so you can save money for an emergency fund.

👉 Measurable

Experts say that your emergency fund should be able to support you for three to six months. To figure out how much yours should be worth, think about how much money you currently need to support yourself every month.

For example, your new goal will now be to fully fund a $6,000 emergency fund by creating a monthly budget.

👉 Achievable

Use a budgeting calculator to figure out where you currently stand. Next, determine the right budgeting method for you and use a budgeting tool to implement it.

Suppose after doing so, you free up $250 monthly which can go towards your emergency fund.

👉 Realistic

Your goal may be unrealistic at the moment if you are currently over budget and struggling to make monthly payments to outstanding debts. Perhaps your focus should be on budgeting to pay off debt rather than to save for an emergency fund.

👉 Time-based

By saving $250 a month, you will be able to reach your goal in 2 years.

Your S.M.A.R.T. financial goal is:

I will fully fund a $6,000 emergency fund in 2 years by using the reverse budgeting method to save $250/month.

Example # 4: Planning for Retirement

Planning for retirement should be on everyone’s list of financial goals. But how can we make it S.M.A.R.T.?

👉 Specific

Planning for retirement is a little too vague. Contributing a minimum monthly amount to your 401(k) to save for retirement is much more specific.

👉 Measurable

You can measure your success each month by contributing a percentage of your paycheck. Your new goal now becomes contributing 15% of your income to your 401(k).

👉 Achievable

Setting up automatic deductions from your salary towards your 401(k) is an actionable step that will achieve your goal.

👉 Realistic

To determine if this goal is realistic given your current financial situation, ask yourself if you can live on a paycheck that is 15% smaller. If not, then you can either lower your contribution amount or lower your monthly expenses.

👉 Time-based

When it comes to planning for retirement, there is no time like the present. This is a long-term goal, but you can set intermediate goals as well. How much do you expect to have in your 401(k) after a year? After 5 years?

Your S.M.A.R.T. financial goal is:

Starting this week, I will contribute 15% of my monthly income to my 401(k) plan and receive matching contributions. This will help me prepare for retirement.

S.M.A.R.T. Goals Worksheet Template

Do you have any S.M.A.R.T. financial goals you want to accomplish this year? To help you get started we’ve prepared this simple printable S.M.A.R.T. goals template that you can use to define your goals.